How Reflexivity Can Inform Options Strategies for DATs

Since late 2025, many digital asset treasury companies (DATs) have seen their mNAV premiums compress or turn to discounts amid broader market weakness. The current environment may raise the need for tools they can use to close their mNAV discount gap or to supplement proceeds from the capital markets.

Options strategies, such as writing covered calls, can be versatile tools intended to help DATs generate income for share repurchases, helping reduce an mNAV discount, or to purchase crypto if trading at an mNAV premium. This is the Metaplanet model, which has a ‘Bitcoin Income Generation Business’ that involves the use of Bitcoin options to generate recurring operating revenue. There are no guarantees, but in 1Q26, these strategies generated nearly $18.7M in revenue for Metaplanet.

A key consideration on which strategy can make the most sense for a DAT lies in its reflexivity to its underlying crypto holdings. Per our definitions, a name has positive mNAV reflexivity if mNAV expands as the coin rallies (usually because the share price outperforms the underlying coin) and negative mNAV reflexivity if mNAV compresses on rallies in the underlying coin (the earlier-stage mNAV premium fades or the equity does not keep pace with the growth in crypto holdings). In this piece, we examine the DAT landscape in this context and point to the options strategies that could benefit them.

DAT Cohort and Methodology

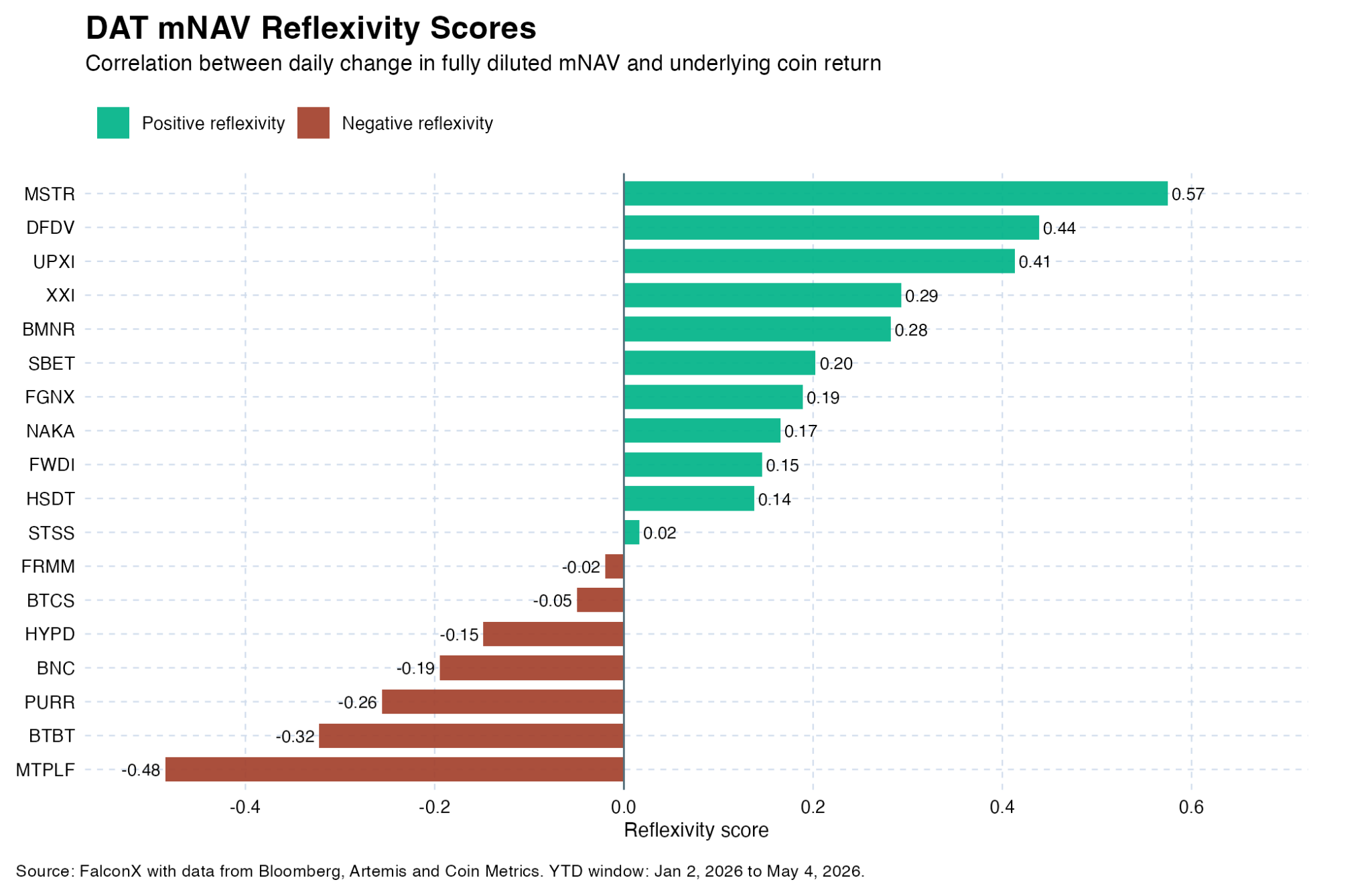

We analyzed the following set of 18 DATs, with fully diluted mNAV data sourced from Artemis.

