Macro Trends Now at the Helm of Crypto Price Movements; We Expect This Trend to Continue

The market price action should remain tethered to macro trends. This means we could range trade for a while. Given how strong and how fast prices have been up over the past six months, it could be a positive to take a breather to resume an uptrend later on.

As we anticipated a few months ago, macro has been gaining influence in crypto price action and is now the primary driver. The cloudy environment put pressure on prices for most of the week, but the weaker-than-expected jobs data brought some relief to risk assets.

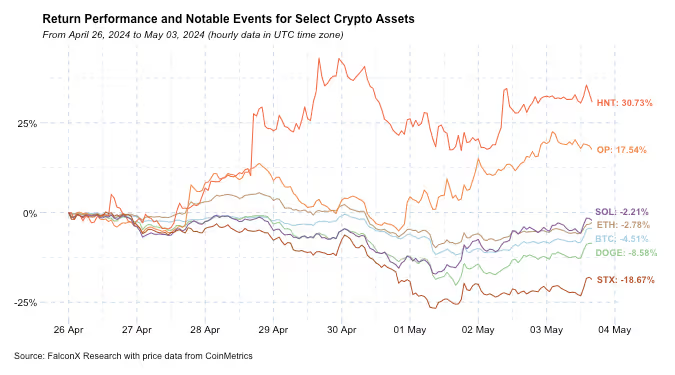

ETH outperformed BTC, which is notable during a period of market correction (more on that below). Only seven of the 23 assets with a fully diluted market cap above $10 billion were in the black over the past seven days.

Among those, OP has been the highlight, with double-digit gains after reports alleging that a16z crypto executed a large private token purchase. Other assets corrected from big moves: While STX and DOGE were down by double digits after a strong performance at the beginning of the year, HNT was up 30%, following a dismal performance over the past couple of months.

There are many macro cross-currents influencing prices. The most important factor remains the outlook of monetary policy in the US, which has been changing on the back of sticky inflation prints. According to CME Fed Fund futures, the odds of a cut in the June FOMC meeting moved to 8% from 62% a month ago. Add to those uncertainties on the JPY reaching multi-decade lows against the USD, whether or not China will inject liquidity to alleviate its economic woes, and geopolitical tensions that continue to mount.

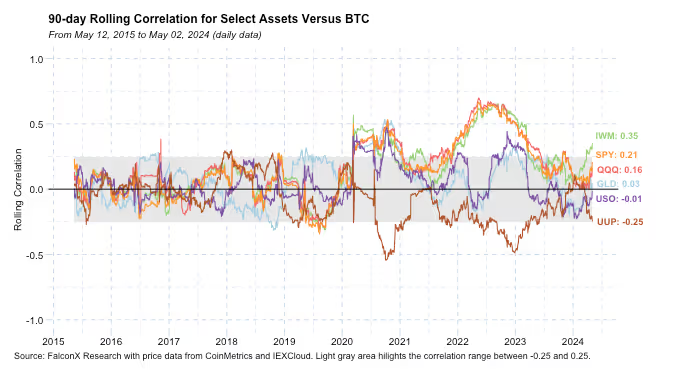

The correlation between BTC and other broader risk assets is still low but has been trending up over the last couple of months. The chart below shows a long-term chart of 90-day rolling correlations against some assets that track broader indices (SPY, QQQ, and IWM) or global macro assets (GLD and USO). Although we are still far from levels that would put crypto’s diversification properties into question, it puts into context how macro is becoming a more important driver.

On top of that, the market currently lacks significant industry-specific catalysis. The US spot ETFs have been a substantial boon for prices and will continue to be a driver, but likely more on a medium- to long-term basis from here on.

The Hong Kong spot ETFs were a notable milestone, and perhaps those who called it a disappointment set their expectations too high. Adjusted for the size of that market compared to the US, first-day asset gathering came in positive at $292 million. However, it’s important to keep in mind that, unlike the U.S. ETFs that start with almost zero assets, it is common for ETFs in other jurisdictions to gather assets before launch. Case in point, second-day inflows amounted to $10 million.

It is interesting to see Hong Kong ahead of the U.S. in terms of having a spot ETH ETF and allowing for in-kind creations and redemptions. But they should not be a meaningful price action driver in the short or even medium term.

As a result, the market price action should remain tethered to macro trends. This means we could range trade for a while. Given how strong and how fast prices have been up over the past six months, it could be a positive to take a breather to resume an uptrend later on.

