The Drivers Behind Hyperliquid’s Next Phase: HYPE ETFs, HIP-4 Outcome Markets, Priority Fees, and its USDC Agreement

HYPE ETF launches, USDC coming on as an aligned quote asset, and new HIP-3 and HIP-4 markets stand to shape Hyperliquid's next stage of growth.

.png)

With traction in Hyperliquid’s permissionless perp markets (HIP-3), the next pieces of potential growth are falling into place. Recent HYPE spot ETF launches are helping improve distribution and investor access to the HYPE token, with strong initial flows and volumes, pointing to pent up demand. HIP-3 markets such as pre-IPO markets are driving awareness and activity, while the introduction of priority fees stand to deliver incremental protocol revenue and add greater token utility. Furthermore, HIP-4 outcome markets launched on mainnet on May 2, 2026, and stand to throw Hyperliquid in the ring with Kalshi and Polymarket. The announcement of USDC becoming an aligned asset through formal support from Coinbase and Circle could also add up to $160M of annualized revenue to the protocol, per our estimates. The combination of these developments have helped lift the HYPE token higher, clearing its ATH from September 2025 on May 21, according to data from CoinGecko.

HYPE ETFs and DAT Activity

Recently launched HYPE ETFs and a renewal of activity from HYPE DATs could serve as incremental drivers of flows into HYPE. The ETF launches from 21Shares (a FalconX affiliate) and Bitwise have seen an aggregate $53M of inflows as of May 20, 2026, per data from Bloomberg, notable considering they have only seen a few trading sessions (THYP was the first HYPE spot ETF to launch on May 12).

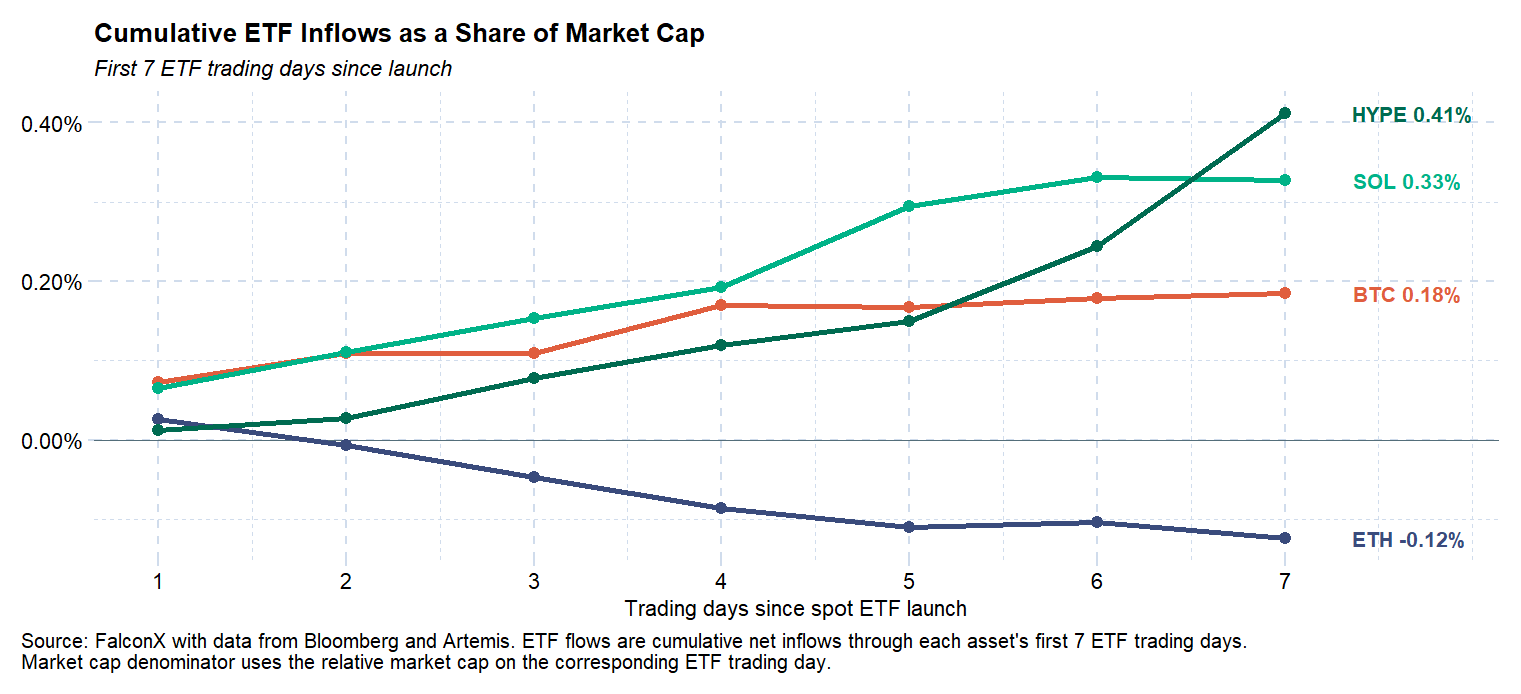

The HYPE ETFs stand out in several areas. Cumulative HYPE ETF inflows as a share of HYPE market cap have grown to 41 bps after 7 trading days, better than at the same point for the BTC, ETH, and SOL ETF launches (0.18%, -0.12%, and 0.33% respectively).

