State of Bittensor: Subnet Adoption Trends, Network Mechanics, and Covenant’s Departure

Bittensor has seen major developments over the past year, including the launch of subnet tokens, a growing number of subnets (now 128), a halving, and changes to key mechanics.

This report is provided strictly for informational purposes and does not constitute investment advice. This report is co-authored by FalconX and SubnetStats (Pine Ridge Analytics LLC), with SubnetStats contributing subnet staking data and analysis. Please note that Martin Gaspar, Senior Crypto Market Strategist at FalconX and founder and owner of SubnetStats, will benefit if this publication results in increased interest in the discussed ecosystem.

More than a year after rolling out its market-led dynamic TAO (dTAO) model, Bittensor has grown to encompass 128 subnets. While many subnets are seeing traction and generating revenue, subnet participation remains relatively low amongst TAO holders with approximately 20% of TAO in circulation staked to subnets as of this writing. The ecosystem’s challenges were exposed in April 2026 when Covenant, an AI lab running several top subnets, suddenly departed the network. Its exit fueled concerns that successful startups might leverage Bittensor's emissions structure to bootstrap their own products before leaving the network for higher valuations elsewhere.

Despite these stresses, Bittensor maintains its status as the leading AI-focused token by market cap ($2.4B), generating $17M+ in annualized revenue, per Artemis, with several of its subnets now tracking $1M+ annualized revenue. As the network pushes toward fully decentralized governance by the end of 2026, Bittensor's key hurdle will be proving the long-term viability of its subnet model as these subnets continue to scale. In this piece, we review subnet mechanics and adoption, the risks presented in the ecosystem, and examine the path forward.

The Mechanics Shaping How Bittensor Operates Today

The Shift to DTAO

In February 2025, Bittensor implemented its dynamic TAO upgrade, which introduced subnet tokens. Each subnet has its own token paired with TAO in an AMM, and its token price initially determined emissions. Participants would stake their TAO to a subnet, increasing its value, and a higher subnet token price would signal that the subnet should receive a greater share of TAO emissions.

The upgrade was meant to transition the protocol to a market-led method of determining emissions to each subnet, versus a more centralized approach previously, where the top 64 validators by staked TAO determined a subnet’s emission. However, since this was stake-weighted, a far smaller group of validators effectively directed emissions. Moreover, this approach faced a scaling problem – with a growing number of subnets, it would become increasingly more difficult for a fixed set of validators to evaluate each one, and could therefore result in misallocation of TAO emissions. The new approach also had the effect of pushing subnets to scale and generate revenue to capture investor attention, helping to alleviate concerns that subnets were still in early stages and did not have much to show for the considerable emissions received (hundreds of millions of dollars’ worth of tokens annually).

TAOflow

In November 2025, the protocol updated its emissions mechanism to one called Taoflow, which measures the TAO being staked or unstaked to each subnet by market participants. It determines TAO emissions to subnets based on a subnet’s net TAO flows, based on a formula that uses the ~87D exponential moving average (EMA) of net flows, scaling slowly. A key motivation for Taoflow was that a subnet’s price reflects its ability to capture flows in the past and not necessarily the present, which could matter when determining emissions. For example, a subnet with a relatively high price could see sustained outflows from stakers but still receive a large portion of emissions. Taoflow was also implemented in part to solve concerns of established subnets farming emissions or “treasury” gaming strategies. In addition, Taoflow allows newer subnets to more easily compete for emissions when starting out with a relatively lower price.

This has resulted in potentially unintended consequences as subnets tailored their approach to bolster flows. For example, subnets with revenue can be rewarded with more emissions for buying back their subnet tokens to improve inflows, rather than allocating these funds elsewhere. Several of the largest subnets (Chutes and Lium, for example) are allocating all or most of their revenue to buybacks. Furthermore, under the Taoflow model, subnets can benefit by burning or reducing miner emissions to minimize selling outflows on their subnet. According to data from Taostats as of April 16, 2026, 67 of 128 subnets monitored were burning 99%+ of incentives, while only 20 subnets were burning 0% of incentives. Miners for these subnets may be participating without receiving any rewards which raises the question of how miners are being compensated and whether Bittensor is overpaying participants to begin with.