Other Top Trends We're Watching

FalconX Trading Desk Color: Desk flow varied over the past week, with prop desks and hedge funds switching between better buyers and sellers, retail aggregators coming mostly on the sell side, and venture funds coming mostly on the buy side. Our total volume in BTC continues to surpass ETH’s by a factor of more than 2x, and we continue to see higher buy/sell ratios for BTC than for ETH. The ratio between BTC and ETH vs. other assets volume remains in the 1.5-3.0x range. Alts activity remained somewhat concentrated in names such as SOL, NEAR, MATIC, AVAX.

Ethereum's Resilience in Market Correction Raises Questions on How Long It Can Continue to Lag: Over the past two weeks, ETH has outperformed BTC by over four percentage points, a rare feat during a broad market correction. Still, even after the bounce back, the ETH/BTC price ratio remains near its three-year lows at around 0.047

Part of ETH's underperformance in 2024 is linked to the market lowering the chances of a spot ETF approval come May 23. The ETHE NAV discount, a proxy for how the market is pricing odds, has expanded from 8% to 25%. Another part of the story is how Solana has gathered momentum, attracting important applications such as the DePIN ecosystem, while trading at less than 20% of Ethereum's FDV. Additionally, some investors gain indirect exposure to Ethereum without actually holding ETH by investing in related ecosystems such as L2s, middleware, or applications.

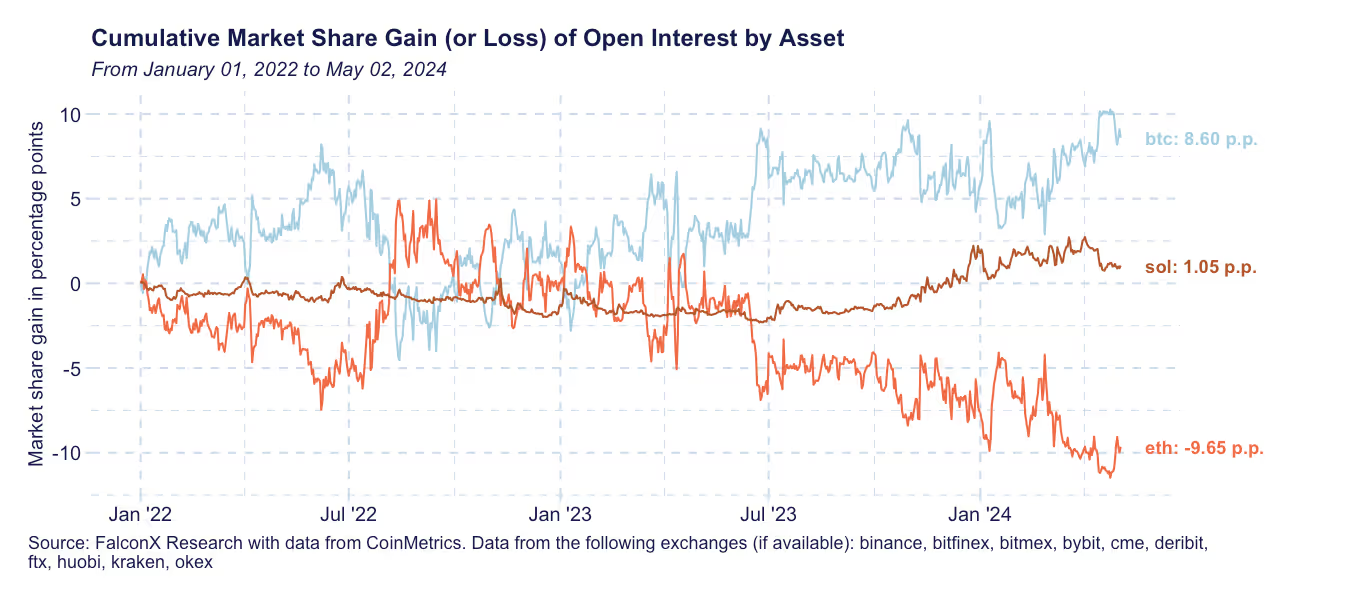

The result is that ETH might be the most under-owned crypto asset at the moment. Since 2022, ETH has lost more than ten percentage points of futures open interest market share to BTC and SOL.

Could the underperformance continue over the next few weeks? The next focus is the SEC decision on the spot ETH ETF, which is due by May 23. The market is already widely expecting a rejection, but it will be interesting to see how it reacts if the expectation materializes.

