The 6 Charts that Defined 1Q26

The first quarter of 2026 was one of crypto’s most challenging periods in years. BTC fell 22% to close around $66K, adding to its 23% decline in 4Q25, while ETH dropped 29% and SOL declined 33%.

1Q26 saw crypto spot volumes decline 49% YoY, while futures volumes fell 22%. Futures open interest declined from $65B to $56B in the quarter, effectively unwinding the leverage built up from the election cycle. Despite the quarter’s softer activity, BTC’s resilience through the Iran conflict (+9% through April 9, 2026) suggests the positioning reset may be nearing completion, though macro shocks could disrupt the recovery.

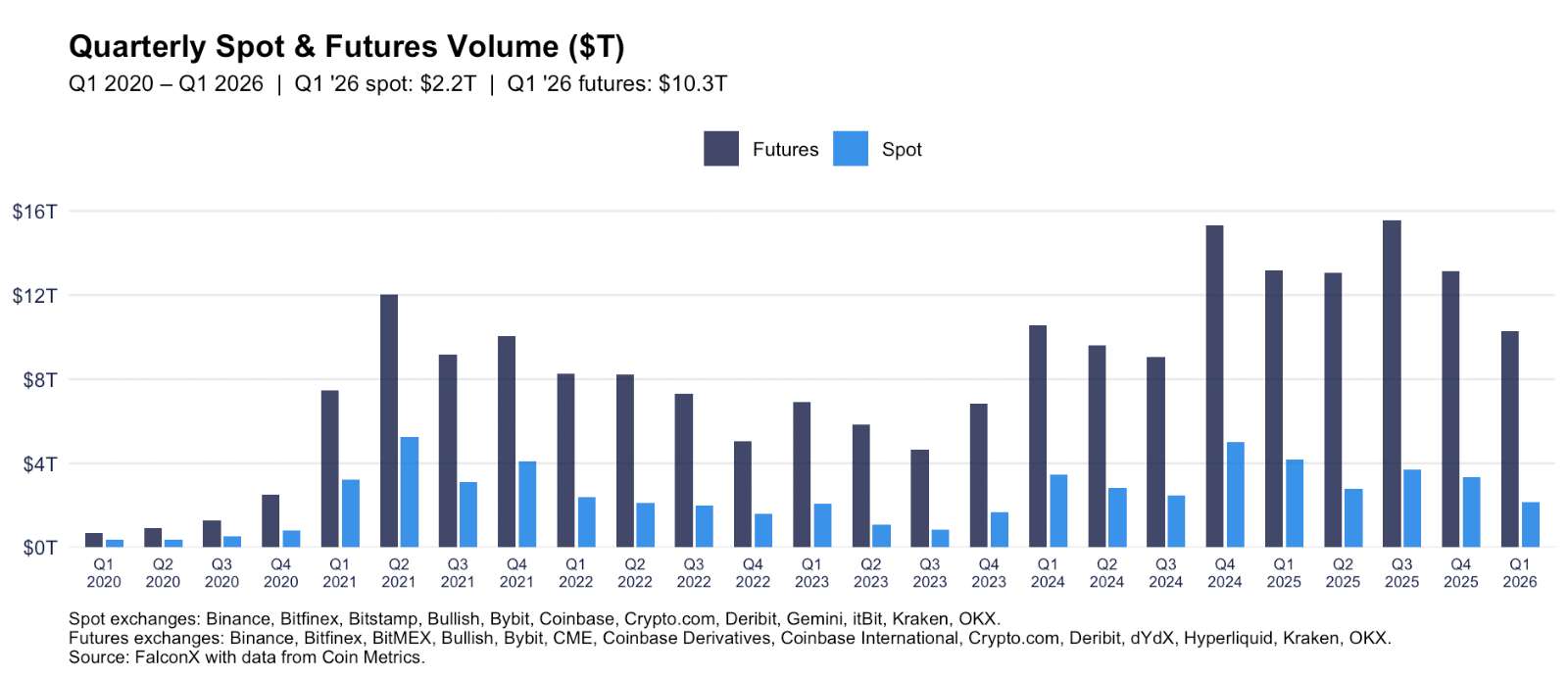

Spot Volumes Hit Multi-Year Lows

Spot volumes across a set of leading exchanges1 totaled $2.2T in 1Q26, -36% from the prior quarter and -49% from a year ago, per data from Coin Metrics. This was the weakest quarter since 4Q23, which saw $1.7T in spot volumes.2 Within the quarter, volumes declined sequentially, with March volumes of $0.6T declining 24% vs January. March spot volumes were down 59% relative to October 2025, when BTC set its all-time high.

