Upcoming Policy Shift to Mark Crypto's True 2025 Kickoff; Turnover Rebound Expected

Crypto markets are experiencing unusual calm as 2025 begins, with thin volumes and range-bound trading masking building anticipation. All eyes are on next week's administrative transition, which could unlock a wave of positive regulatory changes and reignite trading activity across both institutional and retail segments.

The crypto market's relative tranquility in early 2025 feels like the proverbial calm before the storm, with next week’s positive catalysts likely to energize what has been a flattish market.

Excitement is quickly building around a more favorable regulatory and policy environment for crypto effectively starting as the new administration takes office next week. BTC is reaching the top of its trading range it has been over the past couple of months. The flagship crypto asset took a brief but notable dive below $90k before staging a quick recovery.

Beyond a fleeting panic over potential U.S. government token sales, macro factors have been steering crypto price action over the past few weeks. This comes on the back of the 10-year yield’s steady upward march since October, pushed by a cocktail of long-term uncertainties: fiscal policy, trade dynamics, and election-related concerns. Meanwhile, stubborn inflation has forced markets to dial back their rate-cut optimism for 2025, now pricing in just one cut instead of several. The December CPI, however, print offered a glimmer of hope, coming in slightly better than expected and reigniting hopes of multiple cuts.

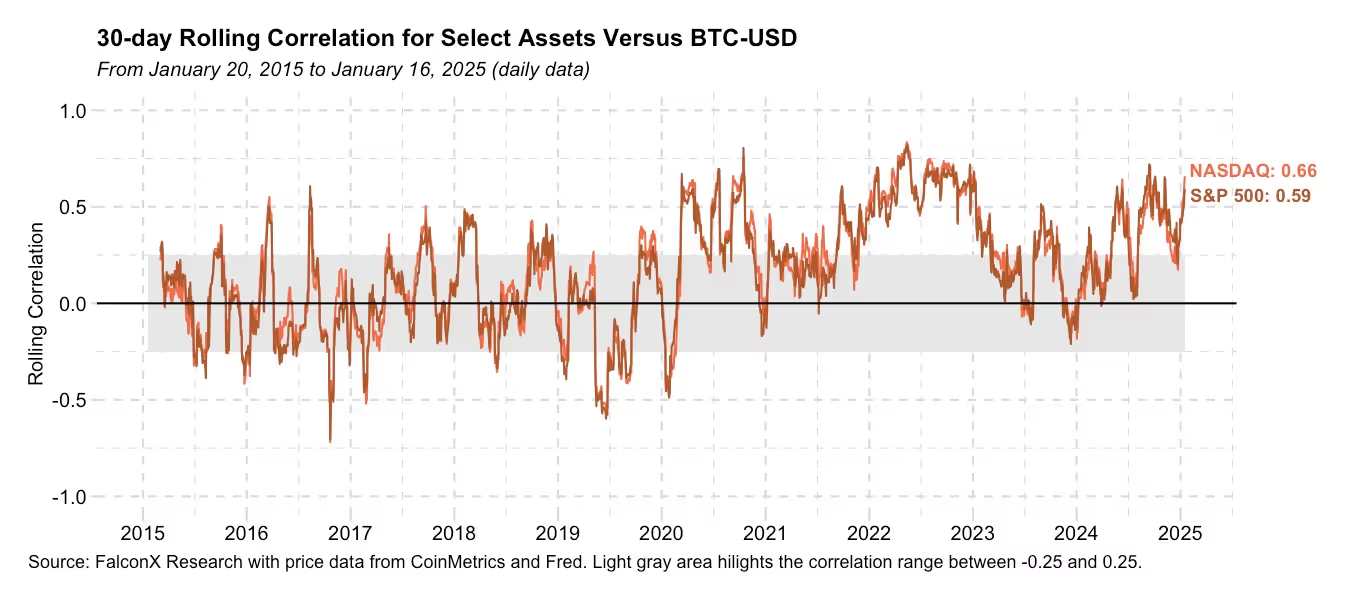

The correlation between BTC and major equity indices (S&P 500 and Nasdaq) has surged from 0.25 to around 0.60 in just a couple of months. As the chart below illustrates, these correlation levels are approaching the peaks we witnessed in 2024, suggesting crypto's industry-specific topics temporarily took a back seat to broader market forces.