Taoflow is expected to see a change as early as mid May, where gross user flows (stakes minus unstakes) is replaced by net flows (considers mechanics such as emissions).

Deregistration

Subnet deregistration was reintroduced in September 2025 and aims to remove underperforming subnets, making space for new subnet registrations. When the network is at its subnet limit (currently 128 subnets) and a new subnet attempts to register, the subnet with the lowest EMA price amongst non-immune subnets is deregistered. In deregistration, a subnet’s tokens are effectively converted back to TAO and refunded to participants. New subnets have a four-month immunity period before being eligible for deregistration, with a minimum time of 2 days between subnet registrations/deregistrations. There have been several subnets deregistered since then, highlighting the competitive nature of Bittensor.

As an alternative to subnet registration, subnets can be sold in the secondary market. New subnet operators can benefit from a subnet’s established value (such as its emissions and a potentially deeper liquidity pool) and may be able to obtain a subnet at a lower cost than registering a new subnet through the protocol. It can also potentially reduce time to market for new entrants by skipping the registration process.

Understanding the TAO and Subnet Token Halvings

Post the dTAO upgrade, TAO has two kinds of halvings. The TAO halving reduces total daily TAO emissions by 50%. It cuts subnet TAO + subnet token pool injections in half, but participant (miner, validator, subnet operator) subnet token rewards remain unchanged. Pool injections are simply the liquidity in the pool. This supply change means a reduction in the growth rate of pool depth over time.

A subnet token halving sees the amount of subnet tokens rewarded to participants reduced by 50%. Similar to TAO’s first halving occurring at 10.5M tokens issued, the first subnet token halving will occur once 10.5M of its own subnet tokens are issued. This will occur subnet by subnet as their registration date and other nuances can influence their halving timeline. These halvings for some of the oldest subnets are estimated to occur as early as 2027.

Both TAO and subnet token halvings are supply-based (triggered at fixed supply thresholds), rather than at a specific block height. Therefore, these halving dates can change due to the amount of TAO that is recycled or other supply changes specific to subnet tokens, such as with the deregistration process. Moreover, a subnet’s token halving can take longer to occur if TAO emissions are lower for a given subnet as that means there are less subnet token injections in its pool (therefore its supply is lower).

Assessing Subnet Adoption

With subnet tokens now live for over a year (launched February 2025), adoption appears to be growing slower than expected. As of May 1, 2026, The percent of TAO staked to subnets stands at 21.3%, while the percent of TAO staked to root (Subnet 0) is 49.6%, per data from Taostats. This means approximately 70% of TAO is considered to be staking in some capacity.

This tells us a potential disconnect. Since the start of dTAO, the overall staking rate has remained unchanged at 70%. This may indicate that many participants prefer the flexibility to trade their TAO (30% of TAO sits in wallets, such as exchanges) rather than stake and that subnets may not be attractive enough to capture staking flows from this cohort.

What Root Proportion Indicates

A key variable to consider in subnet adoption is Root Proportion, which is the share of staking yield that goes to root (Subnet 0) holders. The root subnet does not have its own subnet token; staking to it instead provides exposure across all subnets and subnet token rewards are automatically converted into TAO. Root staking may be less risky than staking to subnets directly, as the principal amount staked is not exposed to volatility in a subnet token’s price. On the other hand, participants staking to subnets directly put their capital at risk by staking TAO into the token. The difference is the yield. Root stakers may receive yields of as much as 10% as of writing. In contrast, many of the top 10 subnets by price are capable of paying yields of 40%+ to stakers, while others are capable of paying 100%+, per data from Taoyield.

Currently, the root proportion is 15% on the largest subnet by market cap (Chutes). This means 15% of staking rewards goes to root stakers and 85% goes to those directly staking to the subnet. Root proportion declines over time as the network incentivizes users to stake to subnets to help actively set emissions. Root proportion varies by subnet and will vary depending on the subnet’s age (newer subnets will have a higher root proportion). Despite the faltering yields from root staking, it serves a key function to the protocol. It helps cut dead weight (root stakers auto sell the tokens, so the impact can be more pronounced on lower quality subnets with low demand). The impact on subnet prices helps the network churn out lower quality subnets over time.