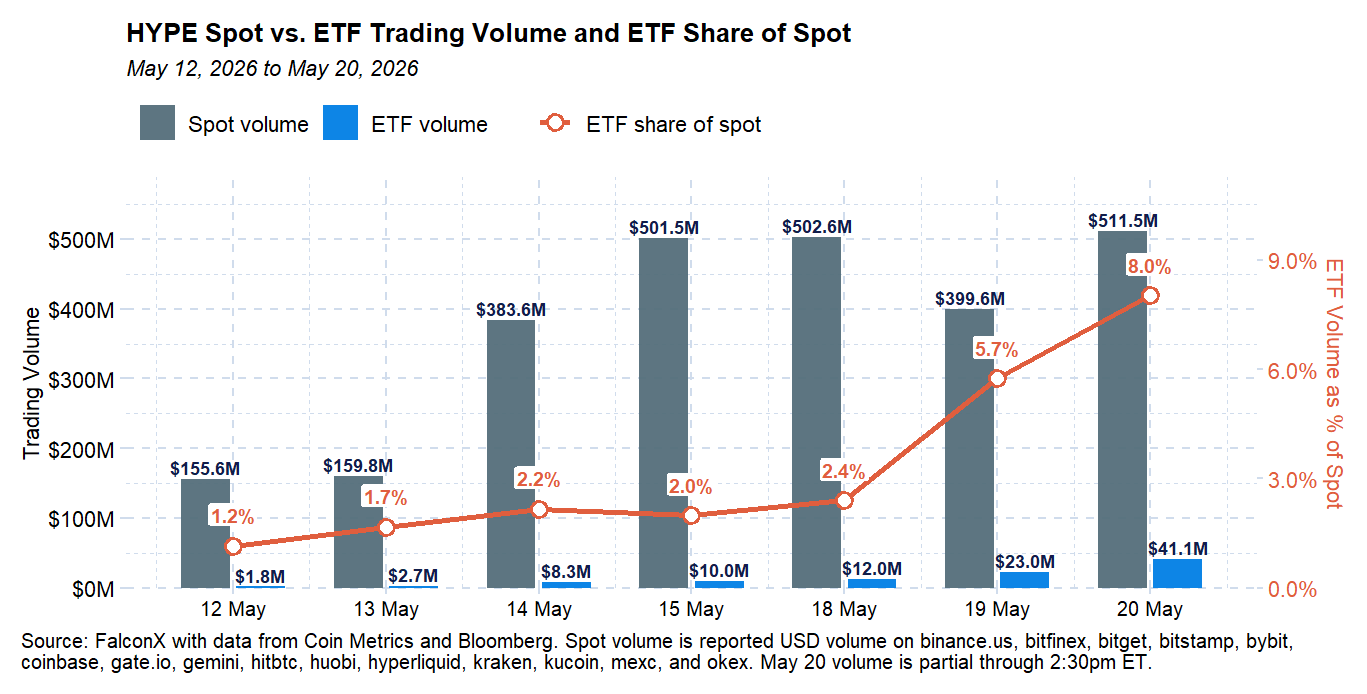

The other notable area for the ETFs is in its volumes. HYPE ETF volumes saw a combined $41M on May 20, which compared to $511M of spot HYPE volumes, per data from Bloomberg and Coin Metrics. This means that ETFs as a share of daily HYPE spot volumes have climbed to an impressive 8.0% as of May 20. On that day, THYP saw volumes of 14x its launch day volumes.

