To Approve or Not to Approve? Point/Counterpoint Perspectives on the Upcoming Spot ETH ETF Decision

Market odds of approval in May are dwindling, but we’ll likely see an ETH ETF approval over the next 12-18 months

Written with FalconX General Counsel Purvi Maniar and originally published on Coindesk.

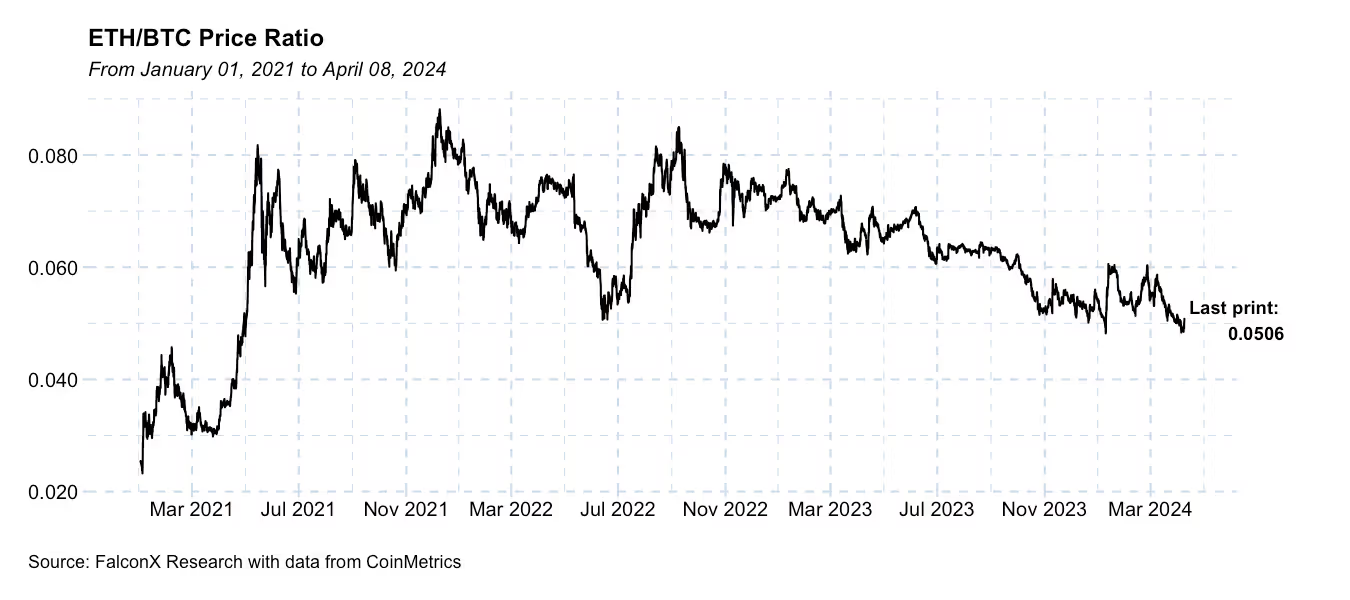

A notable theme in the ongoing bull market is Ethereum's (ETH) underperformance, which has deepened over the past few weeks due to increasing skepticism about the odds of the spot ETF decision being approved by the SEC on May 23.

The ETH/BTC price ratio just dipped below 0.05, marking its lowest point since Ethereum began gaining traction as an institutional-grade asset in May 2021.

As late as February of 2024, the market was anticipating a green light from the SEC on May 23 following the spot BTC ETF approvals in January. This view has been turning sour over the past few weeks, to the point that the current prevailing view is a denial by the SEC. The discount to NAV on the closed-ended Ethereum trust ETHE, a proxy for the market-implied likelihood of denial, increased from 8% to over 25% in the past month.

Spot ETH ETFs will remain a topic of conversation for the markets as we approach May 23rd and the next few quarters if they are not approved by then. Let’s explore what the main arguments for and against approval are.

Point (the Consensus View): The Case for Denial

Over the past few weeks, the market has been trending toward expecting the SEC not to approve a spot ETH ETF at the end of May. This line of argument hinges on a few points.

First, there has been virtually no engagement between the SEC and issuers less than two months from the deadline. This contrasts sharply with the spot BTC approval process, where a back-and-forth was publicly visible through a flurry of amendment filings in the months leading to the approval. Contrary to what some have argued, the recent public call for comments is standard and should not be construed as engagement from the regulator.

Another critical factor is the view that the SEC approved the spot BTC ETF approval only begrudgingly. The use cases that ETH currently enables, such as Decentralized Finance, may make the review process for the SEC more fraught with complexities.

One such nuance is the continued lack of confirmation by the SEC on whether ETH is or is not a security despite its sister agency CFTC claiming it is a commodity.

Counterpoint: The Case for Approval

Some investors and analysts are making persuasive arguments against the mainstream narrative of denial, even if they are not necessarily calling for a May approval.

As Grayscale’s Chief Legal Officer suggested, the absence of engagement does not necessarily predict the outcome. Contrary to the BTC spot ETF approval process, there isn’t much to discuss now. Most of the back-and-forth between the BTC ETF issuers and the SEC was around the redemption mechanism (cash versus in-kind), which is already a settled issue.

The one area where there may be room for discussion would be whether the SEC would allow native staking of ETH. Despite the push by some issuers, the broad view is that staking is unlikely to be allowed initially. That’s a straightforward issue the SEC can resolve at a potential rule-change approval or later when it reviews the S1 (or S3) forms required before launch.

In addition, a denial would likely be met with litigation from the applicants, and there is strong evidence that the issuers would have a strong case. The spot BTC ETF approval hinged on the high correlation between the spot BTC and CME BTC futures markets According to analyses by Fidelity, Bitwise, and Coinbase, the same level correlations also exist for ETH, making it an unlikely issue for the SEC to raise again.

Looking Ahead

The spot BTC ETF approval in January did not come by a wide margin. Two of the five SEC commissioners voted in favor, two against, and Chair Garry Gensler tipped the scale. Gensler’s may be the casting vote again for the spot ETH ETF decision.

Out of the over 575 ETFs Blackrock has filed as an issuer, only one was denied by the SEC. Will the spot ETH ETF be the second? The market is attributing relatively high odds of denial, but if there’s one thing crypto investors have learned over the years, it's that last-minute surprises should never be ruled out.

Going beyond this approval cycle ending on May 23rd, it seems only a matter of “when” and not “if” for spot ETH ETFs to launch in the U.S. market. The arguments for approval will likely outweigh the ones for denial over time. As a result, even if approval does not come by May 23rd, the chances of a greenlight over the next 12-18 months seem high.

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd., nor Banzai Pipeline Limited service retail customers, and the information on this website is NOT intended for them. The material published on this website is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this website is not and should not be regarded as investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

No discussion of a particular company or product shall be considered an endorsement of such company or product. Past performance is not indicative of future results. FalconX, and its affiliated parties, including 21shares, may hold positions in, act as a market maker for, or otherwise have a financial interest in, assets discussed herein, and may benefit from any price movements or transactions involving the subject company. This may change without notice. Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory, and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over-the-counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a swap dealer with the U.S. Commodities Futures Trading Commission (CFTC) and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is licensed by the MFSA as a Class 2 Crypto-Asset Service Provider (Regulation (EU) 2023/1114). It is also licensed as a Financial Institution (Cap. 376) exclusively for EMT payment services. FalconX’s complaint policy can be accessed by sending a request to complaints@falconx.io

"FalconX" is a marketing name for the FalconX Group and its affiliates. Availability of products and services can be subjected to jurisdictional restrictions and operational capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.