Futures volume, across a set of 14 venues3, totaled $10.3T, -22% both QoQ and from a year ago. Futures volumes were the softest since 3Q24 ($9.1T). March futures volumes were 42% below their peak month in 2025 (August).

April spot and futures volumes are running 22% and 15% below their March daily average, respectively, as of April 8. However, this may in part be due to the stock market holiday at the start of the month.

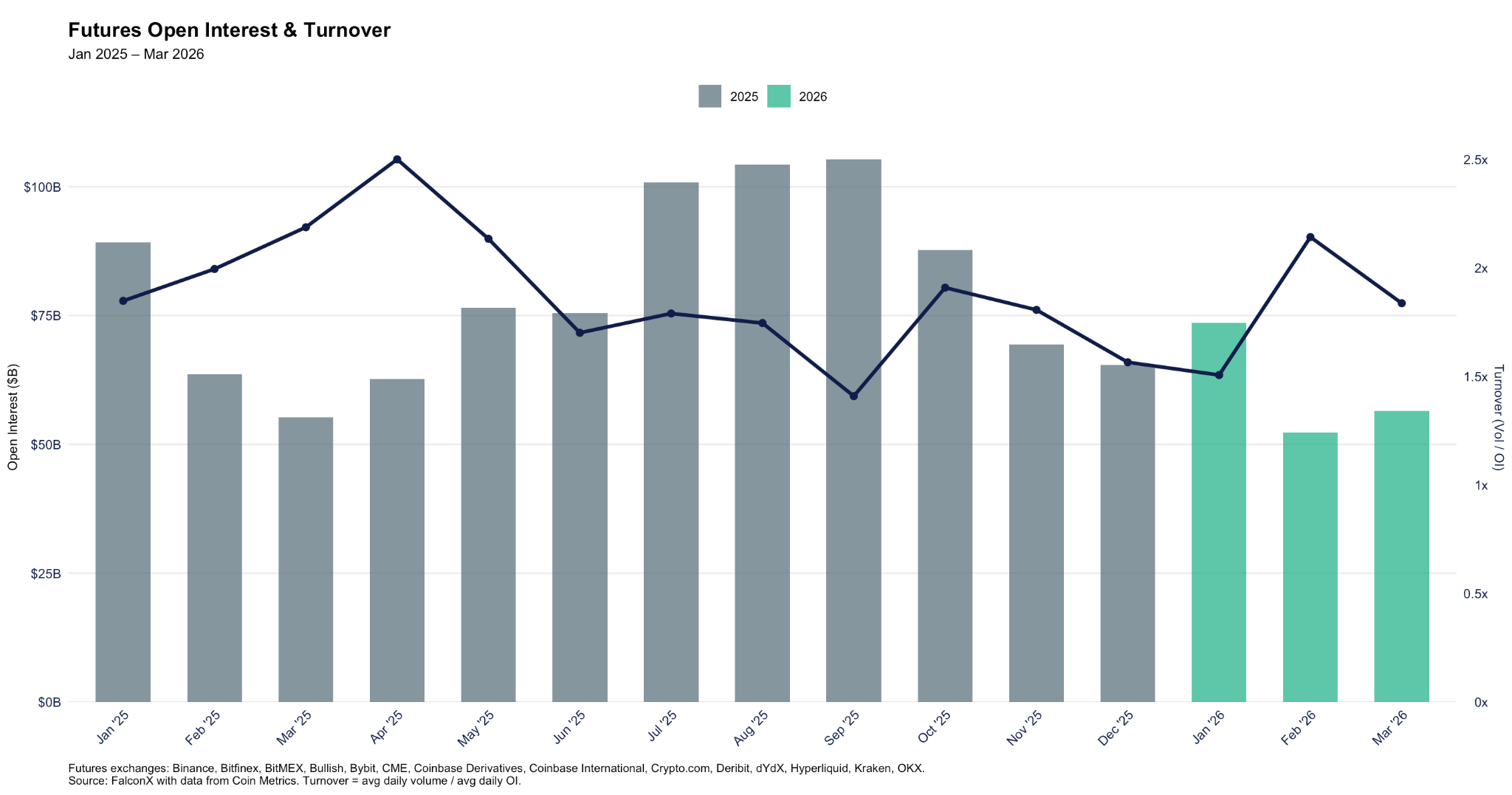

The Open Interest Reset Reaches Mid-2024 Levels

As indicated in the figure below, aggregate futures open interest (OI) ended March at $56.5B, down 54% from October 2025’s $122.2B peak and compares to $65.4B at the end of 4Q25. This brings positioning back to where it stood before the 2024 U.S. presidential election. The turnover ratio (volume / OI) sat at 1.8x in the quarter, well below 2021’s 5–7x range, reflecting a market where more of the OI consists of longer positioning (directional bets, hedges) rather than speculative churn.

The one notable exception was in early February, when turnover rose to over 4.7x, driven by the January 31 and February 5 liquidation cascades, which saw $2.5B and $1.4B in liquidations, per data from Coinglass. This led OI to collapse from $79.8B to $54.5B in roughly two weeks. OI has since stabilized near $56-58B, suggesting the flush may have been the major deleveraging event this cycle.