Logically, one could infer that participation might follow the root proportion curve to keep up with the portion of yield paid to subnet stakers. This has not held up with the percent of TAO staked to subnets at only 21% vs the 85% of staking rewards going to them, per data from Taostats. It appears users overall seem more comfortable to stake to root despite the lower yield.

Another way this can be interpreted is that most participants are likely not confident enough in the subnets yet to stake directly to them and take on additional price risk. These holders may still believe in the TAO thesis, and are therefore staking, but could be waiting for subnets to mature to further participate. Moreover, it could represent staking conducted via assets deposited on exchanges, such as Kraken, who is the 2nd largest validator in terms of TAO staked on root, according to data from Taostats as of April 30, 2026. Exchanges may not yet offer the ability to stake to subnets directly.

The phenomenon of the relatively high percentage of TAO staked to root and subnets trailing broader root proportion may be best explained by aggregate subnet prices. These appear to have spiked initially but drew down 60% or more in the months that followed. Some of the leading subnets from Spring 2025 fell as much as 80-90% by year end. The apparent volatility may have discouraged adoption, although that may be reversing in 2026 with aggregate subnet prices rising again.

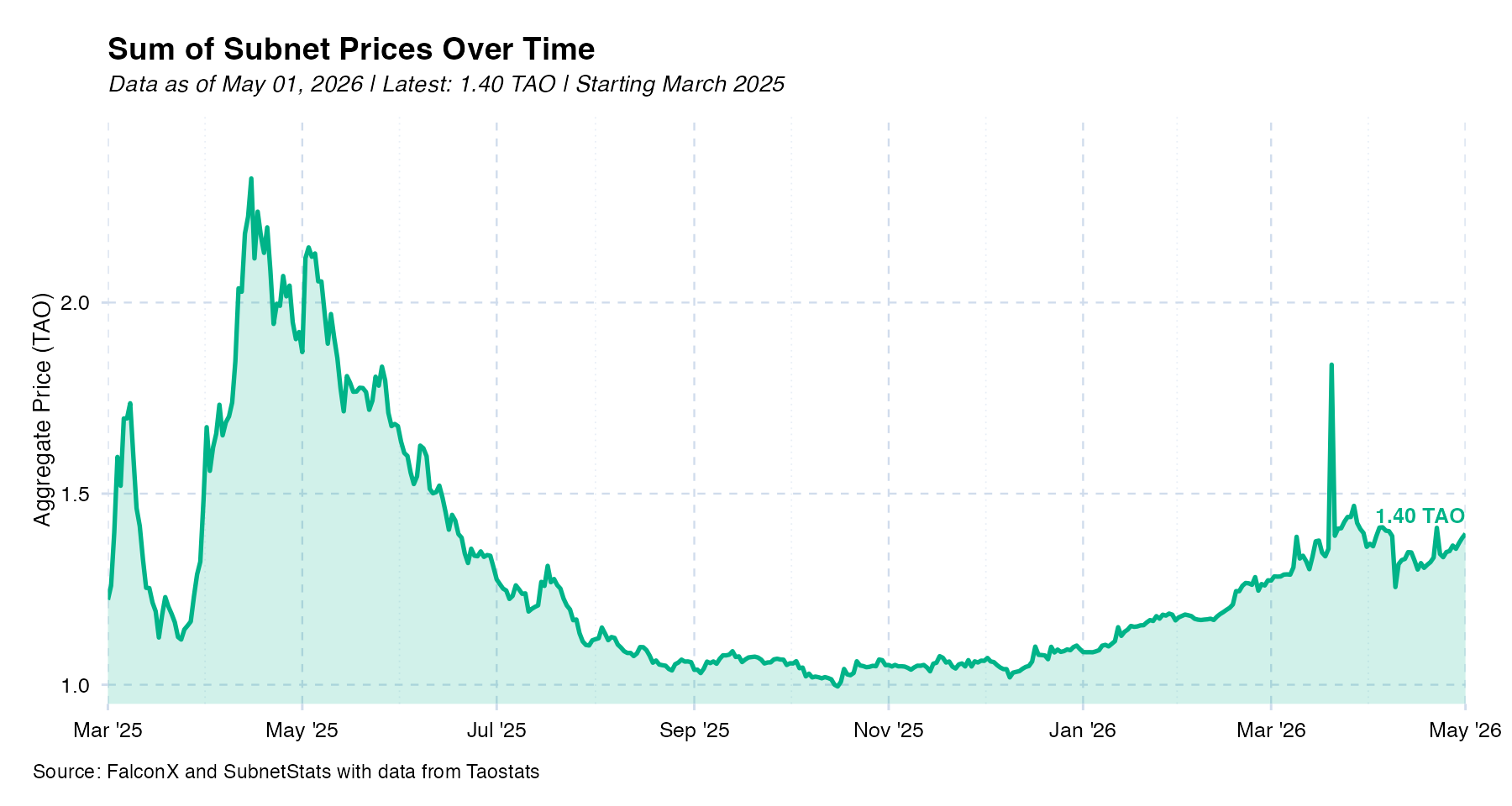

The Theoretical 1.00 TAO Floor of the Sum of Subnets

There is a view that TAO is an index of its subnets and therefore the sum of all subnet prices should total at least 1.00 TAO. The sum of subnets is 1.40 as of May 1, 2026, per Taostats, suggesting the market may be placing a 40% premium on subnets relative to the market price of TAO. Of course, this could simply reflect current staking dynamics where only 21% of TAO holders are active in subnets, according to data from Taostats. Participant behavior may reflect the relatively high yields from subnet staking rather than subnets’ long-term value.

Furthermore, the system tries to enforce a lower limit of around 1.00 sum of subnet tokens, apparently solidifying the concept that TAO is an index of its subnets. If it falls below 1, the system pauses distributions to root stakers, alleviating selling pressure on the subnet tokens until the sum recovers to over 1. Furthermore, chain buys of subnet tokens could intensify as the sum of subnets declines.