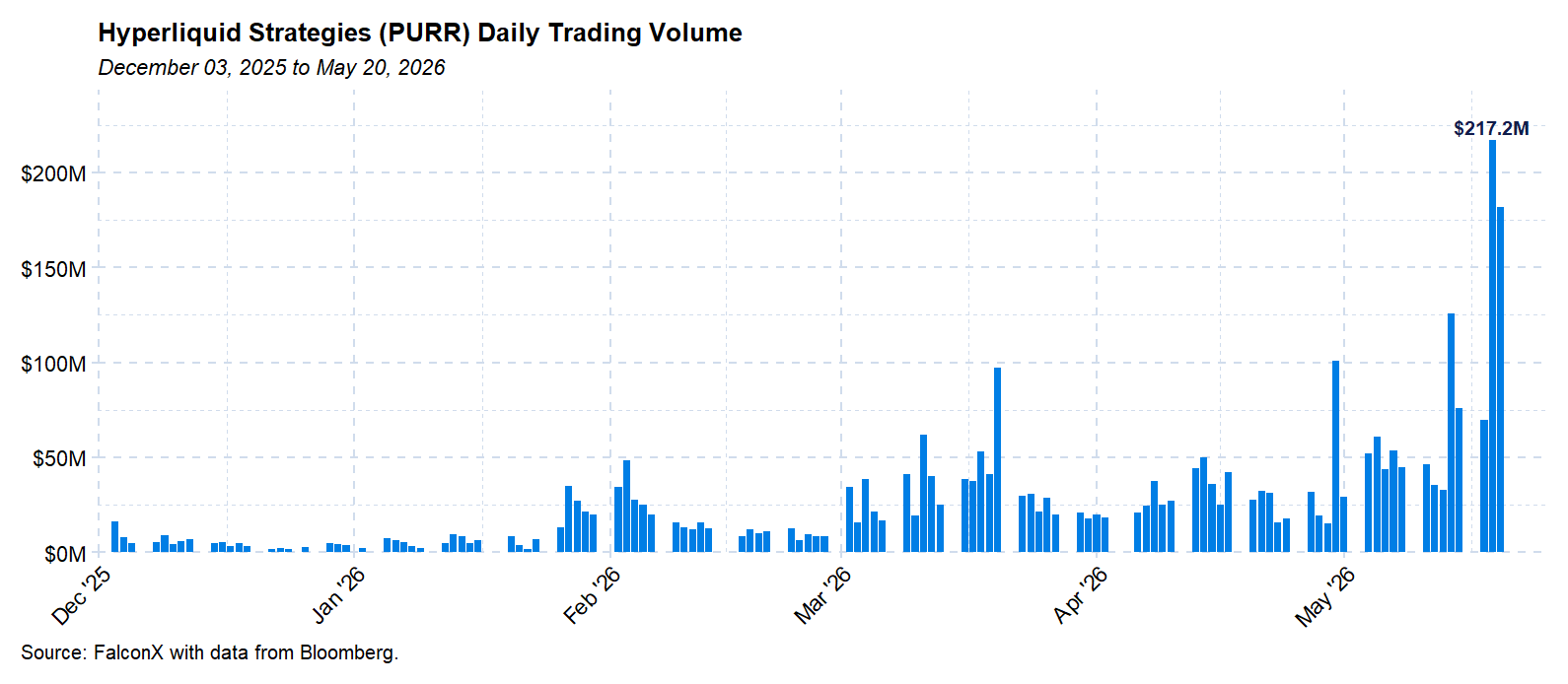

On the DAT front, Hyperliquid Strategies (PURR) saw its largest ever trading day on May 19 ($217M), potentially indicating growing investor interest in exposure to HYPE. Considering data provider Artemis showed PURR’s fully diluted mNAV to be 1.17 as of May 20, it is possible they have been tapping capital markets to fuel further HYPE accumulation. DATs now hold 9.5% of HYPE supply per Artemis, ahead of their respective share of ETH (5.5%) and BTC (5.1%).

If Hyperliquid is able to break into the mainstream, these access vehicles could be key to bringing in new, non-crypto native investors to HYPE.