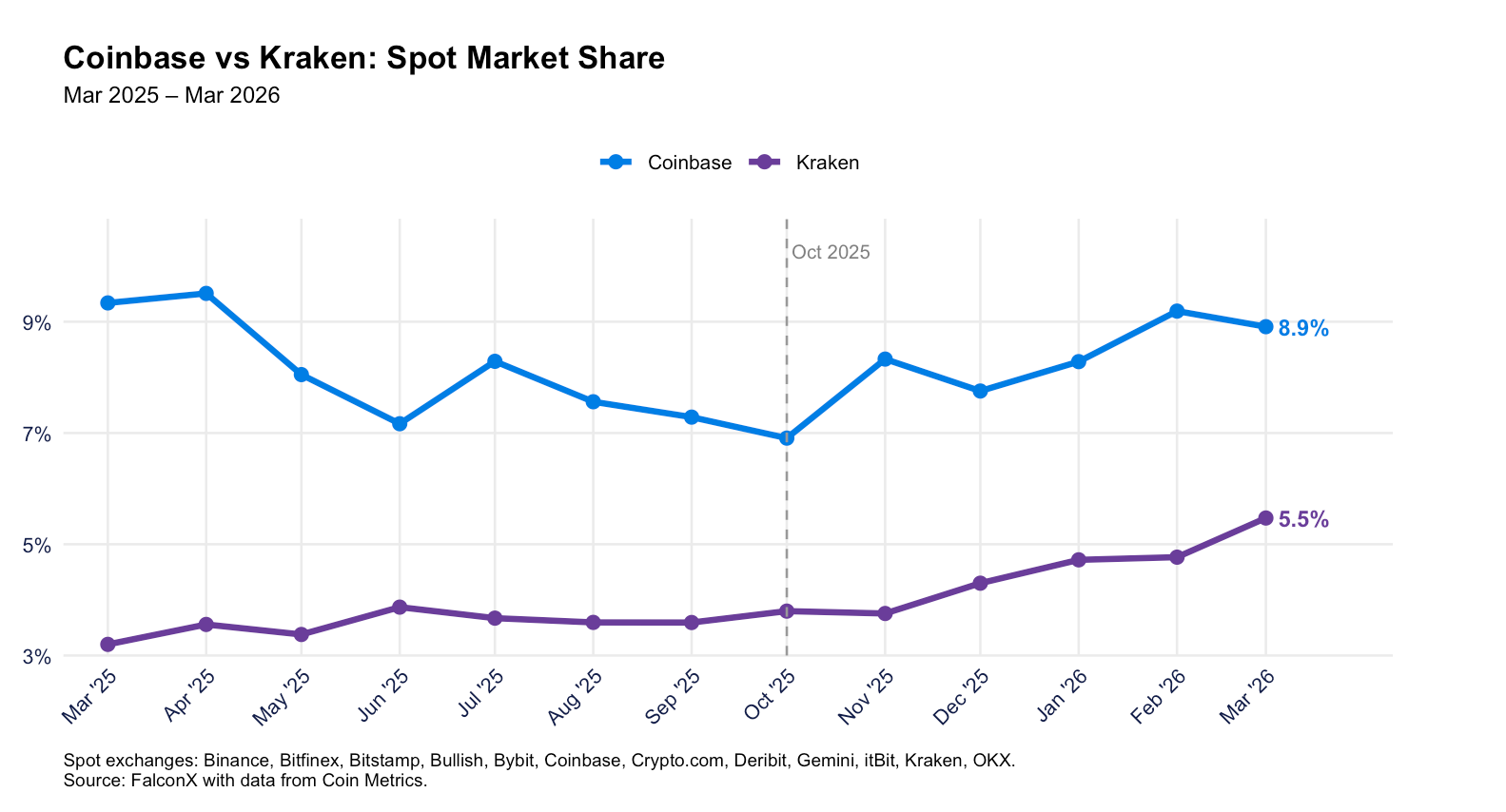

US Venues Are Gaining Spot Share

A quieter but notable trend: US-based spot exchanges are gaining market share as volumes compress. Coinbase and Kraken’s combined share of spot volume increased from 10.7% in October 2025 to 14.4% in March 2026. This appears to be coming in part at Binance’s expense, whose spot market share declined from 54.8% to 43.5% over the period. Bullish also gained significant share in the period (9.8% share in March vs. 4.6% in October), per data from Coin Metrics.

On the futures side, the story is different: CME’s OI share is declining faster than peers. Its total futures OI declined 60% from October 2025 to March 2026, which compares to a 33% decline for Binance over the period. This could reflect basis trades unwinding, with CME annualized basis declining from over 8% in October to around 5% in March, per data from Velo. Meanwhile, Hyperliquid saw its futures open interest jump 16% MoM in March (vs 8% increase across the exchange set).

