Optimism: The Enterprise Blockchain Stack

Optimism (OP) is evolving into a key engine behind enterprise blockchains, with 50+ chains leveraging its tech stack (“OP Stack”), processing over 6 billion transactions in 2025.

By reducing go-to-market friction through its fully open-source distribution model under the MIT license and allowing anyone to participate and fork its code, Optimism has been able to secure major users of its tech stack. So far, key users of the OP Stack include Kraken (Ink), Sony (Soneium), World (World Chain), Uniswap (Unichain), Bitpanda (Vision Chain), and most recently Upbit (GIWA Chain). The low barriers to participation bring a diverse set of use cases: Exchanges, DeFi, Entertainment, and a Social Network (World has ~18M unique humans, 39M World App users). With the adoption in place, Optimism has moved to offer managed infrastructure services via OP Enterprise, similar to how Red Hat (IBM) monetizes Linux.

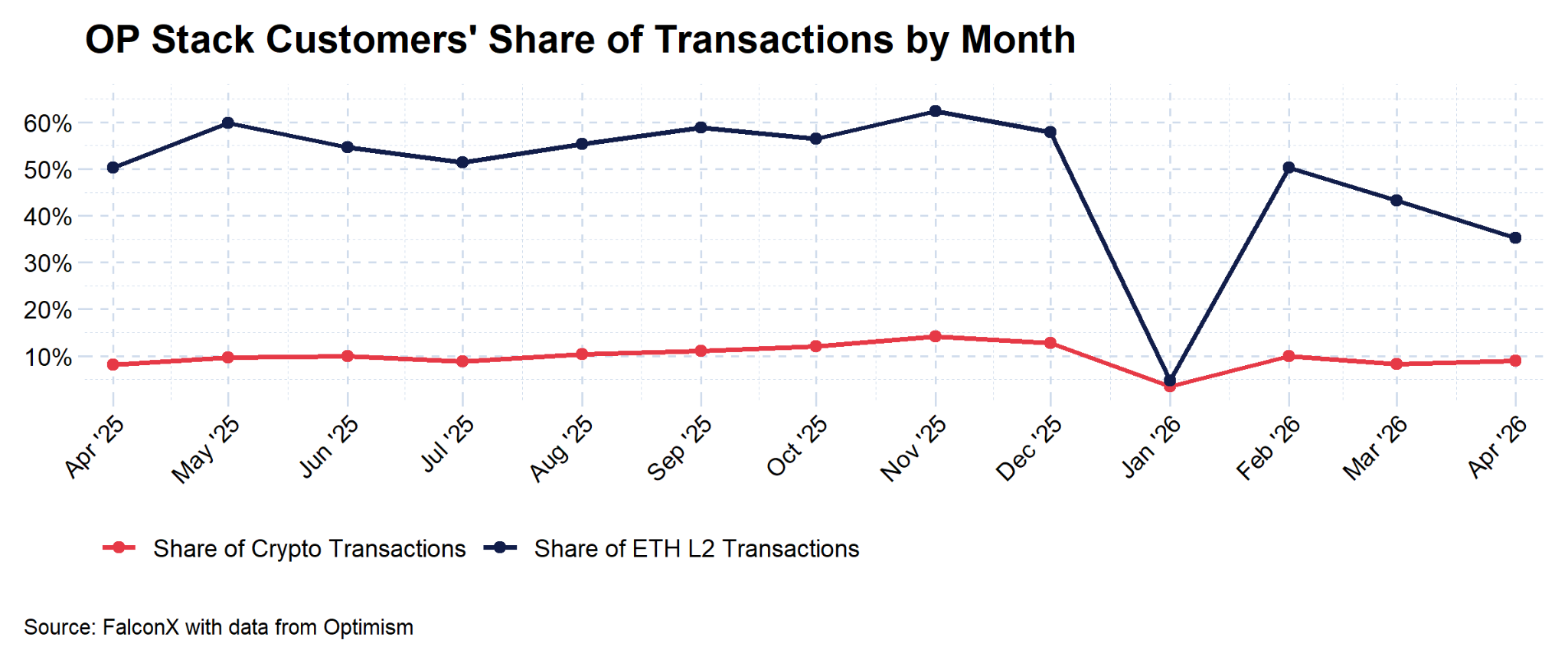

As of April 2026, OP Stack customer chains generated 35% of ETH L2 transactions and 9% of total crypto transactions, per data from Optimism, highlighting its tech stack’s substantial footprint. Note that the drop in share of crypto transactions in January 2026 was attributed to MegaETH’s load testing ahead of its mainnet launch.