HIP-3 Recap

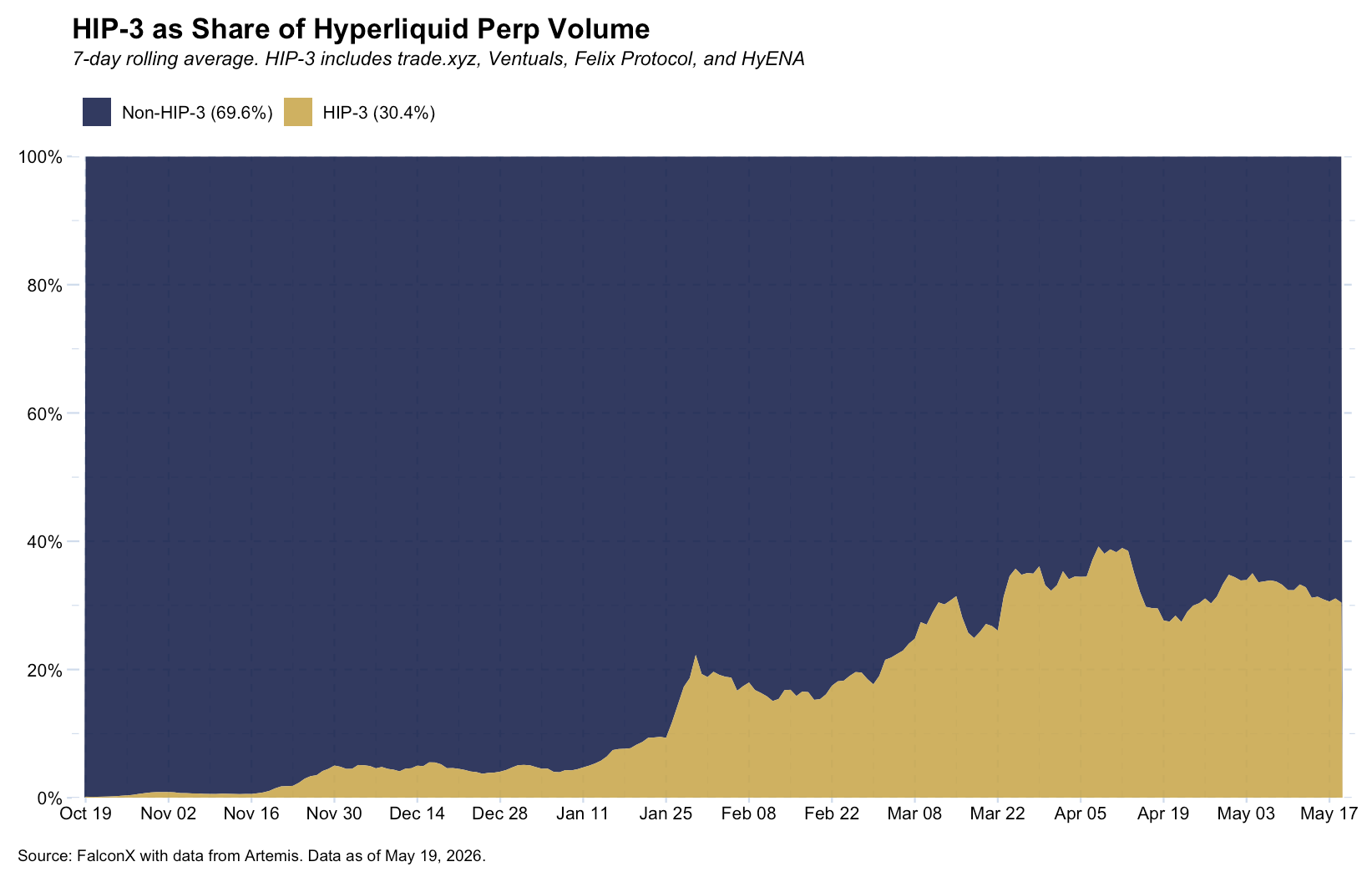

The combination of growth mode (90%+ trading fee reductions) and a broad array of RWA instruments (equities, indices, commodities, forex) has helped propel HIP-3 trading activity since launching in October 2025. Hyperliquid continues to benefit as one of few venues allowing users to trade assets 24/7, which positioned it to capture activity from the metals rally earlier in Q1 as well as from oil volatility around the Iran conflict. With volatility in those assets subsiding, HIP-3 activity has plateaued in recent weeks, with 7D HIP-3 volumes currently at 30% of platform volumes and HIP-3 open interest sitting close to records at $2.5B, per data from Artemis.

Fees from these markets remain only 6% of Hyperliquid fees, signaling the impact of the trading fee reductions, painting a bull and bear case with these markets. Removing the fee discounts on these markets could meaningfully add to protocol revenues, albeit at the cost of potentially losing some volumes which could impact the growth story.

Pre-IPO Markets

Originally spearheaded by HIP-3 deployers such as Ventuals, these are making waves amongst anticipation for upcoming AI IPOs. Three recent developments are noteworthy.

The Cerebras (CBRS) IPO put the spotlight on the CBRS HIP-3 market, which saw relatively strong traction, with researchers pointing to price discovery occurring on-chain.

Furthermore, developments around Anthropic (such as its move to clamp down on unauthorized secondary share sales, Karpathy joining the firm) led to awareness of how traders were pricing in the news on Hyperliquid.

In addition, the SpaceX HIP-3 market saw strong activity after SpaceX set its IPO for June 12, 2026, with open interest of over $30M as of May 19, 2026.

The narrative around the pre-IPO markets isn’t just price discovery. It is how Hyperliquid is meeting demand for markets that traders may not be able to access otherwise.

Outcome Markets (HIP-4)

HIP-4 enables the launch of permissionless binary outcome markets, which are fully collateralized contracts that settle to 0 or 1. These follow a similar model to the markets offered on prediction markets such as Kalshi and Polymarket.

The key unlock for traders is that they will be able to access event contracts 24/7 on the same platform (Hyperliquid) as their spot and perp positions, something not possible previously. The potential for cross-margining these positions would enable significant capital efficiency.

