Initital Observations and Perspectives on Alts Supply Dynamics

The supply dynamics of some of the most prominent alts are already becoming a topic of conversation and a factor of price formation worth monitoring, especially as we move into a meaningful amount of unlocks coming over the next 1-2 years.

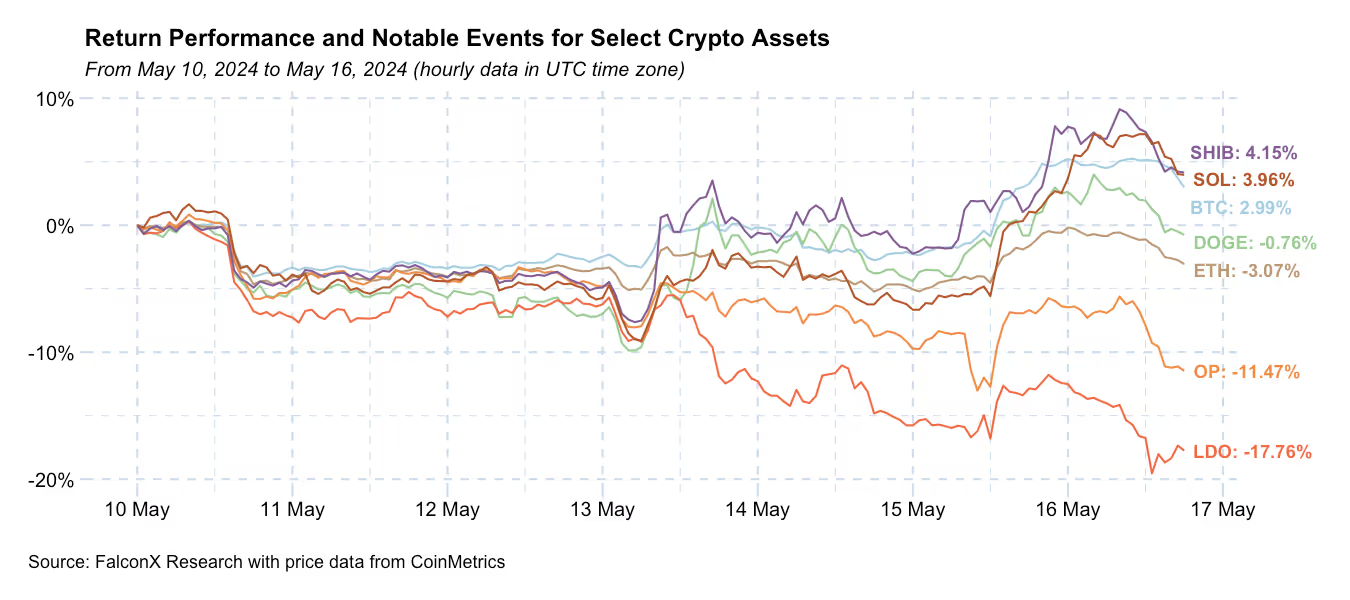

After trading flattish for most of the week, BTC broke above the $66k level on the back of inflation and activity data favorable to risk assets. Macro remains the primary price driver, with the correlation between BTC and the SPY reaching 0.26, which is still low in absolute terms but the highest mark since November 2023.

To close a positive week for the industry, the Senate voted yesterday 60 to 38 to support a resolution to overturn SAB 121 proposed by the SEC. The vote had strong bipartisan support and now goes to the White House, which threatened a veto last week. SAB 121 mandates that companies holding crypto assets for customers must record them on their balance sheets, potentially leading to capital implications for banks that engage with this asset class.

The focus now is on what the White House, who threatened a veto, will do. From a longer-term view, however, the fact that the first stand-alone crypto bill to ever be voted in either Chamber of Congress passed with such flying colors is highly significant. It will likely reverberate throughout this election year.

SHIB, DOGE, and SOL were among the best performers over the past seven days as assets that benefit from the meme mania got some lift after the re-emergence of Roaring Kitty. The Ethereum ecosystem, on the other hand, continues to lag. The ETH/BTC ratio touched 0.045, the lowest level in over three years.