The Legacy Superchain Economic Alignment Model

In Optimism’s original economic model (“Superchain”), L2s built on the OP Stack voluntarily agreed to contribute a portion of their economic activity to the Optimism Collective, calculated as the greater of either 2.5% of total chain revenue or 15% of on-chain profits (fee revenue minus L1 gas fees). In return, L2s participating in the OP Stack benefited from coordinated network upgrades. Ultimately, this was a bet that the network effects and benefits of being in the OP Stack would attract and/or keep partners content enough to pay into the OP Stack.

The New Economic Model: OP Enterprise

As Optimism’s customer base shifted from crypto-native teams to regulated companies, its commercial model evolved to match how these firms traditionally pay for tech infrastructure. Optimism’s managed blockchain infrastructure offering ‘OP Enterprise’ was launched in January 2026. It follows a SaaS pricing model, offering companies predictable costs, SLAs, and dedicated support. Enterprises pay for the service and keep all the value their chain generates. It is geared for teams who want their own L2 blockchain without dealing with the tech and maintenance lift on their own. Launch customers for OP Enterprise included Unichain and Celo, while Bitpanda’s Vision Chain has since been announced as the first fully managed OP Enterprise deployment.

OP Enterprise has three tiers of offerings. According to its announcement, most clients get to production in 8-12 weeks from initial conversations, with testnet in 4-8 weeks, highlighting the relatively short timelines for companies to go to market.

Fully managed: Optimism completely handles the chain.

Self managed: Client operates it, Optimism supports it.

OP Mainnet: Client starts on the Optimism L2 and graduates to their own chain when ready.

Part of the pitch to businesses is that Optimism has already onboarded leading vendors and partners to the Optimism ecosystem. They can thus be ready to quickly deploy to an Optimism-supported chain, accelerating go-to-market. Optimism has launched over 50 chains for enterprise customers demonstrating its capabilities and track record in this regard.

Optimism also offers a ‘Mission-Critical Support’ option for priority incident and security responses, bespoke integrations, and elevated SLAs. This is what Base is using.

On the tech side, the OP Stack allows businesses to launch with sub-200ms block times. Importantly, no vendor lock-in remains key to the offering given the MIT license, with OP keeping the core stack open but monetizing through these enterprise services, similar to a SaaS model. One advantage to working with Optimism through this service is that they see issues before they’re public and can push patches and updates to customers quickly.

Another key feature of OP Enterprise includes managed compliance tooling. This involves configurable rules for transaction ordering and filtering at the sequencer level (such as compliance lists, allowlists, and blocklists). This gives enterprises control over transactions included in a block, which can be critical for regulated industries, permissioned deployments, and compliance requirements. There can also be optional screening on OP Stack bridge contracts that evaluates L1/L2 transactions against configurable rules prior to execution, which can allow chain operators to implement another layer of screening (OFAC/sanctions list, for example) at the bridge contract level.

Pricing for OP Enterprise is not published so it is unclear how much incremental revenue it could generate for Optimism. Payments will accrue to the Optimism Foundation and are currently out of scope for buybacks, which only uses OP Stack/Superchain-related revenue, though this could change in the future.

The Buyback Mechanism

In January 2026, the Optimism DAO voted to implement monthly OP token buybacks using 50% of net Superchain sequencer revenue over a 1-year pilot period, with buybacks commencing in February 2026. In 2025, Optimism collected nearly 5.2K ETH in revenue from chains using the OP Stack (~$12M at current ETH prices), all of which went to the Optimism treasury overseen by Optimism governance, although it is worth noting this traction was largely driven by Base. The move to implement buybacks is a way to help align the OP token with growth of the OP Stack.

Part of the buyback proposal allows for the Optimism Foundation to manage any ETH revenue not directed to buybacks, supporting further treasury management practices. Like its peer Arbitrum, Optimism could use treasury management activities to provide additional resources to support long-term ecosystem sustainability.