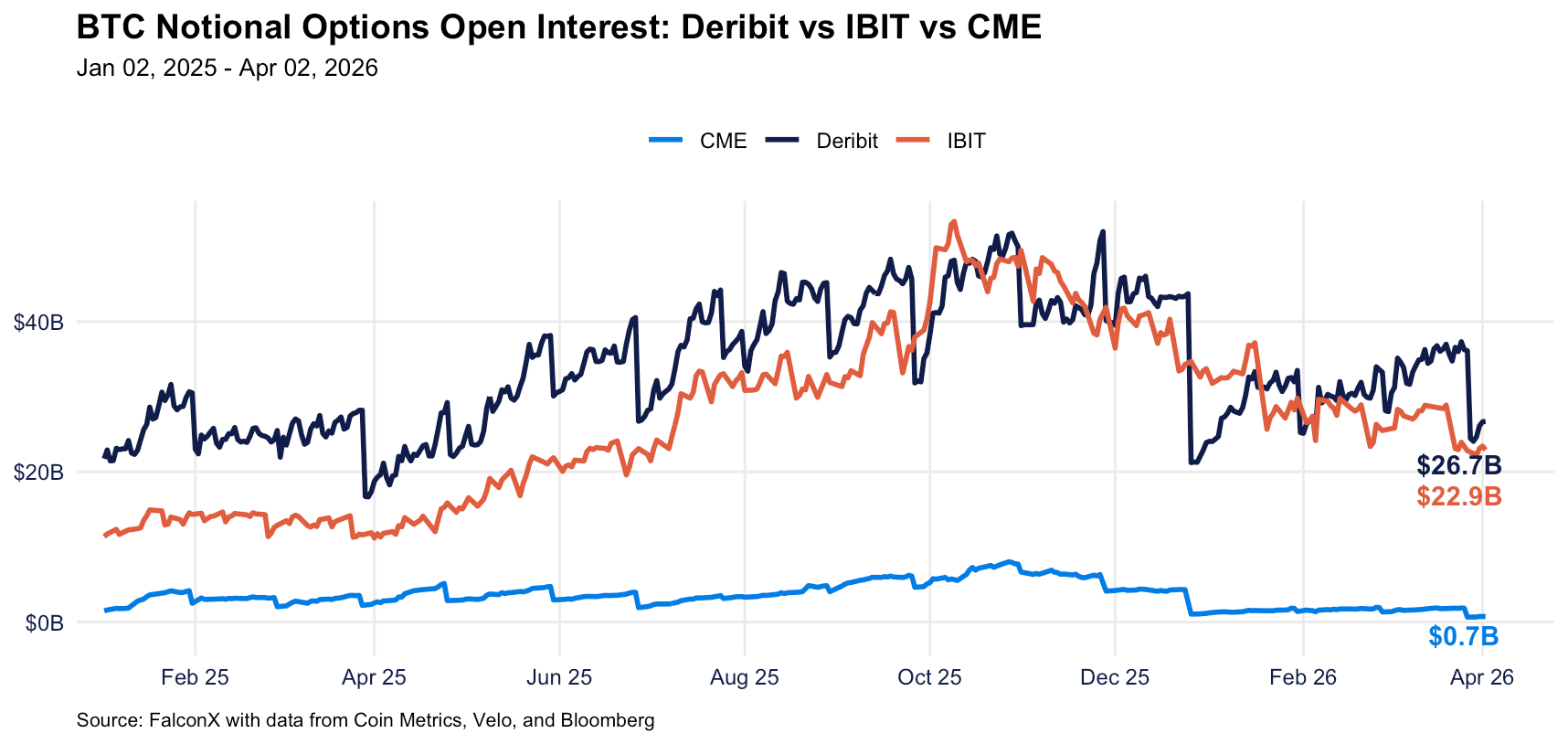

BTC Options OI Undergoes Its Own Reset

The BTC options market experienced parallel deleveraging in Q1 alongside futures. IBIT notional open interest ended the quarter below Deribit OI, reversing a prior trend of IBIT leading the market in OI terms. As of April 2, 2026, Deribit BTC notional OI totaled $26.7B vs IBIT’s $22.9B, as open interest broadly declined following month-end expiries. CME BTC options stood at $0.7B, as quarterly expiries and basis trade unwinds stripped out institutional positioning.

Combined across the three major venues, BTC notional options OI ended Q1 at roughly $50B — less than half the $110B+ that was outstanding at the 4Q25 peak. The next major quarterly expiry on June 26 on Deribit will be a key date to watch for positioning resets, while monthly IBIT expiries (third Friday of each month) continue to drive periodic contract drops that can whipsaw short-dated implied volatility.