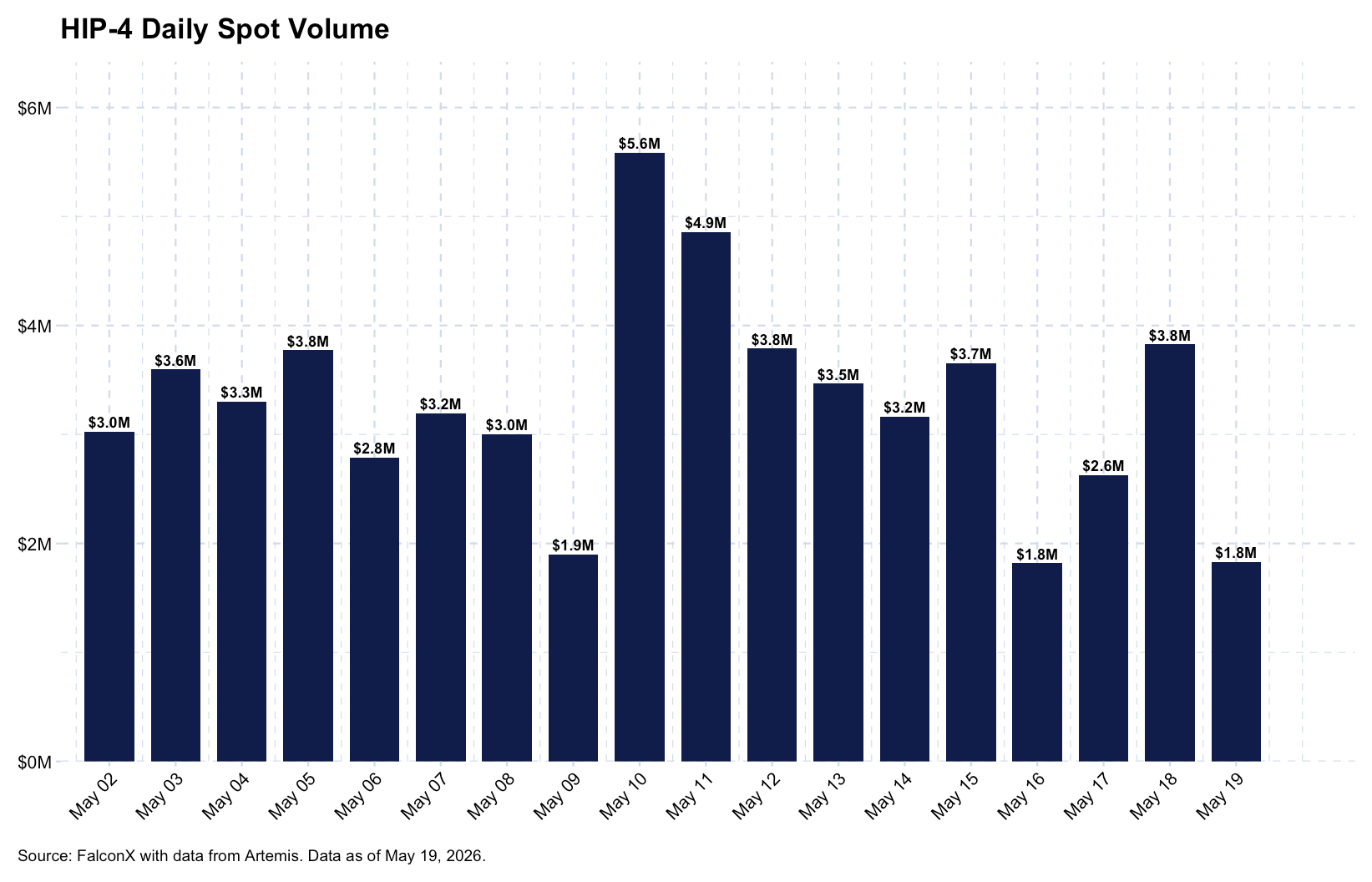

Outcome markets went live on mainnet as a limited-feature initial release on May 2, 2026. As of writing, there are only 2 markets on mainnet, both launched by the Hyperliquid team.

Fully permissionless HIP-4 market deployments are not yet live. When this is enabled, we anticipate it could see a flurry of launches from builders such as Outcome and Trade[XYZ], similar to the ramp up in markets with the HIP-3 rollout.

Given there are only 2 HIP-4 markets on mainnet, there has been limited traction so far, with average daily trading volumes of $3.2M as of May 19, according to data from Artemis. As the outcome market mechanics are validated and more markets are allowed to spring up, activity may grow with it. ‘Growth mode’ trading fee reductions are active on these markets already (currently set to 0 bps for both opening and closing positions on mainnet), which could help drive volumes, especially when compared to the relatively higher fee schedules of major prediction markets (these can be up to 175 bps of notional, which compares to the 4.5 bps and 7 bps base rate fees for Hyperliquid perps and spot, respectively).

How might HIP-4 markets evolve?