The buybacks will be conducted via an OTC partner. OP tokens purchased will go to the treasury, and could be burned or deployed for growth or rewards in the future. As OP Enterprise scales, future governance proposals could expand buyback funding sources to include Enterprise revenue.

Base’s Transition from the OP Stack

In February 2026, Coinbase announced its Base L2 was moving away from the OP Stack, with a key goal to have more control over its tech stack. While this could negatively impact Optimism’s top line, this kind of vertical integration is perhaps inevitable. It validates how Optimism can support the rapid growth of enterprise blockchains until maturity. Moreover, it demonstrates that the relationship does not end once an L2 hits critical scale – Optimism is retained as a key service provider. This may offer a reference case for enterprise blockchain development.

Base’s shift is perhaps the natural progression of building on the OP Stack, which is meant to enable growth of a business to the point where it may seek more independence and control for features. Base is a great example of this, as it was able to quickly go to market thanks to the OP Stack. This enabled Base to focus on growing adoption, instead of spending significant resources building out its tech. Now, it seems to be looking to advance development on its own, such as transitioning from optimistic proofs to TEE/ZK proofs for faster finality. The move would enable it to experiment with different tech features, ship upgrades on its own cadence, and reduce code complexity. Base explained the transition was in part for a faster shipping cadence and simplifying its codebase, noting the coordination and maintenance overhead from multiple teams and repositories as a pain point. It also said the move will enable it to move faster on its decentralization efforts.