How Are Subnet Stakers Positioned Today?

To examine subnet adoption, we analyzed several cohorts of the largest TAO holders to see how they were allocating to subnets.

Largest 10,000 TAO Holders, as of May 1, 2026

We found approximately 52% of the largest 10,000 TAO addresses (holders) staked to subnets, when excluding root (subnet 0). 59% of the cohort was staking to root, with median allocations of 95%. This means most root stakers in the set were almost fully staked and not staking directly to subnets, though individual TAO holders may stake through multiple addresses.

The most common allocations included many of the largest subnets by market cap. Chutes (SN64), Targon (SN4), and Ridges (SN62) were the 3 most held subnets in this regard, seeing 22% and 18% of stakers participating, respectively. Interestingly, median allocations were relatively low: 1-4% for the subnets shown in the figure above. This indicates subnet stakers may be taking a diversified approach and allocating smaller amounts to more subnets, rather than concentrating heavily in a few. It also indicates stakers may be more comfortable allocating more to larger, more liquid subnets that are already generating revenue.

How Have Allocations Changed?

A look at the Top 5,000 TAO holders over time shows those staking to subnets (excluding root) increased their average subnet allocations from around 31% at the start of the year to a high of 40% in early April, 2026, per data from SubnetStats. Allocations declined nearly 10% to 37% on the Covenant developments before recovering to approximately 39% as of early May. Overall, the data suggests that some of the largest TAO holders are becoming increasingly confident in staking a larger portion of their balances to subnets. Note that the increase in TAO staked to subnets may also reflect a rise in subnet prices over the period as well as staking yields from subnet tokens.

Subnet allocations for most top TAO holder cohorts (top 100, 500, 2.5K, 5K) follow a barbell approach, with participants heavily around the 0-5% range (mostly all in root), or 50%+ staked to subnets directly. As seen below, over half of each cohort is allocated to root, with the median allocation of 94%+, indicating many participants are still hesitant to put a more meaningful portion of their TAO portfolios into subnets directly.