Bitcoin dominance sits now at above 50% and apparently continues to trend higher. On one hand this reflects ETF inflows, excitement around potential new use cases for the Bitcoin network, and the sheer size and brand awareness of the largest crypto asset.

Less explored, though, is how the non-circulating part of the crypto market cap, which is not computed in the most common dominance metrics, has been growing recently.

The chart below shows the difference between fully diluted and circulating market cap for the top 100 tokens at CoinMarketCap (excluding Bitcoin, Ethereum, and stablecoins). This non-circulating part of the crypto market capitalization was hovering around $100 billion until the market rally that started in October. It now stands at $250 billion after crossing the $350 billion mark in March.

While part of the increase reflects higher token prices, part also came from newer assets that launched with a relatively low circulating portion of their fully diluted market capitalization.

The prime example is WLD, which boasts a fully diluted market capitalization of almost $50 billion on only 2.1% float and accounts for almost 20% of the total non-circulating market capitalization.

Still, the supply dynamics are meaningful even if we exclude WDL and include only the other 21 projects listed above, which amount to the next 70% of the industry's total non-circulating market capitalization.

The total non-circulating supply of these assets amounts to 618 days of their average daily spot trading volume and 279 days of their futures trading volume. These numbers can be low for some of the most established assets (for SOL, they are 10 and 3 days, respectively).

However, this new supply that will eventually start circulating for other projects might take more work to digest.

Everything else equal, this trend is likely to increase going forward. Notably, the number above does not account for EIGEN, which launched but is not yet tradable, and the potential upcoming large launches of projects like ZeroSync, LayerZero, and Blast, which are expected to significantly impact the market dynamics and should be closely monitored.

All in all, the supply dynamics of some alts are already becoming not only a topic of conversation but also a factor of price formation worth monitoring, especially as we move into those unlocks coming over the next 1-2 years.