The most interesting question is how ETH can perform through the rest of the year. One intriguing argument is whether ETH can emerge as the best way to play the impact of the upcoming presidential elections in crypto. Given the perception of how Ethereum has been held back by regulatory impediments, a potential change in administration could spark hopes that some of that pressure would be released.

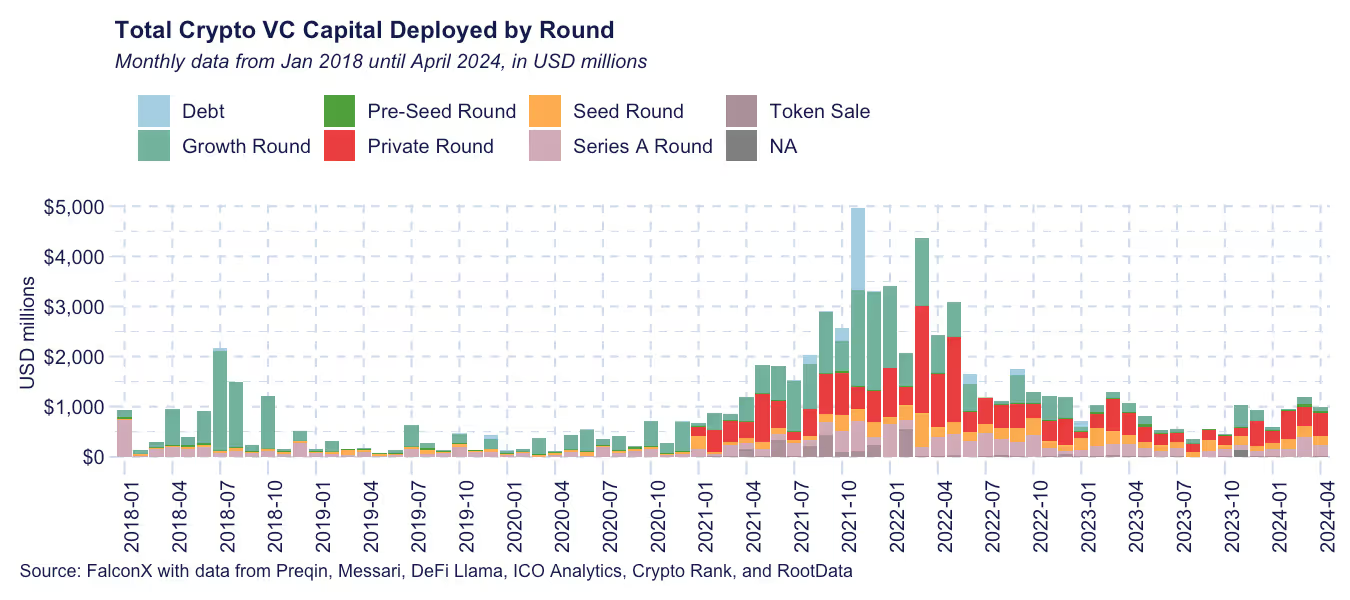

April Venture Capital Deployment Data Suggests the Private Market Remains Heated: According to data from our market-making team, crypto venture capital deployment remained strong in April at $990 million, higher than the average number for Q1 2024 of $909 million. If this trend is maintained over the next two months, Q2 2024 would mark the third straight increase in VC capital deployment.

Sectors that gained market share this month include infra and defi. Parallelized EVM chain developer Monad Labs raised $225 million led by Paradigm with the participation of other storied investors. Bitcoin miner manufacturer Auradine raised a series B of $80 million ahead of the halving from several investors. DePIN platform IOTEX raised $50 million from a group of investors that include SNZ Capital, Foresight Ventures, and Borderless Capital.

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd., nor Banzai Pipeline Limited (separately and collectively “FalconX”) service retail counterparties, and the information on this website is NOT intended for retail investors. The material published on this website is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this website is not and should not be regarded as investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory, and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over-the-counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered with the U.S. Commodities Futures Trading Commission (CFTC) as a swap dealer and a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is a registered Class 3 VFA service provider with the Malta Financial Services Authority under the Virtual Financial Assets Act of 2018. FalconX Limited is licensed to provide the following services to Experienced Investors, Execution of orders on behalf of other persons, Custodian or Nominee Services, and Dealing on own account. FalconX’s complaint policy can be accessed by sending a request to complaints@falconx.io

"FalconX" is a marketing name for FalconX Limited and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.