Subnet Trading Dynamics

Chain Buys

With the Taoflow mechanism, it is possible for a subnet to see inflows that drive imbalances between a subnet’s token price and its flow-based emission share. For example, when a subnet sees a surge in inflows, its TAO emissions will increase. However, there is a strict limit on the number of subnet tokens that can be injected per block. To solve for this, the protocol scales down the subnet token injection proportionally.

Instead of discarding the excess TAO that would have been injected, it stakes that TAO to the subnet’s liquidity pool, essentially market buying the subnet token. The logic is that the subnets may be undervalued relative to the emissions they are receiving.

As of May 4, 2026, 42 subnets were receiving chain buys of up to 330 TAO/day ($92K), making up nearly 4% of volume on certain subnets. This highlights the potentially meaningful impact of this mechanic on a subnet’s price and positioning around it.

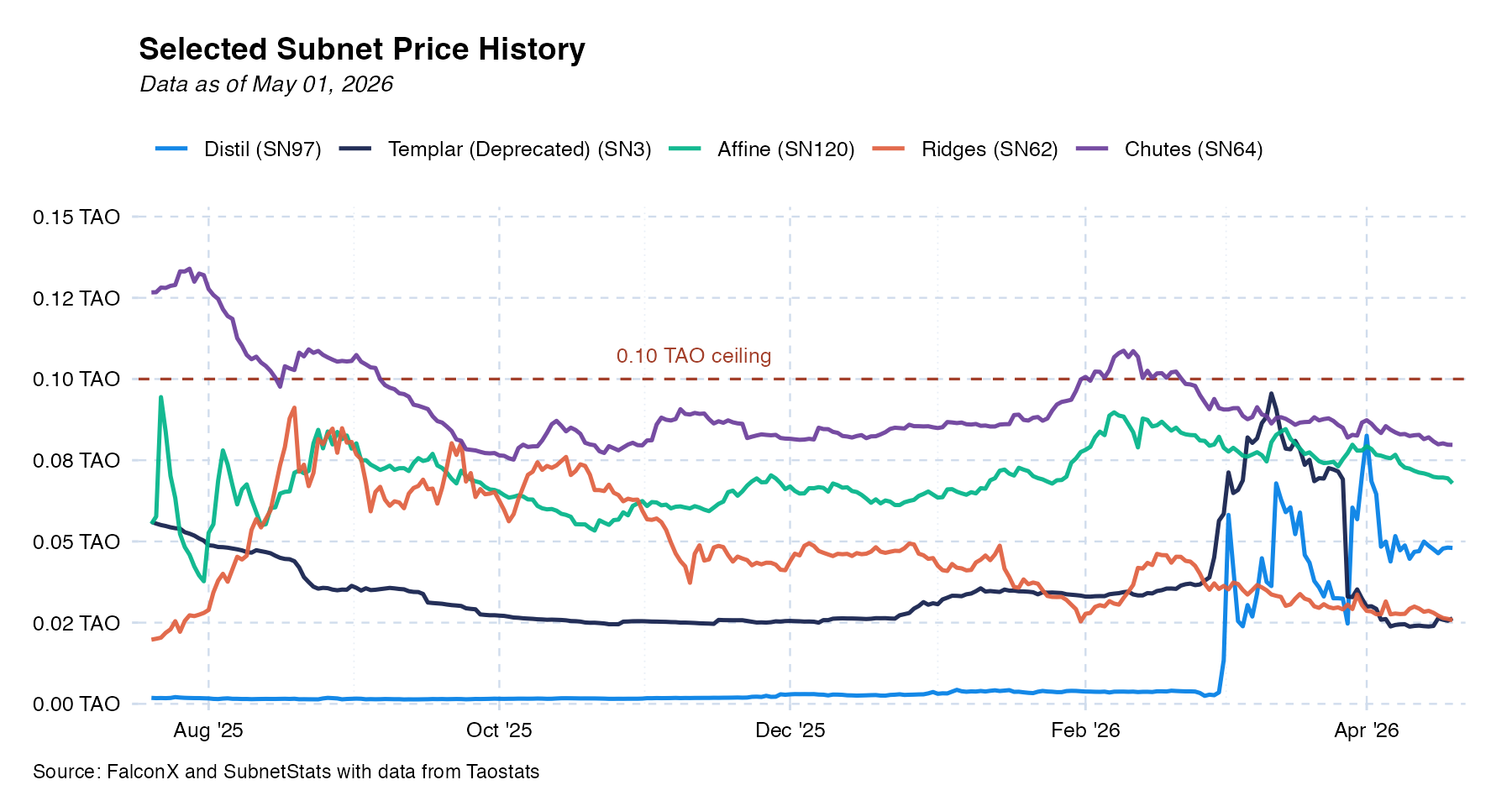

Trading Dynamics: The 0.10 TAO Ceiling

April 2025 saw individual subnets run up to over 0.40 TAO before drawing down over the next 8 months. Since then, trading dynamics have changed and the 0.10 TAO level has appeared as a ceiling for subnets, with no subnets able to hold above that level for long.

This ceiling was observed with Chutes (February 2026), Ridges (September 2025), Affine (February 2025), and Distil (April 2026). Consequently, participants may see this dynamic and prefer to allocate to subnets with lower prices; the largest subnets may be more yield plays rather than upside plays if this ceiling holds. The key question is how much of the overall network could an individual subnet be worth? It likely depends on the addressable market and their state of development. Moreover, the growing number of subnets (128 subnets now vs 64 at the launch of dTAO) may put a lid on subnet prices, especially as the community weighs expanding the subnet cap to 256 in the future.

Whales Drive Flows

Given that many subnet tokens may not be very liquid relative to other cryptocurrencies (only 4 subnets have AMM 2% depth of $1M+ as of writing, per data from CoinGecko), large traders could single-handedly impact the price. On a 7D basis, over 1/3 of subnets see volume largely driven by their top 20 holders, per data from SubnetStats, as of May 1, 2026. Moreover, over the same period, only 9 subnets saw greater than 1,000 traders, reflecting relatively nascent participation.

