Is the Memecoin Mania Losing Steam? Analyzing Liquidity Trends of Crypto’s Most Unexpected Phenomenon

Memecoins have been a driving force within crypto in 2024. We analyze liquidity dynamics to provide more context than just the price action. For better or worse, memecoins are likely to remain a topic of conversation in crypto circles for a while.

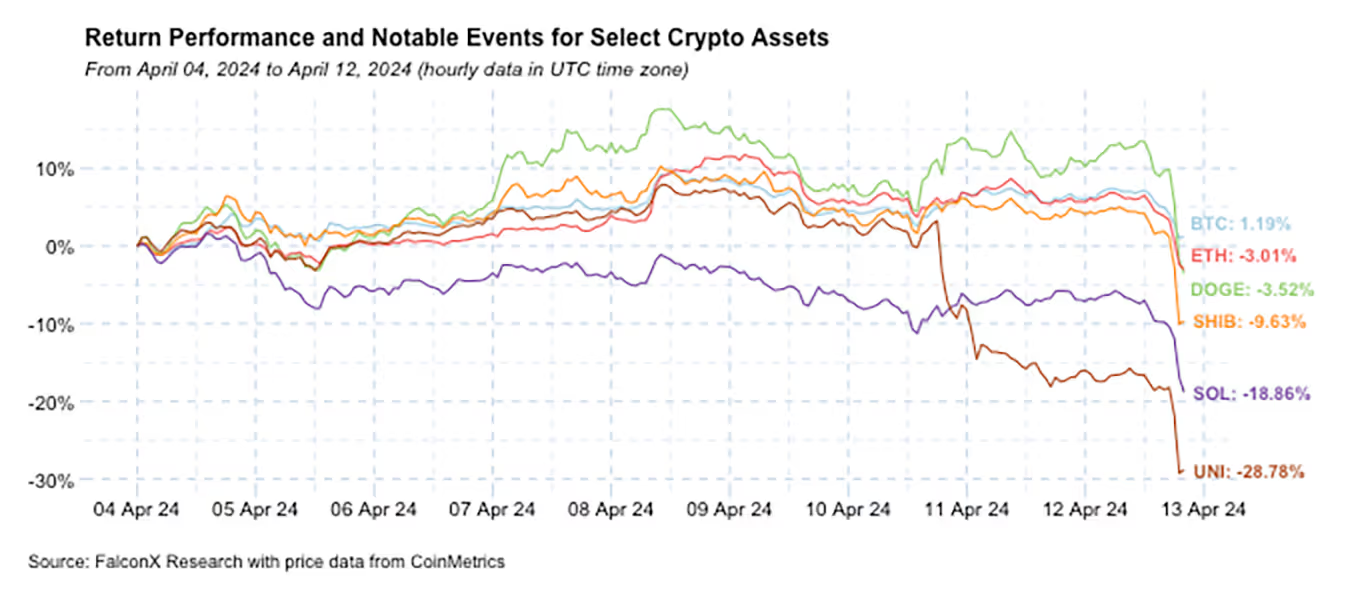

Crypto traded in positive territory for most of the week, but risk-off sentiment prevailed at the very end. Escalating geopolitical tensions in the Middle East added to a complex macro landscape characterized by persistent inflation and substantial deficits.

BTC was the only asset among the larger names that finished the week in the black. Conversely, SOL underperformed as the Solana network faced performance issues on the heels of strong activity Additionally, UNI witnessed a sell-off following the issuance of a Wells notice to Uniswap Labs by the SEC, an event that could potentially precipitate further legal entanglements.

The strong performance of DOGE this week underscores the memecoin phenomenon in 2024.

There have been extensive discussions about the value that these assets bring to the ecosystem. Vitalik Buterin, in a blog post dedicated to the phenomenon, stated that quality and fun projects contribute positively to the ecosystem and even the world around them. Arthur Hayes went further by affirming that “The chains that can support this culture are going to be the chains that have value.”

Leaving aside these important questions, the truth of the matter is that memecoins have been a driving force within crypto in 2024.