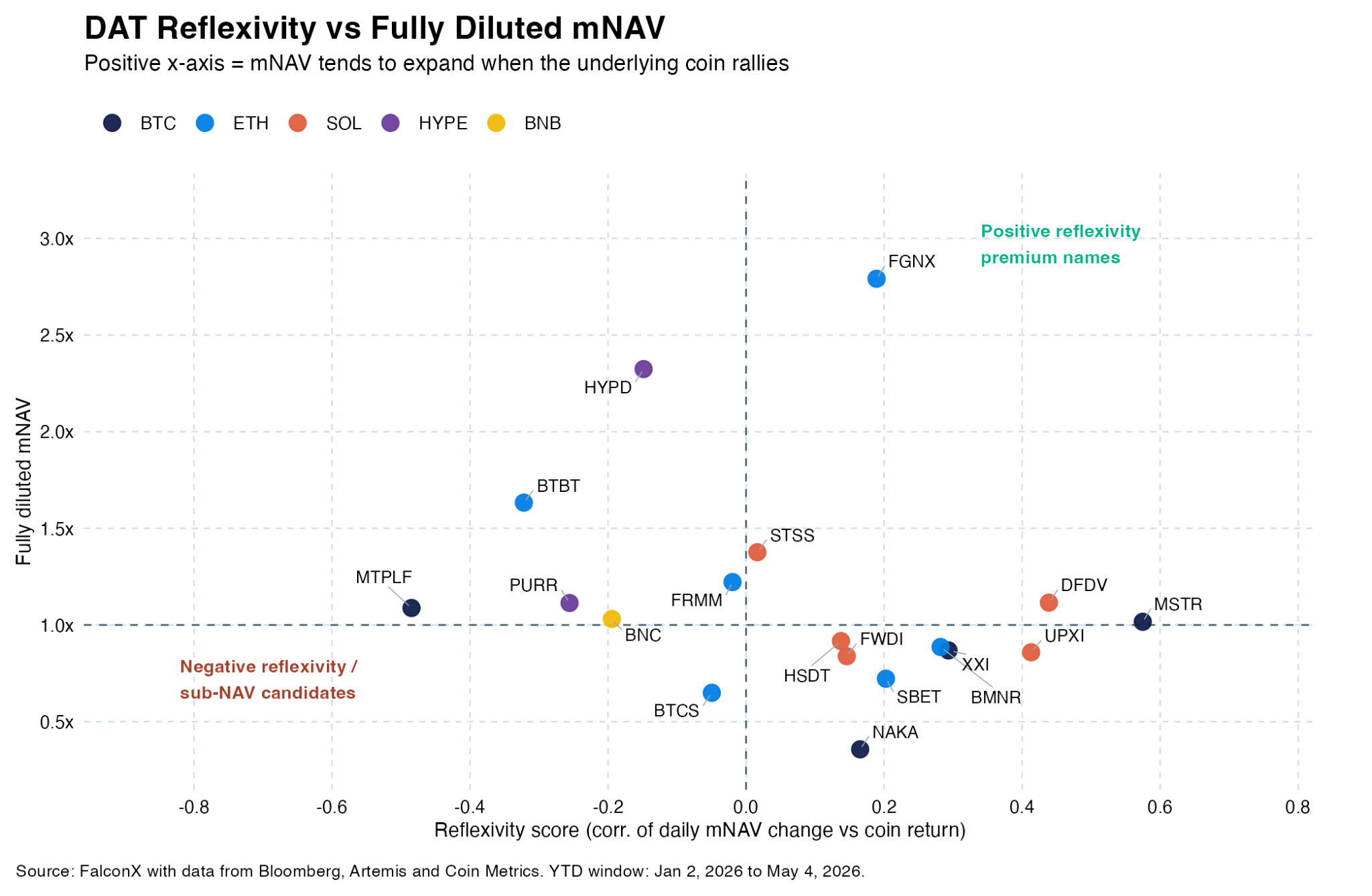

Using YTD data (January 2 to May 4, 2026), we calculated metrics such as correlations, beta, and up/down capture ratios of the DATs’ share price with their respective treasury token (BTC, ETH, SOL, HYPE, BNB). Our goal was to assess each DAT’s mNAV reflexivity score – whether a DAT’s premium to NAV expands or contracts when its underlying treasury token increases in price. Reflexivity was calculated as the correlation between the daily change in fully diluted mNAV and the daily return of the underlying coin.

This kind of reflexivity is an important consideration for options strategies, as it may directly impact the opportunity cost of selling calls. See the Evaluating Options Strategies section for a detailed discussion of how reflexivity may be considered when evaluating strategy selection.

Results

The results show mixed performance across the cohort. DATs that traded at a discount or close to 1.0x mNAV showed positive reflexivity, whereas DATs that traded at a significant premium to mNAV exhibited negative reflexivity. This is despite the majority of names exhibiting positive correlations with the returns of their stock and those of the underlying treasury token.

8 of 10 DATs that began the period trading under 1.0x mNAV exhibited positive reflexivity.

Across BTC DATs, MSTR and XXI saw notable positive reflexivity, while MTPLF exhibited negative reflexivity, respectively.

ETH DATs saw more dispersed results. Of the ETH DAT cohort, BMNR and SBET exhibited the strongest reflexivity (0.28 and 0.2, respectively), while several saw negative reflexivity.