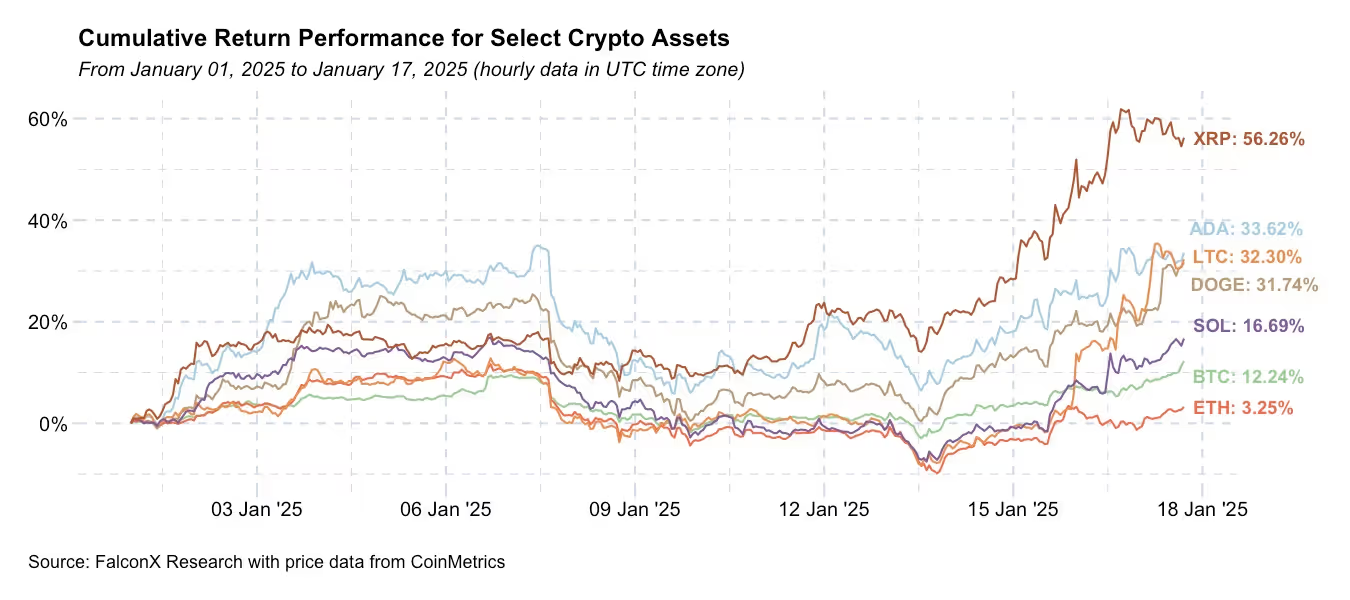

The relentless march higher of legacy Layer-1s like XRP, ADA, and LTC has been more surprising. As we noted in a previous analysis, this rally bears all the hallmarks of retail-driven enthusiasm. Part of the recent trigger is related to rumors that XRP could be included in the potential strategic reserve, but there’s reason to believe these are unlikely to materialize.

It’s important, however, not to read too much into market signals year to date given the notably thin trading conditions.

Crypto markets are not yet fully back from their holidays, with trading volumes painting a particularly telling picture. Current crypto turnover stands at a sobering 25-35% below what we witnessed in early December's bustling sessions.

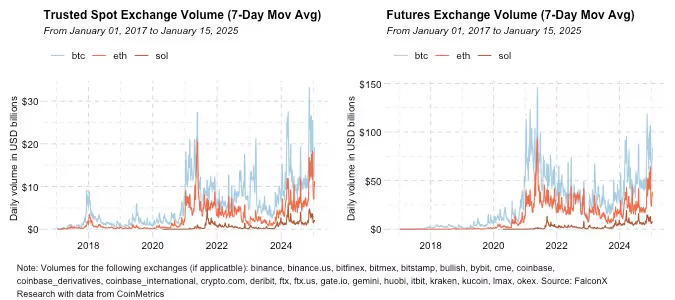

For perspective, BTC spot trading volumes in December regularly surpassed $30 billion - even touching an impressive $50 billion peak on one particularly active day. In contrast, 2025 has yet to see a single session break through the $30 billion threshold.

This volume drought isn't limited to Bitcoin alone. As the chart below illustrates, the same pattern of subdued activity is playing out across other major cryptocurrencies, affecting both spot and futures markets. Feedback from our trading desks suggests that this trend is also notable among institutional crypto circles.