The only two assets in the top 20 that are delivering triple-digit returns are SHIB (+160.6%) and DOGE (+114.8%). CoinGecko lists six assets boasting a fully-diluted market capitalization of over $1 billion and 13 above the $500 million threshold. A meaningful amount of on-chain activity is related to these tokens.

And as usual in crypto, liquidity trends can provide further insight than just looking at price action.

If there is one indicator that is more impressive than the price appreciation of memecoins it might be the increase in their spot traded volumes. As the chart below shows, the top memecoins used to trade on average less than $500 million per day in January 2024. This figure jumped over 10x to $5.8 billion in March 2024. That is more than five times the growth in trade volume registered in BTC and ETH.

Although April has shown a decrease in volumes, which was the case for the market in general (more on that below), the top memecoins are still trading a respectable $3 billion per day on average. DOGE, PEPE, and WIF have been the main winners in volume market share at the expense of BONK, MEME, and SHIB.

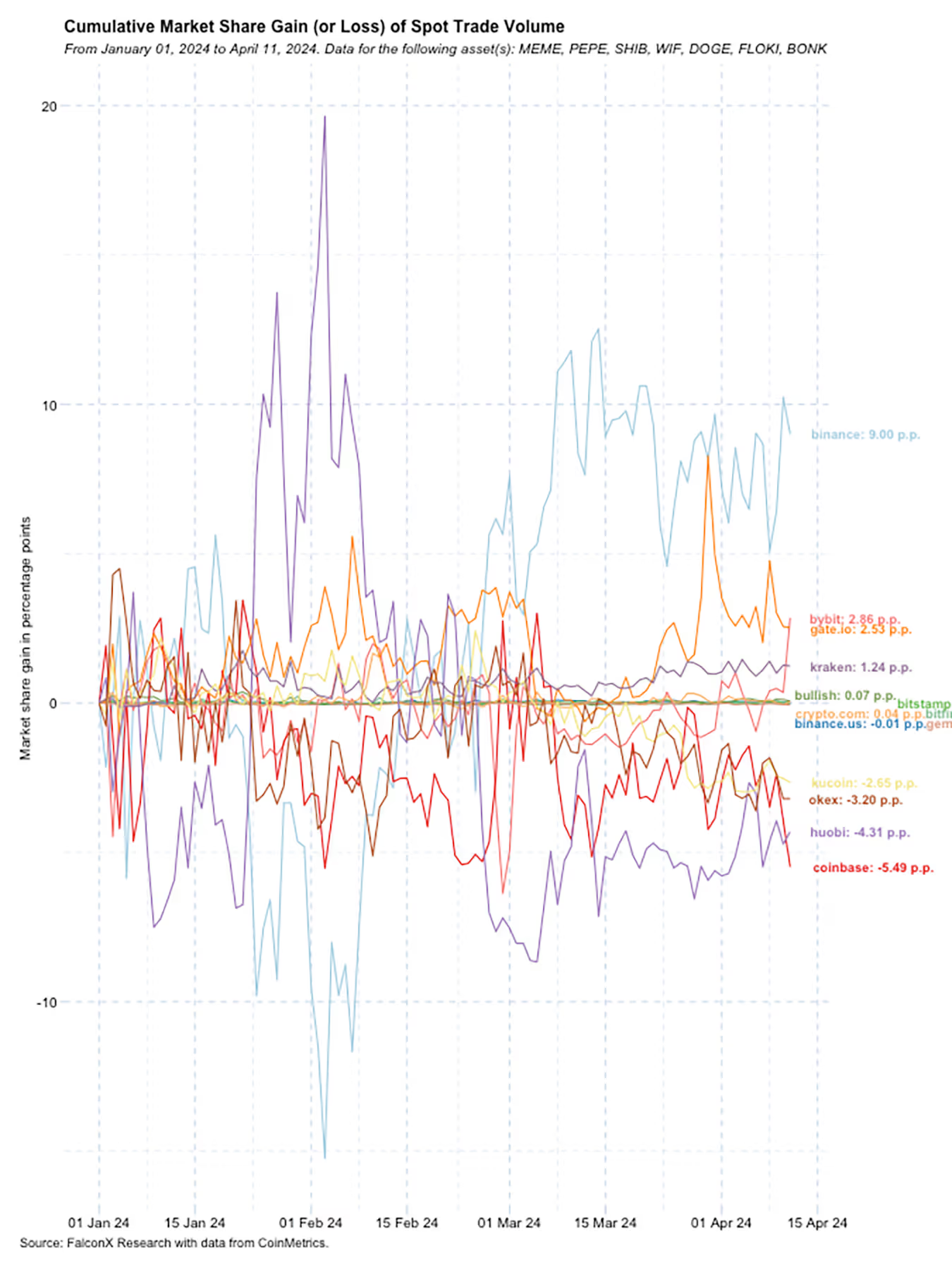

From an exchange perspective, Binance has been the main market share winner while Coinbase the main loser for those assets in 2024, especially after early March. This suggests that recent memecoin trading activity has been led by non-U.S. markets.

If volume trends have been dwindling somewhat in tandem with prices over the past month, depth of market remains on firmer ground.

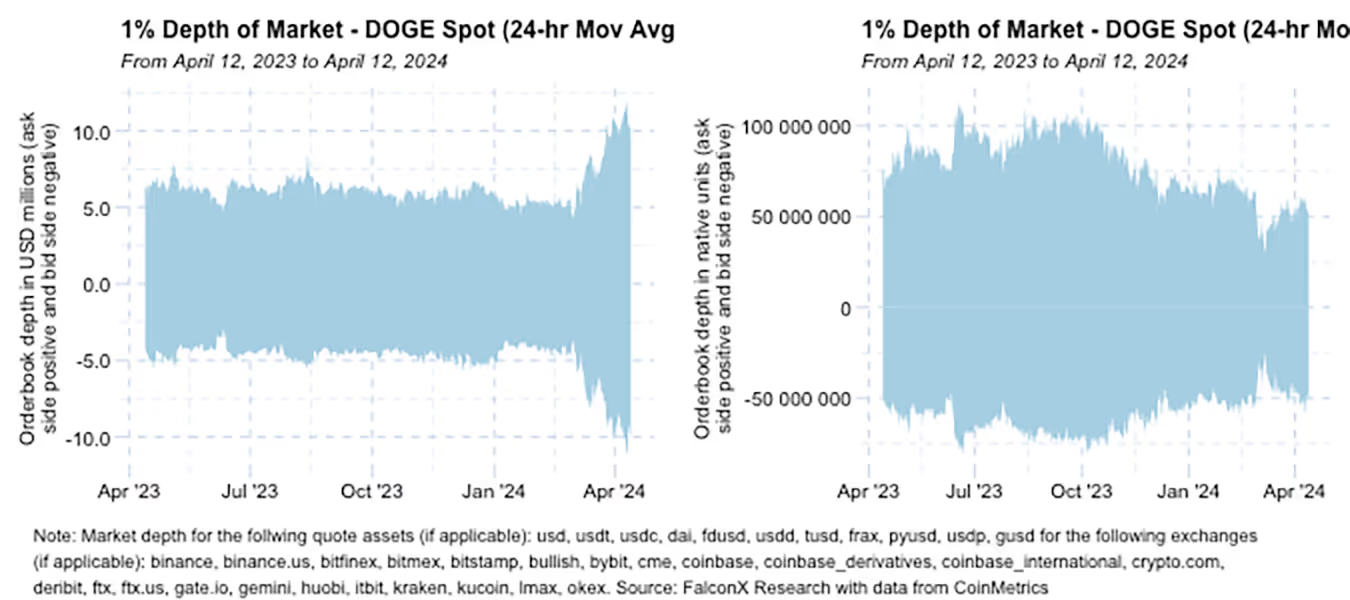

As the chart below shows, the 1% orderbook depth for DOGE and SHIB, the two largest assets in the space, is now at $10 million and $4 million on each side of the book, respectively.