Ether.fi Migration: A Case Study in the OP Stack’s Pull

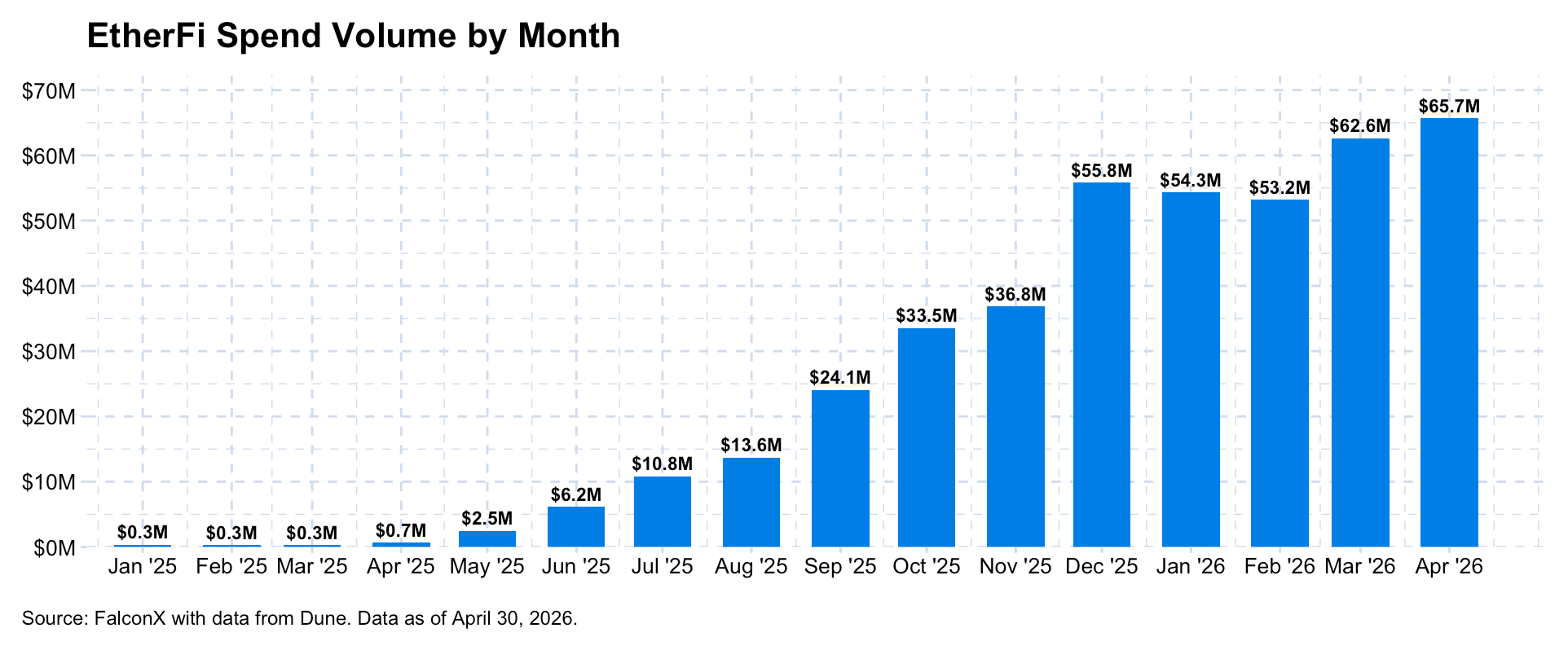

While Base is departing the OP Stack, another major crypto player has opted to transition to the OP Stack. In February 2026, crypto neobank ether.fi announced plans to migrate its digital cash account and card product from the Scroll L2 to OP Mainnet as an OP Enterprise customer. This migration will bring ~70K active cards, ~300K accounts, and an average of $2M of daily spend volume to Optimism.

The announcement states the migration will unlock increased liquidity for swaps within a larger DeFi ecosystem. Moreover, it cites a stronger infrastructure designed to support high transaction volume. Importantly, gas fees and network costs for card transactions will be covered by ether.fi, made viable by the low gas fees on the network. With ether.fi’s card spending volume ramping up in recent months, the activity could prove a meaningful driver for Optimism.

The ether.fi migration to OP Mainnet occurred mid-April, bringing $220M in TVL, 70,000 active cards, and 300,000 accounts to OP mainnet. This effectively doubled TVL on OP Mainnet, adding substantial new activity. Upcoming ether.fi offerings on OP Mainnet include rolling out its Gold Vaults and launching its Euro card.

Ether.fi’s decision to shift to Optimism highlights how top projects increasingly select their L2 homes based on strategic alignment and infrastructure quality. The move is especially notable considering the neobank narrative is heating up and ether.fi is seeing increasing activity in its card product (ether.fi Cash).

Bitpanda’s Vision Chain

Optimism added another major enterprise partner to its tech stack with Bitpanda, a European crypto exchange with 7 million users, in March 2026. Bitpanda is launching its ‘Vision Chain’ geared towards European financial institutions, with tokenized assets in mind. Bitpanda is targeting the mainnet launch for later in 2026.

Its Vision Chain is being developed on the OP Stack and will be fully managed through OP Enterprise, enabling Bitpanda and its partners to go to production without building the tech stack from scratch. The fully managed component means Bitpanda does not run sequencers or coordinate security patches; rather, Optimism handles this for them.

Notably, this chain will integrate OP Succinct’s zero-knowledge technology, targeting same-day withdrawals to L1 — providing capital and settlement efficiency for institutions. It will also enable Euro stablecoin gas payments.

This is a great example of how Optimism’s tech stack enables corporate partners to go to market by abstracting away the tech complexity, enabling Bitpanda to focus on delivering products for its users. The announcement specifically highlights the customizability of the OP Stack (custom gas payments) as well as its tech benefits (same-day L1 withdrawals) that Bitpanda found useful.

European institutional finance is a large market and the Vision Chain could provide the playbook for more institutional participation via the OP Stack. Per the Optimism team, key to this is the MiCA and DORA compliance architecture built into the infrastructure, rather than at the application layer, which is a differentiator vs other L2s.

Recent Developments

In addition to the ether.fi and Bitpanda Vision Chain news, Optimism has had several announcements in April:

Stake-Based Priority Ordering

Optimism announced an experiment with regards to MEV and tokenomics: stake-based priority ordering. Participants who stake OP into an audited smart contract receive top-of-block positioning for their transactions. The experiment is live on testnet and will roll out to OP Mainnet in phases, starting with a flat FIFO tier and progressing to a stake-weighted multiplier model.

Currently, its transaction inclusion policy on OP mainnet has every transaction competing for block inclusion via a priority gas auction. This can lead to redundant transactions from bots, potentially disrupting blockspace access for other users.

The initial phase of the rollout will enable addresses staking at least 100,000 OP ($13K as of writing) to be eligible for top of block positioning on a FIFO basis. Non-staking transactions will continue to be ordered by the existing priority gas auction.

The next phase introduces a multiplier that blends stake size, stake duration, and priority gas into a single ordering score, incentivizing larger and longer OP staking. Ultimately, this move could help drive more utility to the OP token, and could make it partially reflect the value of MEV on the chain.