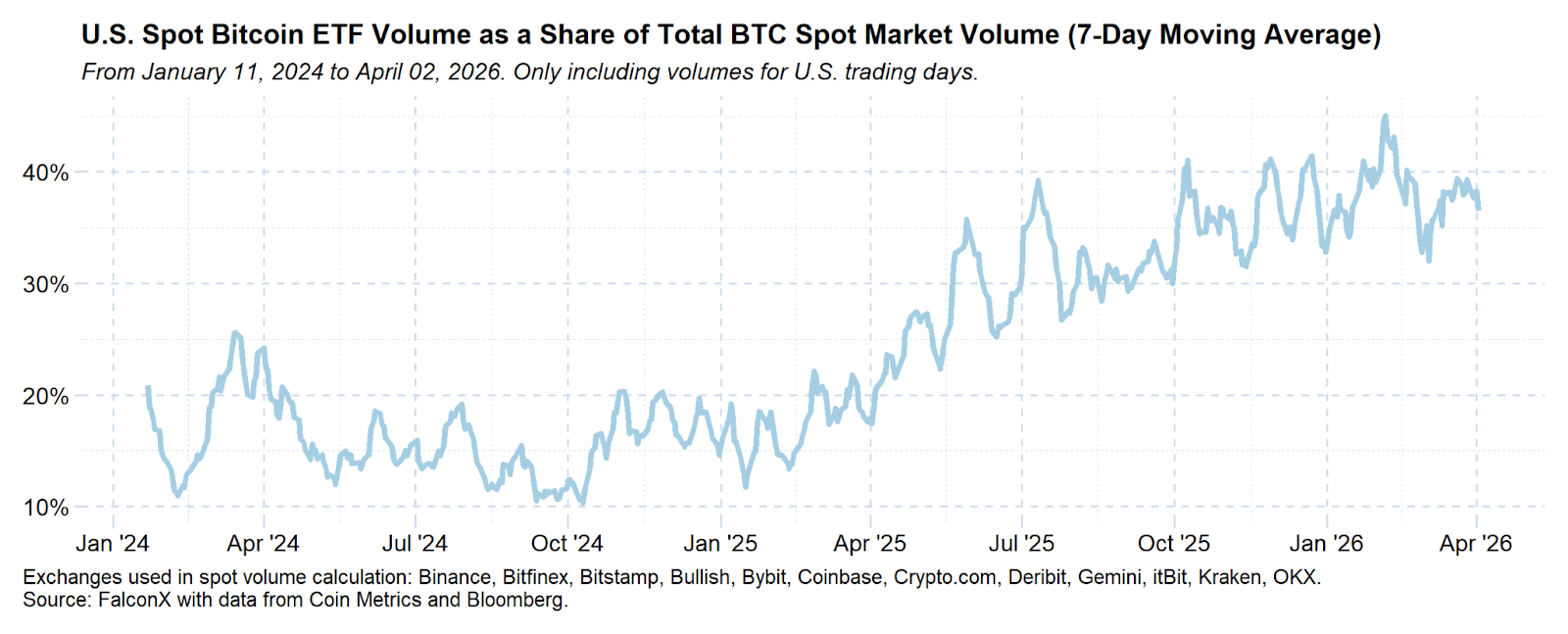

ETF Flows Continue to Gain Share

In 1Q26, spot BTC ETFs remained a driving force of activity in the markets, with their volume totaling over 50% of spot volume4 for the first time, on a daily basis, in early February 2026, before retracing towards quarter end. Potential drivers of this could be traders coming in through familiar wrappers, now that more brokerages have approved spot crypto ETF products to be offered on their platforms. What could potentially move activity back to spot is brokerages rolling out spot capabilities, with Charles Schwab recently reiterating plans to offer spot crypto trading in 1H26, starting with BTC and ETH.