These levels are very respectable for alts liquidity. For reference, SOL has a market depth of roughly $20 million. Such increased volumes coupled with market depth are not that common and have traditionally happened to assets believed to have staying power, such as SOL recently.

All in, if the price and volume trends show a tired market in the short term, market depth is showing that memecoins could have more staying power than some expect.

According to data from Artemis, Coinbase’s blockchain Base is not clocking DEX volumes of over $400 million and fees of over $500k per day, much of that driven by memecoin activity.

Even the bitcoin ecosystem might see a rekindle in memecoin activity. The Runes protocol, developed by Ordinals’ creator Casey Rodarmor, is launching after the halving at the end of April and will make memecoins transactions on Bitcoin much more efficient.

For better or worse, memecoins are likely to remain a topic of conversation in crypto circles for a while.

Other Top Trends We're Watching

FalconX Trading Desk Color: Flows came primarily from different directions across investor personas over the past week. Crypto hedge funds and VCs have been net sellers over the past two weeks, prop trading desks 50/50, and retail aggregators net buyers. BTC continues to dominate volumes across our desk, as it recently traded over 4x more than ETH. BTC flow was again firmly on the buy side (64% of total flow), as it has in seven over the past eight weeks. ETH activity was also primarily on the buy side, but only slightly so (52% of total flow). Activity in alts remains concentrated in relatively few names, such as SOL (26% of the total flow from the buy side), FTM (54%), AVAX (57%), and NEAR (36%).

BTC and ETH Volumes So Far in April Show a Significant Reduction from March: Crypto volume has traditionally been a reliable confirming indicator of overall market direction. The robust growth in traded volume that accompanied the price rallies of January 2024 and October 2023 gave confidence that there could be more to come, as we highlighted in the past.

However, crypto volumes shrunk significantly for the first time in the past five months. Since the Easter holiday week, volumes have been down about 50% and have since recovered only about 30% lower than the peaks registered in March.

Could this trend shift in spot traded volume presage a shift in the market's direction? Perhaps that means something for the short term, but we are not changing our positive stance over the medium and long term.

Two main reasons suggest taking this shift with a grain of salt.

First, the comparison base in March was exceptionally high. BTC spot daily volumes, for example, increased from less than $1 billion at their lowest point in 2023 to over $30 billion in March. Out of the top 20 highest-ever prints, half of them took place last March.

The other reason is that this shift is still too recent. There was a brief drop, albeit much less pronounced, in volumes in early 2024 that proved temporary.

At any rate, it is once gain time to monitor crypto spot volume trends.

Crypto VC Capital Deployment Increases for the Second Straight Quarter: The volume of new capital raised in new rounds announced by crypto startups in Q1 2024 increased by 11.0% over the previous quarter to $2.7 billion. Although this number is still a far cry from the numbers achieved at the highs of the previous bull market, this marks the second consecutive quarter of growth after seven straight quarters of declines starting in Q4 2021.

March and February of 2024 were the two best months ever regarding the number of deals closed, and we are starting to see activity among raises above the $50 million mark.

While EigenLayer's $100 million funding round led deal activity in February, Optimism led the charge in March with an $89 million private token sale. Zama, a cryptography firm focused on FHE (fully homomorphic encryption) applications, raised $79 million and scored the second-largest deal of the Month. Four other firms raised more than $50 million: Berachain (initially announced at $69 million and later raised to $100 million), Figure Markets ($60 million), Succinct Labs ($55 million), and Eclipse ($50 million).

Have a great weekend!

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd. nor Banzai Pipeline Limited service retail counterparties, and the information in this material is NOT intended for retail investors. This material is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this material is not and should not be regarded as investment advice, investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over the counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a Swap Dealer with the U.S. Commodities Futures Trading Commission and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is licensed by the MFSA as a Class 2 Crypto-Asset Service Provider (Regulation (EU) 2023/1114). It is also licensed as a Financial Institution (Cap. 376) exclusively for EMT payment services.

"FalconX" is a marketing name for the FalconX Group and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.