The initial staking parameters feature no lockups and eligible transactions are limited to up to 20% of the gas limit consumed per flashblock.

Mitsui Launches Japan's First Commodity-Backed Cryptoasset on OP Mainnet

Mitsui & Co. Digital Commodities, a wholly owned subsidiary of Mitsui & Co., Ltd. (a Fortune Global 500 company with a market capitalization exceeding $94 billion), announced it is launching Zipangcoin (ZPG) on OP mainnet. This is a cryptoasset backed by gold, silver, and platinum, and helps support the thesis of the OP Stack serving the needs of financial institutions.

Privacy Boost

Optimism announced its first privacy offering via Sunnyside Labs’ Privacy Boost, described as an on-chain privacy SDK for enterprise. By leveraging both TEE and ZK proofs, this offering enables encrypted token transfers, private smart contract logic, and compliance-compatible architecture, such as auditability. This can enable private swaps, earn, and lending.

So far, Privacy Boost is coming to Soneium and integrating into the Startale App, which serves as a flagship entry point to Soneium. This integration allows for high-performance privacy at large scale (sub-500ms proof generation and 1,800+ TPS). The release states this can help support offerings such as crypto cards, where users can spend without exposing their full on-chain activity.

This is a significant development for Optimism as privacy stands to be a key factor in bringing enterprises and institutions on-chain. This potential customer base has strict compliance requirements and may not be able to fully build out offerings if a chain’s activities are completely public, therefore such privacy features can be essential for them.

Re7 Capital Launches ETH Strategy on Optimism

Digital asset investment firm Re7 Capital launched its market-neutral ETH Yield Strategy on Optimism, helping position Optimism as a key chain for institutional DeFi. This is a tokenized strategy via Midas. The Optimism Foundation has engaged Re7's ETH Yield Strategy as a primary source of yield across its ecosystem. The arrangement gives the ETH Yield Strategy access to native incentive structures tied to real ecosystem growth on Optimism, distributed through genesis liquidity provision.

Dunamu (Upbit) Building on the OP Stack

In early May, Dunamu, the parent company of Korean crypto exchange Upbit, and The Optimism Foundation announced a non-binding Memorandum of Understanding (MoU) on GIWA Chain, a new Ethereum L2 built on the OP Stack. Under the MoU, GIWA Chain plans to be the first chain to operate on the self-managed tier of OP Enterprise. GIWA chain is currently live on testnet.

The announcement adds another major crypto exchange as a user of OP Enterprise. Upbit serves more than 13M registered users and ranked #2 globally by cumulative spot trading volume from 2020 to 2024, per CoinGecko.

It is notable that Dunamu will be using the self-managed tier of OP Enterprise. Versus the fully managed tier where Optimism handles the chain, in the self-managed offering, the operator runs the chain's primary sequencer, controls configuration, and holds operational authority. The Foundation provides assurance, monitoring, engineering support, and a backup sequencer in the event of primary sequencer disruption.

Assessing the Arbitrum vs Optimism Models

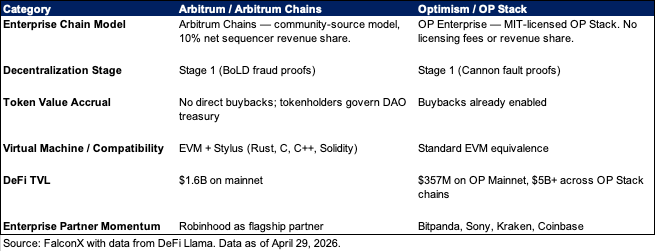

On the surface, Arbitrum and Optimism are both leading L2s with impressive tech stacks. Each is balancing an approach to support activity on their own L2, but also position themselves in the emerging blockchain-as-a-service vertical.

While Arbitrum currently leads Optimism in terms of DeFi and RWA activity on its chain, Optimism has demonstrated the ability to secure rapidly growing protocols like ether.fi for its main L2. Arbitrum may be better suited to benefit in the short term from current activity on its chain, but if Ethereum L1 scaling slows the migration of activity to L2s, Optimism could ultimately benefit from independent sources of activity (neobanks).