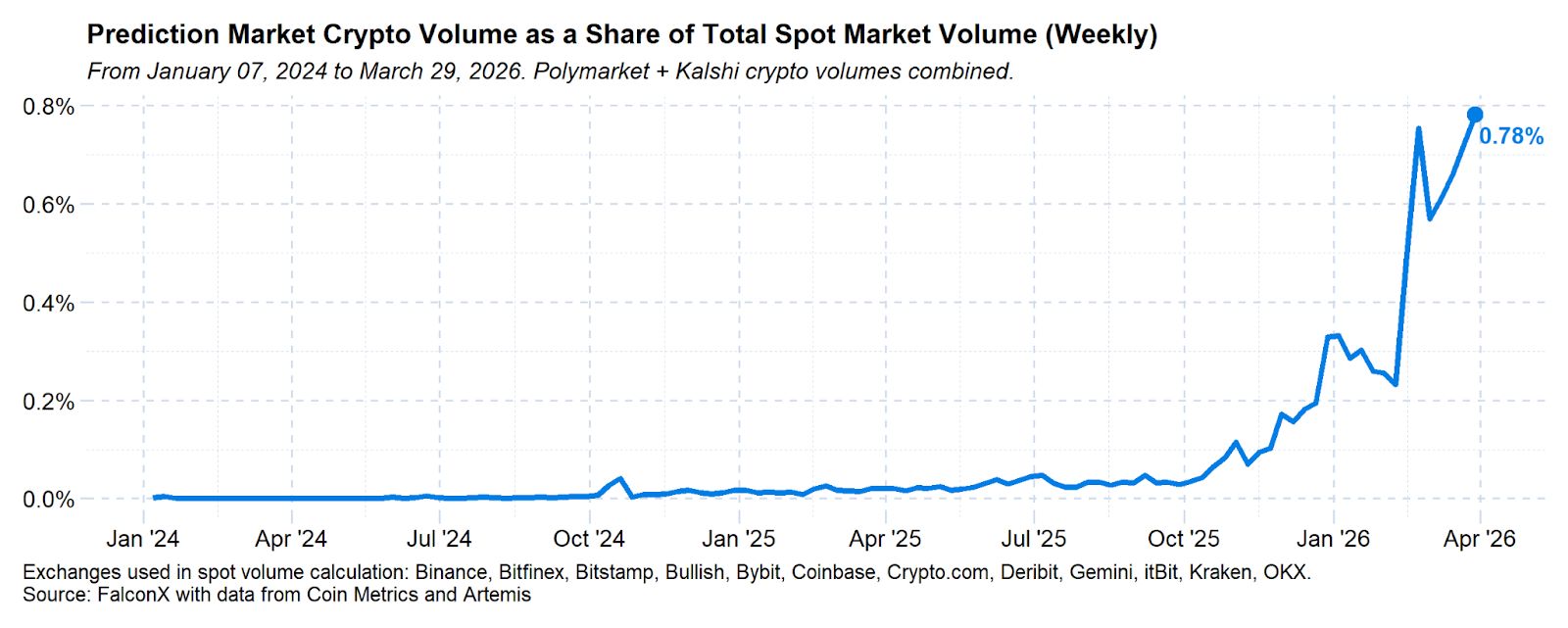

Prediction Markets See Surge in Crypto Volumes

An interesting shift is underway in prediction markets, where leaders Polymarket and Kalshi are seeing a sharp uptick in volumes on their crypto markets. Their combined crypto volumes totaled approximately $900M for the week ending March 29, 2026, per data from Artemis, equivalent to nearly 1% of spot crypto volumes in the period, highlighting the growing significance of these markets. The increase in activity may have been driven by the introduction of ultra-short-term crypto markets, such as 5-min up/down markets.

Looking Into Q2

The positioning data suggests a market that has substantially deleveraged. OI is back to mid-2024 levels and perpetual futures funding rates are below neutral or negative on majors. The Fear & Greed Index is at the extremely low levels that have historically preceded recoveries, though past performance is not indicative of future performance, and the sharp selloffs around early February may have served as a key capitulation event. However, current open interest remains well above prior cycle troughs ($16–20B), positioning the market above historical support levels amid prevailing macro conditions. The Iran conflict, quantum concerns, and upcoming economic data releases will be near-term catalysts to watch heading into May.

1 Spot exchange set includes Binance, Bitfinex, Bitstamp, Bullish, Bybit, Coinbase, Crypto.com, Deribit, Gemini, itBit, Kraken, and OKX

2 According to data from Coin Metrics

3 Includes Binance, Bitfinex, BitMEX, Bullish, Bybit, CME, Coinbase Derivatives, Coinbase International, Crypto.com, Deribit, dYdX, Hyperliquid, Kraken, OKX

4 Exchange set includes Binance, Bitfinex, Bitstamp, Bullish, Bybit, Coinbase, Crypto.com, Deribit, Gemini, itBit, Kraken, and OKX

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd., nor Banzai Pipeline Limited service retail counterparties, and the information on this website is NOT intended for retail investors. The material published on this website is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this website is not and should not be regarded as investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

No discussion of a particular company or product shall be considered an endorsement of such company or product. Past performance is not indicative of future results. FalconX, and its affiliated parties may hold positions in, act as a market maker for, or otherwise have a financial interest in, assets discussed herein, and may benefit from any price movements or transactions involving the subject company. This may change without notice. Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory, and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over-the-counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a swap dealer with the U.S. Commodities Futures Trading Commission (CFTC) and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is a registered Class 3 VFA service provider with the Malta Financial Services Authority under the Virtual Financial Assets Act of 2018. FalconX Limited is licensed to provide the following services to Experienced Investors, Execution of orders on behalf of other persons, Custodian or Nominee Services, and Dealing on own account. FalconX’s complaint policy can be accessed by sending a request to complaints@falconx.io

"FalconX" is a marketing name for FalconX Limited and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.