Other Top Trends We're Watching

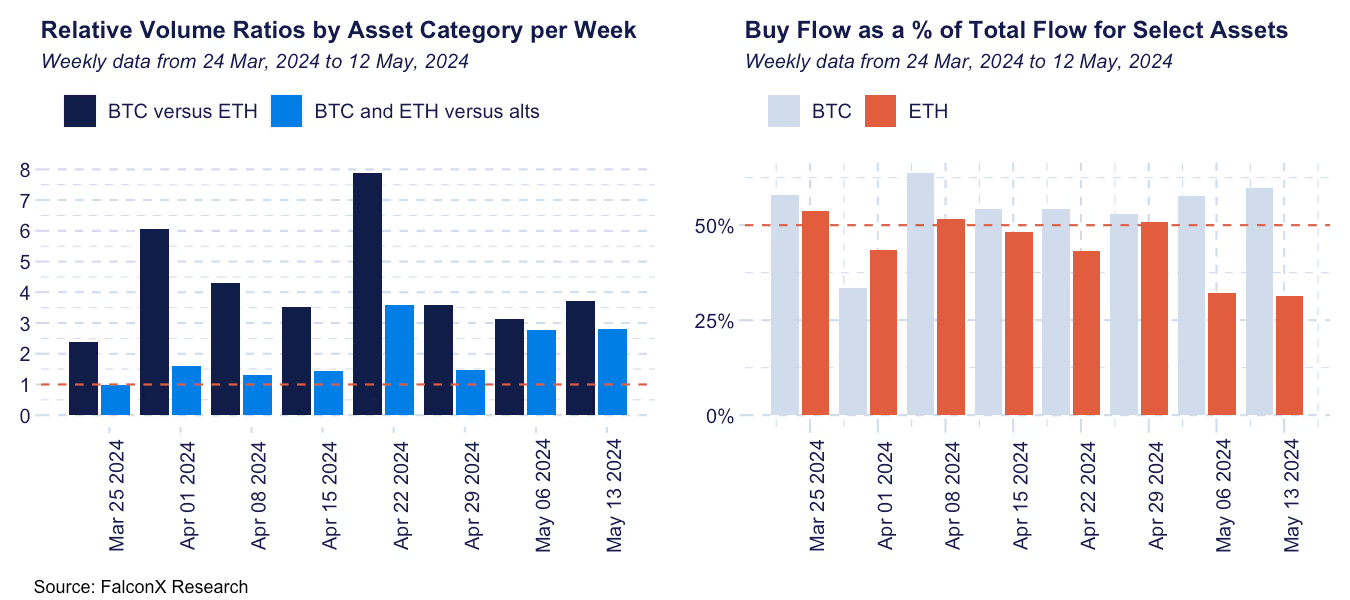

FalconX Trading Desk Color: Client personas have recently been varying between better buyers and better sellers across weeks at our desk, and the past week has been no different. While proprietary trading desks and retail aggregators swung from better sellers to better buyers, hedge funds and venture capital firms switched from better buyers to better sellers. BTC volumes continue to dominate ETH’s by a factor of at least 3x. For the third week in a row, we saw the majority of our BTC flow coming from the buy side and the majority of our ETH flow coming from the sell side. Volumes in majors continue to dominate alts by a factor of 2.5-5.0 times depending on the week. Within alts, we were better buyers of LDO, ENA, and NEAR and slightly better sellers of SOL and DOGE.

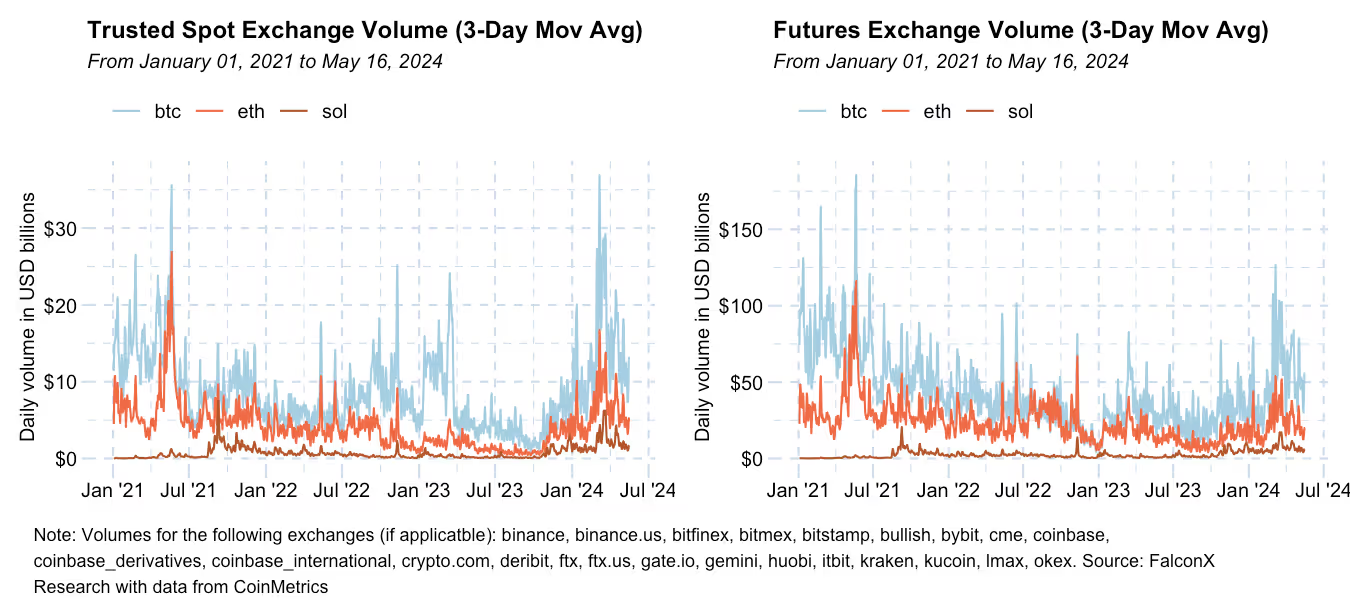

Spot and Futures Trade Volume Remain Soft, U.S. Flow Recovery Remains Essential for Price Action: As we have been highlighting since the beginning of April, trade volumes significantly shrunk after the end of March. The drop was more pronounced in the spot market, with BTC and ETH total volumes on trusted exchanges shrinking by 28% and 27% versus 22% and 26% in the futures market, respectively. Even the price recovery of the past three days has been supported by relatively soft volumes.