These dynamics can lead to sharp selloffs, with even the largest subnets seeing 10%+ moves occasionally due to a handful of traders. It also highlights the risk of holder concentration, where many subnets have their top 20-50 holders comprising most of the circulating supply. If one of the top holders exits, it could cause a sharp candle down. Subnet operators can fall into this bucket, another reason for caution.

AMM Liquidity Depth: Another Mechanic to Consider

Given a portion of emissions is added to the subnet token liquidity pool, subnets that can grow emissions typically see greater depth in their pools. While limiting slippage for participants, greater pool depth also means more inflows are required to drive price growth. For example, the largest subnet, Chutes (SN64), stands -78% from its prior ATH (April 2025), yet its AMM has increased 170% in depth ($53M vs $20M). This means far more TAO is required to impact the price and may not necessarily reflect the subnet’s current traction, which may pose challenges for subnet operators and participants. This dynamic could be more pronounced on older subnets that saw heavy emissions under the previous price model, as they now have deeper pools.

The longer-term expectation is for most of the supply to be staked into subnets. For context, root staking stood at 70% at the start of dTAO, per Taostats, and could be a reasonable target (compares to staking ratios of 68% on Solana, per data from StakingRewards).

If this capital comes into subnets, (3x today’s levels), it could have a meaningful impact on subnet token prices. For context, Chutes would require at least $80M of inflows today to return to its ATH, or roughly 2% of circulating TAO supply, per data from SubnetStats, flows that may not necessarily materialize for a given subnet.

Ecosystem Risks: The Covenant Departure

In April 2026, Covenant, an AI lab behind 3 of the top 15 subnets by market cap on Bittensor (Templar, Grail, Basilica) announced it was leaving Bittensor, citing governance issues and that co-founder Jacob Steeves had too much control over the protocol. Covenant sold all its subnet tokens, causing the price of these subnets to decline as much as 40% almost instantly.

This was an impactful event for the protocol, considering Covenant’s flagship subnet Templar had surged to become the 3rd largest subnet by market cap after news picked up of its decentralized 72B parameter LLM training run, thought to be a first in the industry. Moreover, Covenant’s founder Sam Dare was formerly from the Opentensor Foundation (early Bittensor team) and was a prominent Bittensor flagbearer over social media. The episode highlighted the risks to subnet investors in that a subnet’s team can sell its tokens at any moment and wind down the project suddenly.