Amongst SOL DATs, DFDV and UPXI saw the most positive reflexivity (0.44 and 0.41, respectively). Notably, 4 out of 5 DATs in the cohorts saw their share price performance outperform that of SOL over the period.

HYPE DATs HYPD and PURR exhibited negative reflexivity, likely in part due to their steeper mNAV premiums at the beginning of 2026.

Evaluating Options Strategies

mNAV reflexivity can help inform derivatives trading strategies for DATs. For DATs who want to generate income on their underlying, covered call strategies can potentially take advantage of positive mNAV reflexivity. For the positive reflexivity cohort, when the underlying rallies the share price is expected to outperform the underlying (due to the reflexivity), which may overcome the opportunity cost of being short calls in a rallying market. Consequently, this metric can be useful in informing DATs on the aggressiveness of strike selection.

While there are always risks inherent to options strategies, potential structures include:

Covered Calls: Write OTM calls against coins in treasury. This can be a viable strategy for DATs regardless of reflexivity; positive reflexivity DATs can see their mNAV improve even if called away.

Puts: Sell OTM puts to be able to acquire more coins at a discount and earn a premium in the meantime. This could potentially be relevant for cash-heavy DATs such as PURR (had $104M of cash as of May 4, 2026) and BMNR ($685M cash as of May 17, 2026). Such a strategy could make sense for DATs whose share price outperforms the underlying token on the way down (observed in the downside capture ratio for DATs including HSDT, and STSS) as they may have more flexibility to manage selloffs.