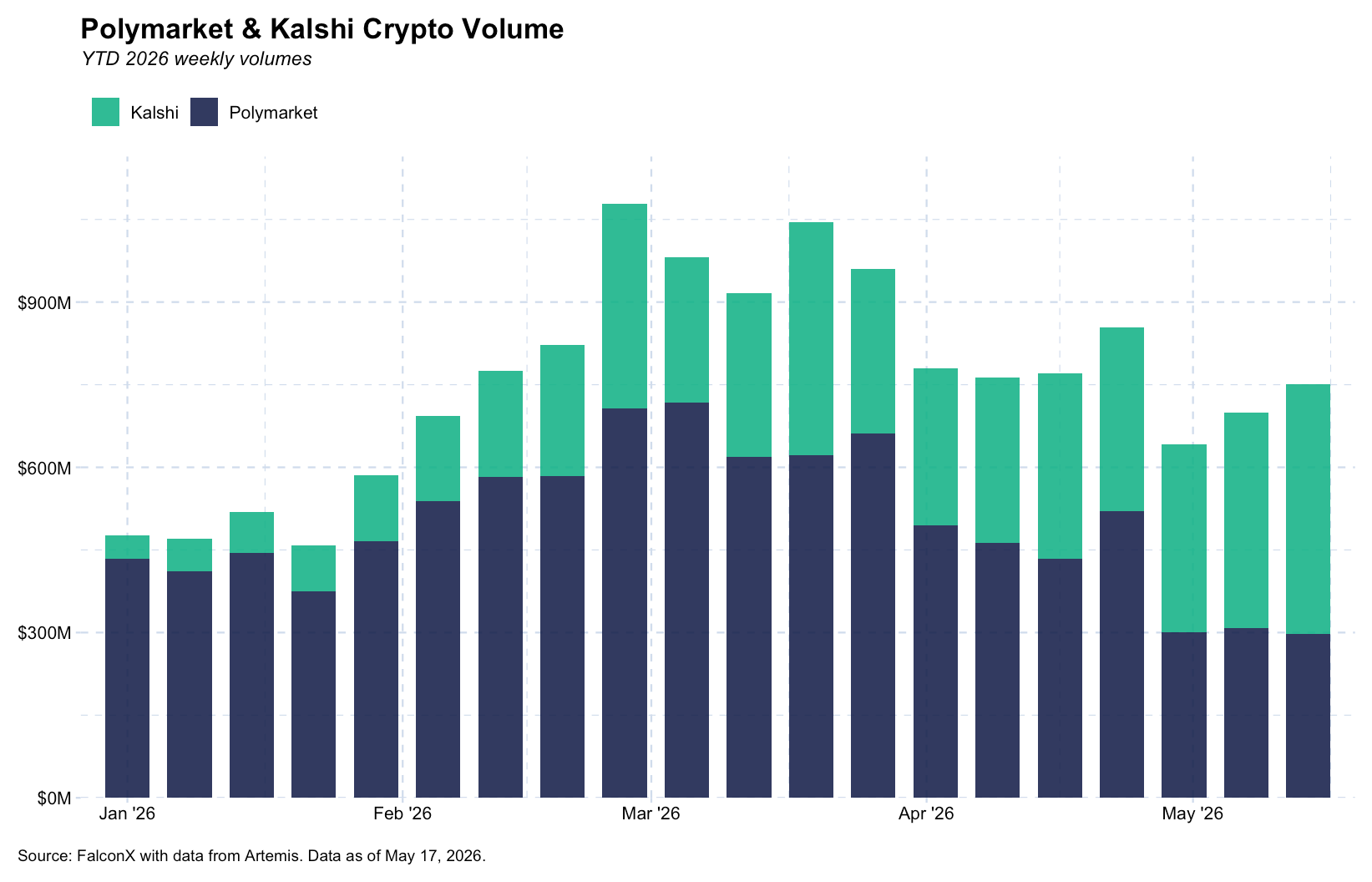

Looking at Polymarket and Kalshi for clues, the majority of volume is in sports-related contracts (60% and 76%, respectively, per Artemis). On Polymarket, 15% of trading volume for the week ending May 17, was in crypto-related contracts, such as the up/down markets, per data from Artemis. Financials (1%), Economics (1%), and Politics (16%) were smaller categories but arguably more relevant for Hyperliquid’s platform which targets traders rather than sports bettors. On Kalshi, crypto also made up a notable portion of volume (12%) over the same period.

Most of the incumbent prediction market crypto market volume is in the 5 and 15 minute markets, which can explain the relatively muted HIP-4 activity so far. In contrast, the 2 contracts on Hyperliquid mainnet are daily markets.

Given the current slate of markets on Hyperliquid (largely Crypto and RWA), we see the following categories as more likely to drive activity rather than sports. However, experiments with sports-related markets are ongoing on testnet, highlighting that builders may be weighing launching these.

- Crypto up/down markets

- Economics: central bank policy decisions, economic releases

- Financials: company earnings

- Politics: election outcomes, government decisions

Crypto-related contracts drove $750M+ of volumes last week across Polymarket and Kalshi. This area alone represents 2% of Hyperliquid’s current perp volumes, per Artemis. The real opportunity likely lies in the economic and financial categories, which have natural synergies with HIP-3 markets. Combining these with the rest of the Hyperliquid platform could make it easier for traders to express a range of views. For example you could pair a HIP-3 perps position on NVDA with outcome markets that it could miss/beat earnings.

The USDC Arrangement

On May 14, 2026, Coinbase announced plans to support USDC as an aligned quote asset (under the AQAv2 framework) as the treasury deployer, with Circle serving as the technical deployer responsible for CCTP and native cross-chain infrastructure. As part of this, Native Markets, the project behind the original aligned quote asset USDH, agreed to terms granting Coinbase the right to purchase the USDH brand assets.

Hyperliquid’s announcement on the matter stated that Coinbase would share the “vast majority of reserve yield revenue with the protocol”, which was clarified in the docs to be approximately 90% of cost-adjusted reserve yield revenue on their Hyperliquid supply. This is a notable win for the protocol as this rate is roughly double the prior rate under USDH (50% to the assistance fund).