A key difference between the two is their approach to enterprise L2 solutions. Arbitrum leverages a community source model at a fixed 10% net sequencer revenue share, ensuring some monetization, while Optimism sees the network effects of the MIT-licensed OP Stack driving partners to engage with OP Enterprise. Per the Optimism team, OP Enterprise also brings built-in key compliance features, such as OFAC/sanctions screening at the sequencer level, guardian role for incident response, permissioned fault proofs, and Stage 1 decentralization. Moreover, its fully managed service handles sequencers, upgrades, and monitoring, reducing potential technical lift for enterprise clients.

Regarding value accrual, Optimism already has buybacks enabled, making it more than a governance token. Arbitrum has yet to have such direct value accrual, but tokenholders strictly govern the DAO that manages the project’s treasury.

In terms of Vitalik Buterin’s updated L2 framework, both of these leaders are differentiating through their tech stack, offerings, and partnerships. The future of Arbitrum relies on the success of its Arbitrum Chains model and the adoption of the Robinhood Chain will likely be key to this. Optimism must see continued enterprise adoption of the OP Stack, and the addition of new partners such as Bitpanda signal momentum on this front. Market participants may evaluate which path stands to be the most successful, especially as scaling improvements continue driving down transaction fees, making high turnover business models especially key to any blockchain.

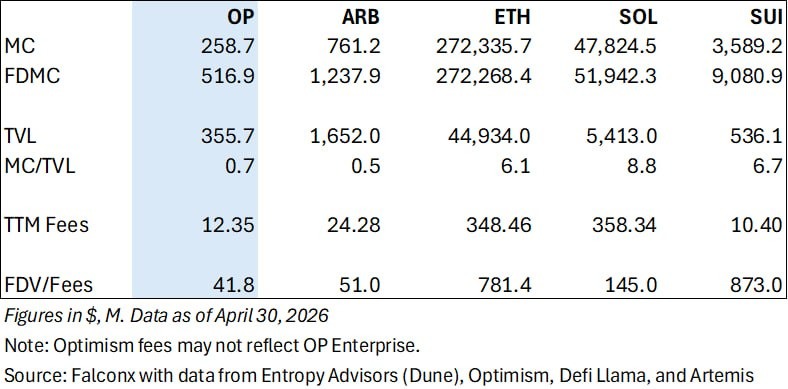

Relative Metrics (Illustrative)

At current levels, OP trades at a lower revenue multiple (FDV/Fees) relative to leading L1s. ETH, for example, trades at roughly 19X OP’s FDV/Fees multiple. Pertaining to its core L2, OP trades amongst the lowest MC/TVL multiple of its peer set, per data from Artemis.

One takeaway may be that compared to L2s, major L1s trade at significantly higher revenue multiples relative to their current activity and revenue generation, despite functionally delivering a similar offering (blockspace). However, the increasing convergence of traditional industries onto blockchain tech often supports separate chains for greater control and customizability, which could favor L2s such as Optimism which offer blockchains as a service.