However, many of the allegations were dispelled by Steeves, while the Covenant post was found to be written entirely in AI, which could cast doubt on the real motivations of the Covenant team.

This incident drove an apparent crisis of confidence in TAO, sending it down 24% within hours after the announcement. One of the key criticisms of the protocol in the past was the risk that successful subnets could simply leave Bittensor and strike it out on their own, with other notable AI projects winding down their subnets previously, such as Nous Research. Covenant leaving was a potential validation of this thesis, and the market had to digest it.

The Potential Risks Exposed

The Covenant departure was a case study on some of the risks in the Bittensor ecosystem.

1. There may not be a strong moat keeping subnets tethered to the Bittensor ecosystem and successful startups may be compelled to leave once at a certain stage. They could seek a cleaner economic structure without the complexity of subnet tokens and emissions. Moreover, they could potentially capture more upside from launching their own Bittensor-like network with their own token.

Steeves alleges Sam Dare/Covenant is trying to raise capital off the back of Templar’s decentralizing training success, suggesting they may be launching their own venture. This would support the route other subnet departures have taken (Nous Research raised at a $1B token valuation). These efforts may suggest Bittensor’s collective intelligence was not core to their business and that they used the network to help test or bootstrap their product.

Challenges here may include not being able to retain the potentially anonymous miners contributing to the subnet (adds friction for them to migrate), and the potentially heavy resource lift in launching one’s own network. Such efforts could also distract from the core business.

2. Bittensor may attract many low-quality subnets or teams looking to extract emissions. The top 10 subnets comprise 32% of the entire network’s sum of subnet prices as of May 12, 2026, per data from Taostats, highlighting investors apparently place the most value on a small number of subnets, following a Pareto distribution. One potential view is that 128 subnets may simply be too many projects for investors to properly assess and raises the possibility of dead weight in the network, although the subnet deregistration mechanism could help solve for this. On the other hand, it could also be argued that if the market is able to assess thousands of public companies in the stock market, it can also efficiently evaluate subnets.

3. The network may be overpaying in emissions. There is criticism that Bittensor is heavily subsidizing subnets relative to what they have produced so far. Moreover, that the subnet products would not be competitive enough to operate without the subsidies. Ultimately, this argument is subjective and can be applied to VC-backed AI labs as well. On the flip side, Bittensor proponents see the high emissions as the key to attracting the best miners/operators around the globe and as paramount to the protocol’s success.

4. The network may have unsustainable economics due to halvings. The other side of the prior argument is that Bittensor will eventually run out of tokens to be able to attract participants. While a valid argument, this is the same case for Bitcoin. The counter to this may be that the network is still early in development and will produce revenue in some form later, or that the TAO token value will rise to the point that the economics still work. As TAO is an index of its subnets, who will presumably return value to token holders in some form, it’s possible the underlying token could grow in step with the prospects of its subnets. By this logic, a single moonshot subnet that proves successful could ultimately validate the valuation of the network. In the long run, TAO subnets may also be able to leverage outside revenue to compensate participants if TAO emissions decline or stop.

5. There may be a gap around the role of subnet tokens. If a subnet has not explicitly committed to driving value to their token or has raised external capital, the token’s success may be separate from that of the project’s. This is akin to the DAO vs Labs situation occurring with many DeFi names.

The Community’s Response to the Covenant Shock

While Covenant’s abrupt departure was surprising, the builders, investors, and contributors behind Bittensor came together rapidly to denounce the Covenant departure and dispel the concerns raised. Many of the largest subnets issued statements suggesting that remaining on Bittensor was core to their project’s success.

A common sentiment was that the Bittensor thesis remains largely unchanged. 3 subnets out of 128 have departed and will likely be replaced with new, motivated subnets or be revived otherwise. Given Covenant’s work was open source, others can pick up the project and further push decentralized model training along. Already, efforts in the old Templar subnet (3) have started for training a 1B parameter model, while other subnets such as IOTA (SN9) continue their work on decentralized training.