Per the announcement, Coinbase and Circle have committed to stake HYPE per their respective deployer roles (treasury and technical deployer).The activation of AQAv2 is by validator vote, after both deployers have staked and sent the authorization transactions from the staking accounts. As of writing, the vote has not occurred yet, but Circle and Coinbase have already staked 500K HYPE ($30M) each, per Mlm onchain.

USDC was already the dominant quote asset across Hyperliquid, so this helps it retain its position on that front. Moreover, AQAv2 will be a requirement for quote assets to be listed against HIP-4 and validator-operated perp markets in the future, further improving the positioning of USDC on the Hyperliquid platform.

Unlike the original AQA framework, there is no trading fee or volume contribution benefit to AQAv2. Previously, there were 20% lower taker fees, 50% better maker rebates, and 20% more volume contribution toward fee tiers. This means Hyperliquid stands to retain more fees from its USDC markets.

HYPE TVL (USDC) is $5.1B as of May 19, 2026, according to data from DeFi Llama. Applying Circle’s reserve return rate of 3.5% from 1Q26 and the 90% that Hyperliquid captures results in up to $160M of revenues that the protocol could receive from this arrangement.

Priority Fees

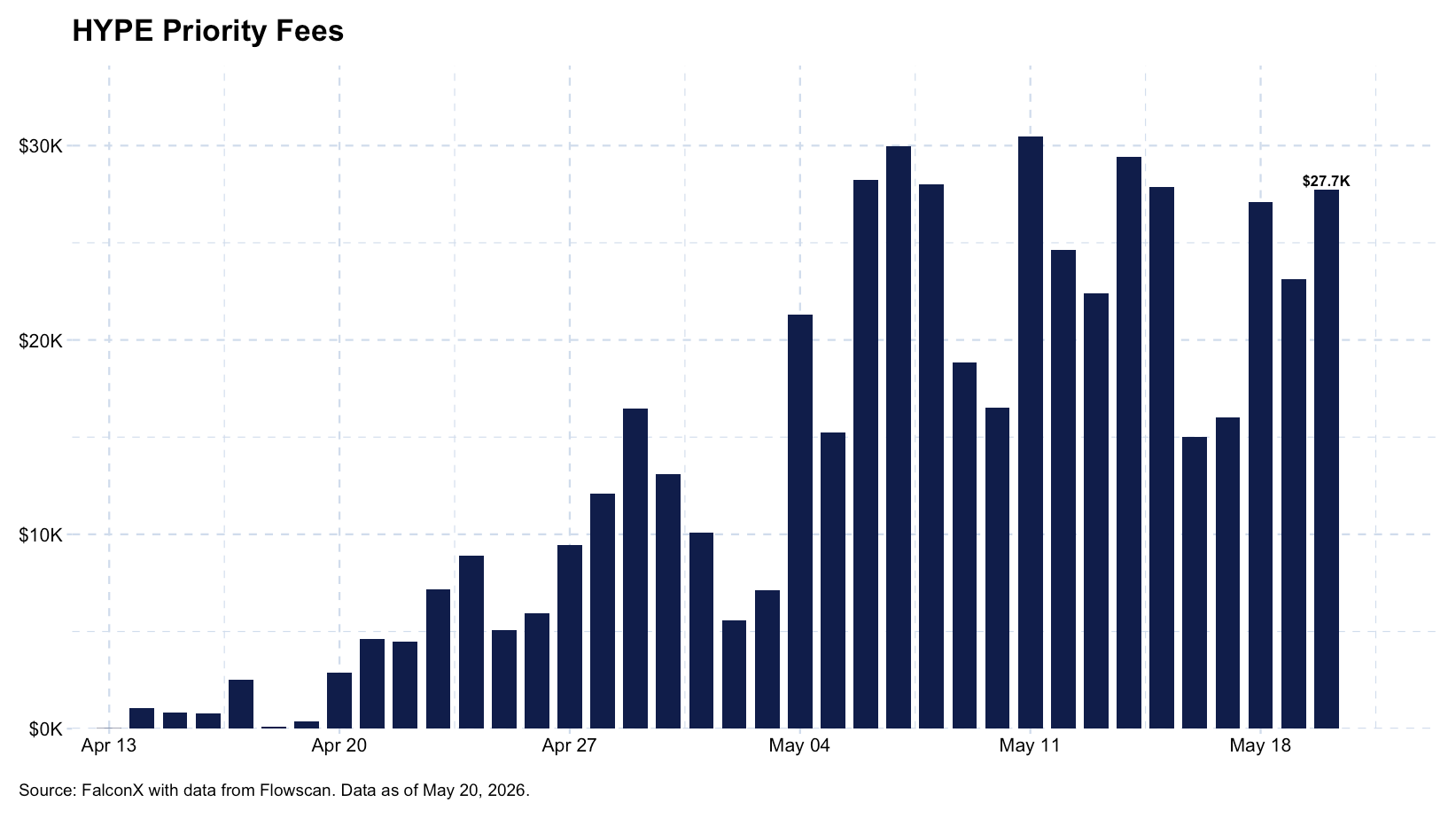

Hyperliquid launched priority fees on mainnet in April 2026. This allows traders to pay in HYPE to gain priority access to reading data or for submitting orders. For reading data, there are Dutch auctions run every few minutes, while traders attach a priority rate of up to 8 bps to orders, with higher rates getting priority. Cancels are prioritized before immediately executable orders. The fees are taken from a traders’ undelegated HYPE staking balance in HYPE, calculated as a percent of the filled notional, converted to HYPE at the spot mark price at the time of the fill.