Collars: Cap upside with a written call and finance a long protective put. Potentially useful for sub-1x mNAV names that may want to defend book value (NAKA, FWDI) without forcing a coin sale.

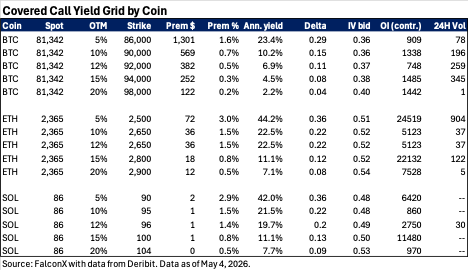

Designing the Coin-Underlying Covered Call Program: Strikes, Yields, and Sizing

We pulled the Deribit option chain (snapshot from May 4, 2026, for the May 29, 2026, expiry) for BTC, ETH, and SOL to determine what a front-month, OTM covered call program could look like for each coin. We selected representative strikes at 5-20% out of the money.

The front-month 10% OTM annualizes to roughly 10% on BTC, 22% on ETH, and 22% on SOL. 15% OTM annualizes to 4% on BTC, 11% on ETH, and 11% on SOL. The difference in yield is due to the IVs of the underlying: BTC 30D OTM IV is in the mid-30s, while ETH and SOL IV is around 50. This is why ETH and SOL DATs can generate more yield from selling 10% to 15% OTM calls relative to BTC DATs, although there is relatively more risk that an option will land in-the-money (ITM) given the higher IVs suggesting market expectations for larger price moves .

Liquidity Considerations

Options liquidity on exchanges can be thinner than the DAT cohort’s collective treasury. For example, Deribit BTC open interest stood at around $30B, as of May 4, 2026, which compares to MSTR’s BTC holdings of over $66B as of the same date. Deribit’s ETH open interest was around $5B, which compares to BMNR’s holdings of $10B, per its SEC filings.

For larger sizes or non-BTC options (such as ETH, SOL, BNB, and HYPE) with less on-exchange liquidity, DATs can trade with OTC desks such as FalconX that support much larger sizes than orderbook liquidity. FalconX operates one of the world’s largest institutional crypto options desks supporting 80+ tokens across select jurisdictions. As a top dealer on platforms like Deribit and Paradigm, FalconX brings a proven track record of execution, liquidity, and reliability.

Depending on the size of its coin holdings, DATs may look to only allocate a smaller portion (5%-10%) of their total treasury to options strategies. This can help limit market impact.

DATs may consider front-month or front-week expiries. Options decay increases exponentially as the options get closer to expiry, so weekly rolls of 10-14 days to expiry (DTE) could be preferable over monthly rolls at the cost of more operational overhead and the potential for greater transaction costs.