In the aftermath, Bittensor co-founder Steeves is pushing forth potential solutions to alleviate the risk of a team selling their subnet tokens suddenly on holders, such as ‘Locked Stake’, where subnet operators would need to lock up their tokens to continue to maintain ownership of the subnet. This could provide subnet token holders some predictability against events like Covenant in the future.

Ultimately, it seems that the community may be doubling down after these events, and the remaining subnets remain focused on improving their offerings and going to market. However, the incident could remain an overhang on the network for some time; it may ultimately take another breakthrough delivered by a subnet for market participants to regain confidence in Bittensor.

Looking Ahead: Building Back Stronger

Bittensor participants are currently evaluating the locked stake proposal that could help deliver some safeguards for subnet token investors by requiring subnet operators to lock up their subnet tokens for periods of time to maintain ownership of the subnet. Therefore, they would not necessarily be able to immediately sell those tokens into the subnet pool, preventing the same situation as with Covenant. Moreover, the mechanics could allow for ownership transfer of subnets based on their locked conviction score, helping abandoned or inactive subnets transition to new operators. However, this proposal is not an end-all. Subnet projects could monetize lock stake through OTC deals or other avenues, which may not solve the problem at hand.

Other key items on the roadmap, presented by Steeves in February 2026, include governance changes. This includes a transition to nominated proof of stake and an on-chain governance model. The stated goal is to have fully decentralized governance by the end of 2026. Part of this involves updating the triumvirate, a group of three key ecosystem participants with ties to the Opentensor Foundation that can make proposals and implement upgrades, to a rotating set of top subnet operators and validators, which are backed by TAO/subnet token holders.

In addition, there are calls for governance actions to be taken in the coming months to eliminate emissions for exploitative or non-productive subnets. An idea was also floated to cap the number of subnets receiving emissions, such as to the top 64 subnets only.

Relative Metrics (Illustrative)

TAO is the largest AI token by market cap, with other larger players including NEAR and ICP. Notably, TAO is generating $17M annualized revenue, per data from Artemis, which consists of subnet registration fees and transaction fees. This gives it a lower MC/Revenue multiple than some of its AI peers, and comes in lower versus L1s ETH and SOL, which may be relevant comparisons in terms of network effects.

Conclusion

Bittensor remains a big idea (permissionless, decentralized marketplace for intelligence) that is attracting AI builders around the world, but it must work through the overhang caused by Covenant. Its subnets are starting to deliver breakthroughs, demonstrating early traction, but it remains to be seen if the subnet token model will be viable as the subnets scale.

As the largest AI-focused token by market cap, TAO remains a story to be followed. Participants may look toward further traction in subnets, improved governance, and emissions changes to reward only productive subnets as a sign that the Bittensor thesis remains on track.

This report is provided strictly for informational purposes and does not constitute investment advice. This report is co-authored by FalconX and SubnetStats (Pine Ridge Analytics LLC), with SubnetStats contributing subnet staking data and analysis. Please note that Martin Gaspar, Senior Crypto Market Strategist at FalconX and founder and owner of SubnetStats, will benefit if this publication results in increased interest in the discussed ecosystem.

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd., nor Banzai Pipeline Limited service retail counterparties, and the information on this website is NOT intended for retail investors. The material published on this website is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this website is not and should not be regarded as investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

No discussion of a particular company or product shall be considered an endorsement of such company or product. Past performance is not indicative of future results. FalconX, and its affiliated parties may hold positions in, act as a market maker for, or otherwise have a financial interest in, assets discussed herein, and may benefit from any price movements or transactions involving the subject company. This may change without notice. Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory, and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over-the-counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a swap dealer with the U.S. Commodities Futures Trading Commission (CFTC) and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is a registered Class 3 VFA service provider with the Malta Financial Services Authority under the Virtual Financial Assets Act of 2018. FalconX Limited is licensed to provide the following services to Experienced Investors, Execution of orders on behalf of other persons, Custodian or Nominee Services, and Dealing on own account. FalconX’s complaint policy can be accessed by sending a request to complaints@falconx.io

"FalconX" is a marketing name for FalconX Limited and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.

.jpg)