But these lackluster liquidity dynamics are very likely to change starting next week. Expectations are running hot for the potential regulatory unlocks coming once the new administration takes office on Monday. Trading volumes are ready to surge as months of pent-up anticipation finally meet concrete policy action.

While the exact sequence of regulatory changes remains uncertain, market signals are flashing increased optimism. The most liquid BTC strategic reserve prediction market has climbed to 40% probability - a notable jump from last week, though perhaps overly optimistic. More realistic early wins could come from the SEC: a swift reversal of SAB 121 to ease bank crypto custody, a review and potential freeze of non-fraud litigation, and perhaps a bit later on ETF-related improvements like allowing in-kind creations and redemptions for crypto ETFs and the allowance of staking for ETH spot ETFs.

There is good reason to expect important market shifts starting next week.

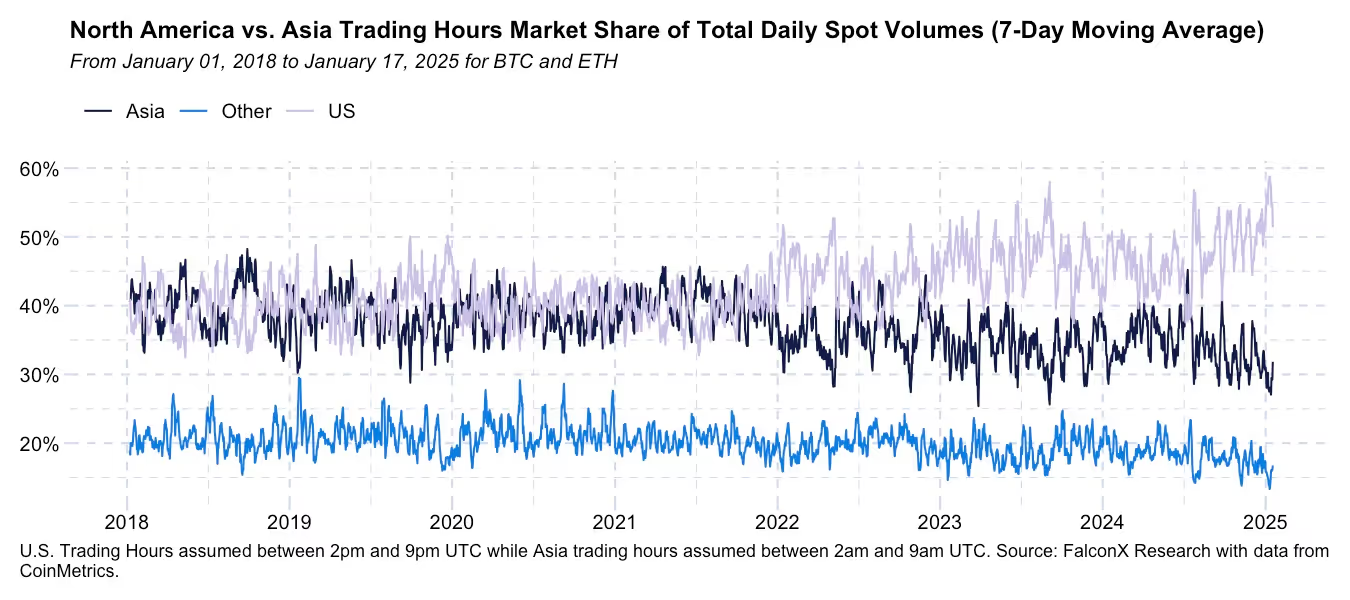

The centrality of U.S.-related market topics is already clear in market dynamics even if most of the trading volume still takes place in offshore markets. As the chart below shows, the share of global spot BTC and ETH trading during U.S. trading hours is brushing an all-time high of almost 60%.

Liquidity trends could once again serve as a compass for confirming this potential new market phase. The playbook that served us well through market recent regime changes should prove valuable here as well. We'll be watching for the first signals in volume patterns across spot and derivatives markets, followed closely by order book dynamics to gauge market sentiment.

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd. nor Banzai Pipeline Limited service retail counterparties, and the information in this material is NOT intended for retail investors. This material is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this material is not and should not be regarded as investment advice, investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over the counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a Swap Dealer with the U.S. Commodities Futures Trading Commission and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is licensed by the MFSA as a Class 2 Crypto-Asset Service Provider (Regulation (EU) 2023/1114). It is also licensed as a Financial Institution (Cap. 376) exclusively for EMT payment services.

"FalconX" is a marketing name for the FalconX Group and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.

.jpg)