This brings some tokenomics changes to HYPE. Priority fees are burned, adding another potential pathway to make HYPE deflationary. Traders who wish to pay for priority fees must have already acquired HYPE to pay for the fees, adding another demand sink.

DEXes are known to be major sources of MEV, so priority fees could be meaningful over time. Daily priority fees are still relatively low relative to HYPE’s overall platform fees but have been picking up since going live. For the week ended May 17, 2026, it saw around $166K in fees burned from priority fees, per data from Flowscan, around $8.6M annualized.

Regulatory Developments:

SEC Tokenized Stock DeFi Innovation Exemption

Bloomberg reported that the SEC plans to soon announce its innovation exemption for tokenized stocks. Notably, the SEC seems to be leaning towards allowing the trading of third party stock tokens on DeFi platforms, although these may not have voting rights or be eligible for dividends.

This could be the catalyst for broader integration of RWA on Hyperliquid. Already, its HIP-3 markets have proved popular, and adding spot equities on HyperCore or on the HyperEVM could unlock a wave of activity.

Potential for Regulatory Headwinds, or Partnerships

Bloomberg also reported that exchanges CME and ICE were calling on officials to regulate Hyperliquid, citing concerns over the potential for price manipulation. Punitive regulatory action could deliver speedbumps for Hyperliquid.

At the same time, it is possible these venues are also looking to defend their moat in the trading space, with CME set to launch 24/7 crypto futures and options trading on May 29.

It’s notable that ICE invested in Polymarket, another exchange trailblazer in new markets. It’s not out of the question that some of these exchange incumbents could strike similar partnerships with Hyperliquid, especially considering its deal with Coinbase and Circle demonstrates major companies are seeking to get involved with it.

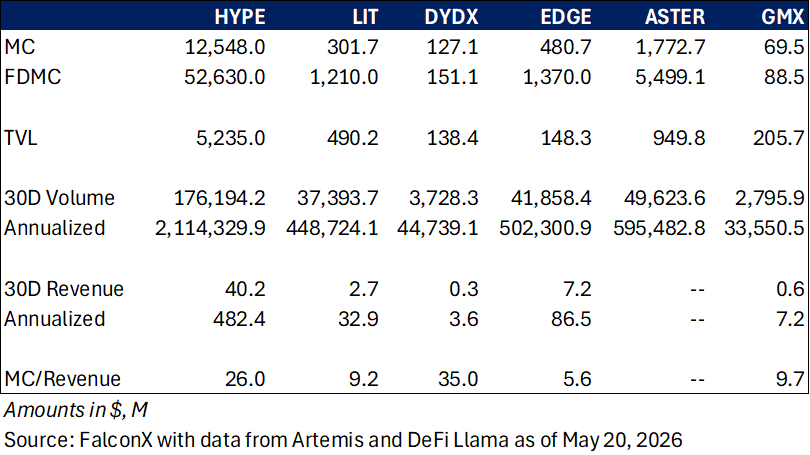

Relative Metrics

According to data from Artemis and DeFi Llama, HYPE remains firmly above its peers in terms of TVL, volume, and revenue generation. It is tracking annualized revenue of $482M, nearly all of which goes to token buybacks. Moreover the metrics do not reflect the potential for the $160M of incremental revenue from its USDC aligned asset arrangement.

On a multiples-basis, HYPE is trading at 26X MC/Revenue (P/E in this context), cheap to peer DYDX but rich to other perp DEXes such as LIT, EDGE, and GMX. If we consider the $160M of additional potential USDC-related revenue, HYPE would trade closer to 20X. This compares to P/E of around 24X and 26x for ICE and CME, respectively, as of data from May 20, 2026, per Bloomberg.

Takeaways

Hyperliquid is seeing traction as demand for its HIP-3 markets expands to include pre-IPO markets. With more HIP-4 markets on the horizon as well as the potential for more awareness and distribution through its ETFs, activity could grow, though such a trajectory is not guaranteed.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a swap dealer with the U.S. Commodities Futures Trading Commission (CFTC) and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is licensed by the MFSA as a Class 2 Crypto-Asset Service Provider (Regulation (EU) 2023/1114). It is also licensed as a Financial Institution (Cap. 376) exclusively for EMT payment services. FalconX’s complaint policy can be accessed by sending a request to complaints@falconx.io

"FalconX" is a marketing name for the FalconX Group and its affiliates. Availability of products and services can be subjected to jurisdictional restrictions and operational capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.