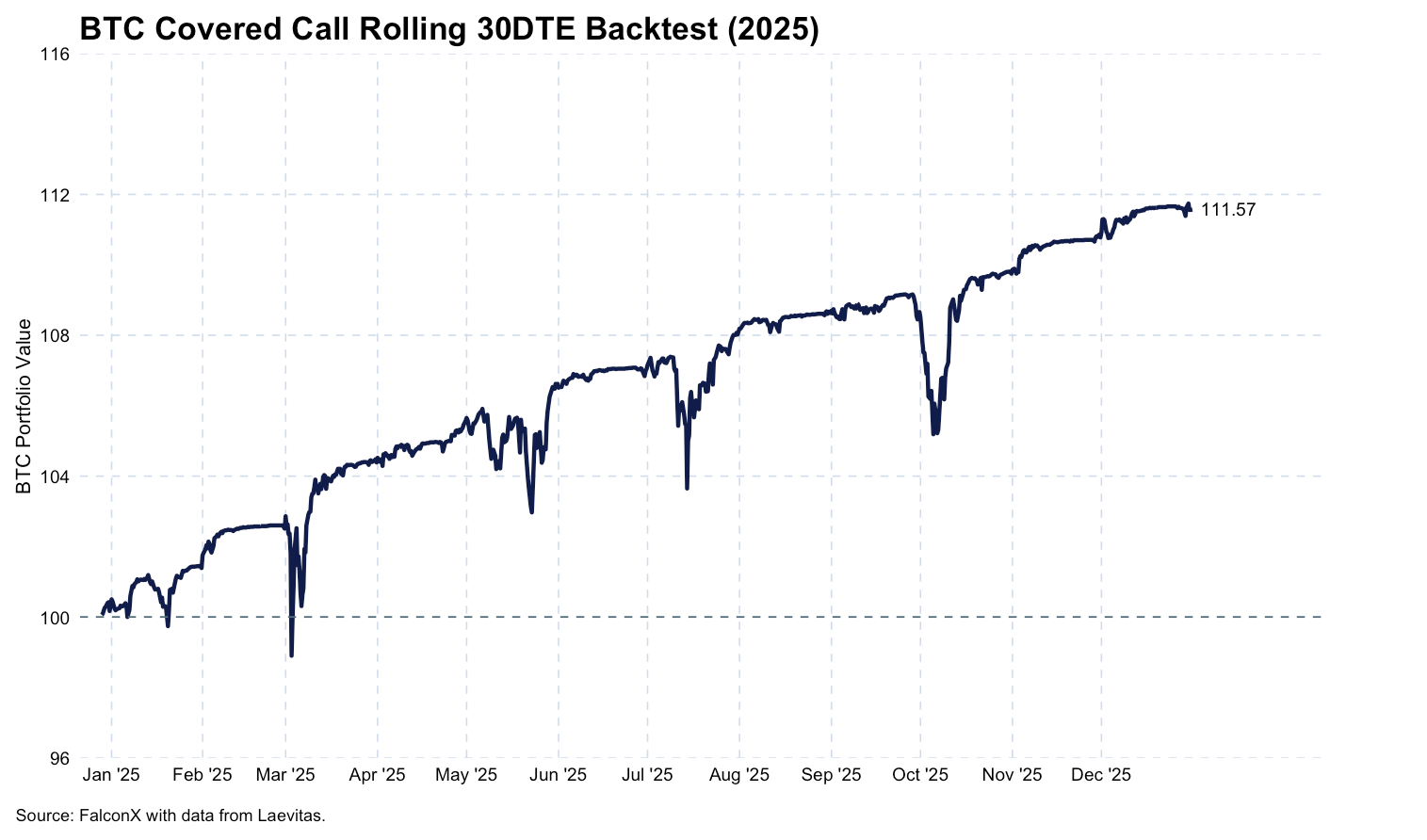

Covered Call Strategy Illustrative Performance (2025)

According to data from Laevitas, a BTC covered call strategy that rolled 1M expiry call overwrites at an average of 17% OTM and 0.15 Delta could have been reasonably expected to produce over 11% of yield in BTC terms in 2025. This highlights how such strategies can be effective methods for incremental income generation in the right market conditions. For SOL, a similar strategy could have returned nearly 17%.

Takeaways

Options strategies such as call overwrites and put selling could help DATs generate income to help improve mNAV or grow their crypto holdings. DATs could benefit by monitoring their mNAV reflexivity to determine the best strategy for them. Options strategies could represent a useful mechanism to enable DATs to generate meaningful incremental income, with the added risk of losing certain upside, requiring thoughtful management of such programs.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a swap dealer with the U.S. Commodities Futures Trading Commission (CFTC) and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is licensed by the MFSA as a Class 2 Crypto-Asset Service Provider (Regulation (EU) 2023/1114). It is also licensed as a Financial Institution (Cap. 376) exclusively for EMT payment services. FalconX’s complaint policy can be accessed by sending a request to complaints@falconx.io

"FalconX" is a marketing name for the FalconX Group and its affiliates. Availability of products and services can be subjected to jurisdictional restrictions and operational capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.