OP Stack Revenue Traction

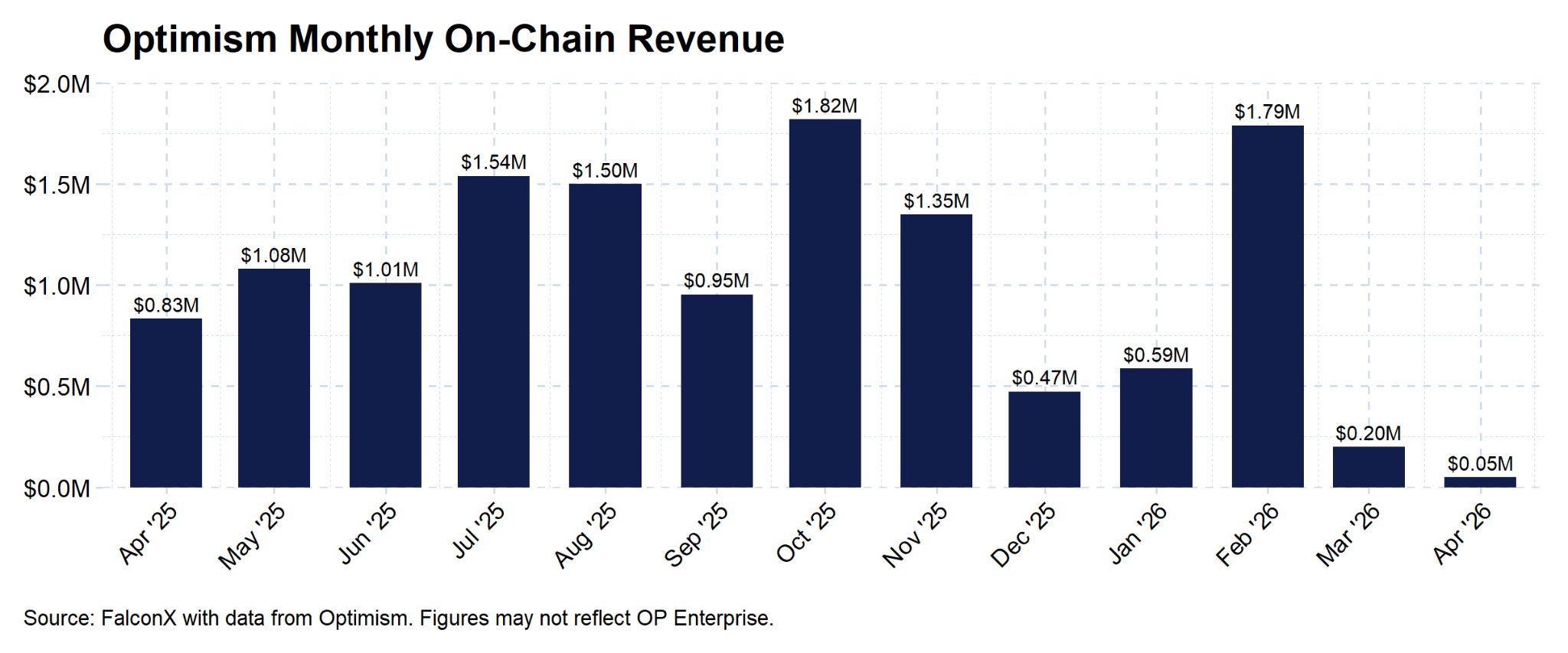

Per Optimism’s dashboard, the OP Stack generated $12.4M of on-chain revenue in the trailing twelve months as of April 2026. Revenue includes 100% of OP on-chain profit and the greater of 2.5% chain revenue or 15% net on-chain profit in ETH for all other chains in the OP Stack.

A key trend that can be seen is that the highest revenue months in the period were those with significant volatility events (October 10, 2025 and February 5, 2026). These may have served as catalysts for greater on-chain activity across the OP Stack.

March and April 2026 were softer months in terms of revenue, likely reflecting weaker market conditions more broadly but also the transition to the OP Enterprise model - the impact of which should become clearer in the coming months.

Conclusion

Optimism stands to be a key infrastructure provider in the enterprise blockchain space. Its full product suite, now coming into vision through the launch of OP Enterprise, sets the stage to support enterprises in each step of their blockchain journey. OP mainnet has proven to be a valuable initial landing field for applications such as ether.fi, while partners like Bitpanda requiring enterprise blockchains have found OP Enterprise to fit their needs. With OP Enterprise, Optimism further opens the door to meet businesses where they are, and maintains a key relationship as their infrastructure provider as these companies scale.

It is still early days in the enterprise blockchain journey. Optimism has lined up several marquee partners utilizing its tech stack in some form, especially on the exchange side (Coinbase, Kraken, and now Bitpanda), and stands to benefit if activity from these chains ramps up.

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd., nor Banzai Pipeline Limited service retail counterparties, and the information on this website is NOT intended for retail investors. The material published on this website is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this website is not and should not be regarded as investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

No discussion of a particular company or product shall be considered an endorsement of such company or product. Past performance is not indicative of future results. FalconX, and its affiliated parties may hold positions in, act as a market maker for, or otherwise have a financial interest in, assets discussed herein, and may benefit from any price movements or transactions involving the subject company. This may change without notice. Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory, and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over-the-counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a swap dealer with the U.S. Commodities Futures Trading Commission (CFTC) and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is a registered Class 3 VFA service provider with the Malta Financial Services Authority under the Virtual Financial Assets Act of 2018. FalconX Limited is licensed to provide the following services to Experienced Investors, Execution of orders on behalf of other persons, Custodian or Nominee Services, and Dealing on own account. FalconX’s complaint policy can be accessed by sending a request to complaints@falconx.io

"FalconX" is a marketing name for FalconX Limited and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.