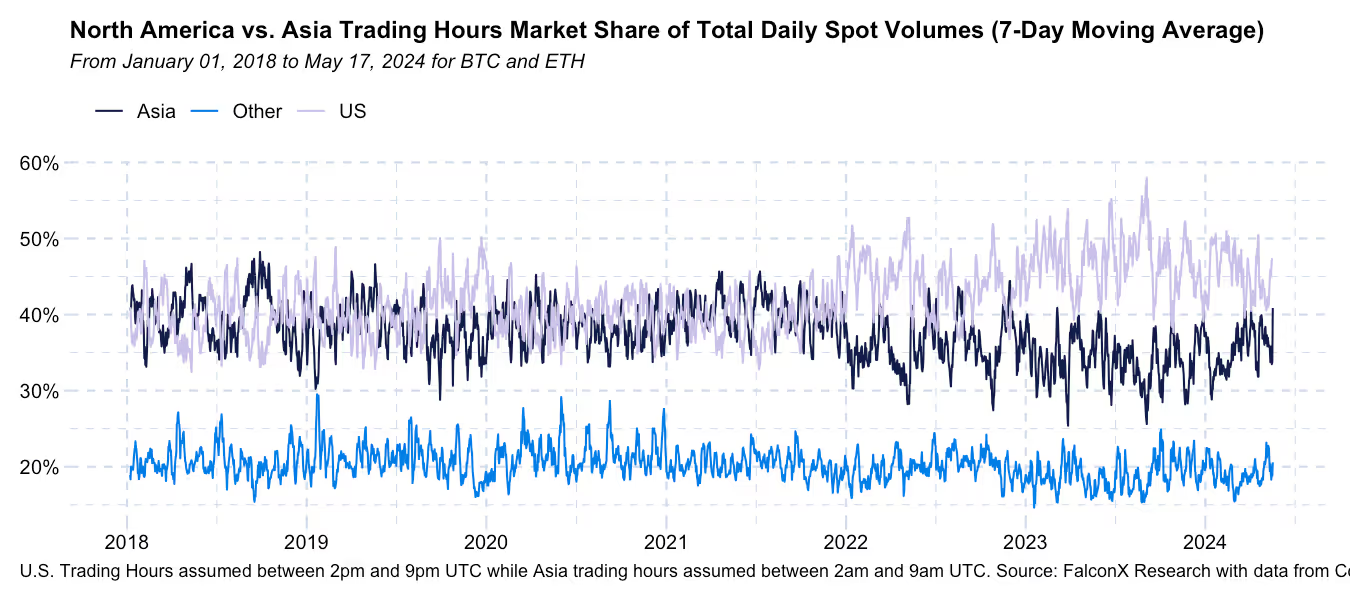

Interestingly, this has been accompanied by a sharper drop during U.S. trading hours, at least on the spot side. Spot trading in majors BTC and ETH during U.S. hours (7-day moving average) fell from around 50% until the beginning of the year to about 45% currently after touching 40%.

Most of the current and future critical major market drivers are still associated with U.S.-centric events, such as spot BTC ETF flows, the path of monetary and future policy, and now the upcoming presidential election.

It is therefore not a coincidence that the recent upswing came supported by stronger trading activity during U.S. hours. I expect the relative strength of U.S.-related crypto trading activiy to remain a critical confirming indicator for a decisive break from the current price range.

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd., nor Banzai Pipeline Limited (separately and collectively “FalconX”) service retail counterparties, and the information on this website is NOT intended for retail investors. The material published on this website is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this website is not and should not be regarded as investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory, and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over-the-counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered with the U.S. Commodities Futures Trading Commission (CFTC) as a swap dealer and a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is a registered Class 3 VFA service provider with the Malta Financial Services Authority under the Virtual Financial Assets Act of 2018. FalconX Limited is licensed to provide the following services to Experienced Investors, Execution of orders on behalf of other persons, Custodian or Nominee Services, and Dealing on own account. FalconX’s complaint policy can be accessed by sending a request to complaints@falconx.io

"FalconX" is a marketing name for FalconX Limited and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.