How the Launch of Spot ETFs Could Dampen Bitcoin’s Volatility

The approval of a wave of bitcoin exchange-traded funds will lead to a more mature market structure

Originally published on Coindesk.

One of the critical ingredients for Bitcoin’s success has been the emergence of new trading infrastructure and investment wrappers that open access to new investors. This trend is now in overdrive with the recent launch of spot BTC ETFs.

Beyond the circles of liquidity providers and trading desks, we haven’t quite appreciated how these monumental changes will change the Bitcoin market structure.

We can expect reduced inherent volatility as this market structure matures. Here, we will explore how a couple of important shifts associated with the launching spot ETFs are poised to facilitate this change.

ETF Fix as a Market Price Reference?

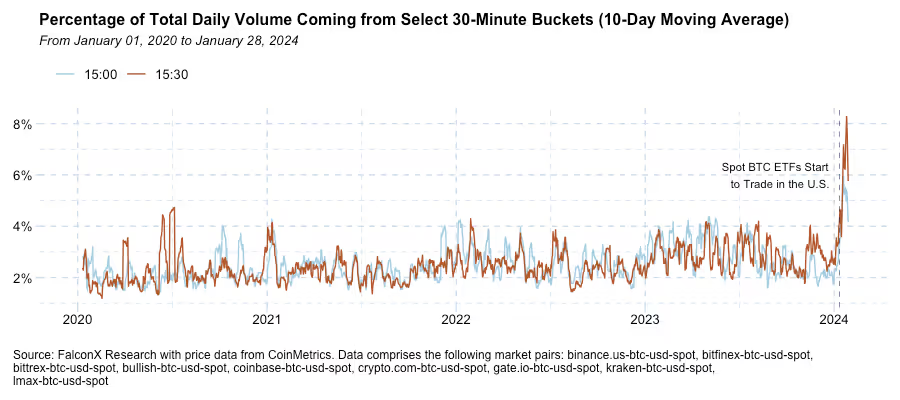

It is no secret that the recent ETF launches have yielded a meaningful uptick in the underlying spot BTC trading volumes. Notably, a disproportionate share of this volume increase has happened mostly between 3 p.m. and 4 p.m. ET, or close to the ETF price fix.

The chart below shows the daily BTC trading volume percentage in the 30-minute buckets starting at 3:00 p.m. and 3:30 p.m. ET for the leading trading pairs. Activity from these two buckets, which regularly accounted for less than 5% of the total daily volume in aggregate, now represents 10-13%.

By providing a transparent and consistent reference point recognized by increasing market participants, the ETF fix allows investors to aggregate large trades around a common time, reducing their market impact and overall market volatility.

A New Options Market Around ETFs?

All three exchanges that currently list spot BTC ETFs have already asked the SEC to allow them to list options on such ETFs. It could take anything between one and eight months for those applications to be evaluated by the SEC, and there are wrinkles related to their clearing and settlement processes.

The Bitcoin options market will likely get a significant boost if this new class of options is given the green light. The Bitcoin options market is currently split between investors who trade in offshore exchanges inaccessible to U.S. persons or on platforms accessible only to large institutions, such as the CME. Allowing options based on spot BTC ETFs could significantly expand the options market beyond these two markets.

Overall, the BTC options market should continue to increase in importance in 2024, even after the massive growth it posted last year. A more developed options market can yield lower volatility because it allows investors to express a broader range of investment strategies and make the most liquid ETFs even more liquid. It also expands the importance of events such as expirations and dealer positioning as price action drivers.

20-Year ETF Legacy Meets the Bitcoin Revolution

It’s exciting to see the ETF revolution now benefit the bitcoin market. The launch of spot BTC ETFs has brought, and will likely continue to bring, an increase in investor participation, perhaps similar to the gold ETF launch in the early 2000s.

More than two weeks into launch, the spot bitcoin ETFs are already clocking in at over $1.5 billion daily trading volume. For context, this volume is about 20% of what bitcoin trades in the spot market on a good day.

As the innovation in crypto ETFs continues, we expect trading activity related to ETFs to continue, which should dampen Bitcoin’s volatility and contribute to the maturation of this emerging asset class.

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd. nor Banzai Pipeline Limited service retail counterparties, and the information in this material is NOT intended for retail investors. This material is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this material is not and should not be regarded as investment advice, investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over the counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a Swap Dealer with the U.S. Commodities Futures Trading Commission and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is licensed by the MFSA as a Class 2 Crypto-Asset Service Provider (Regulation (EU) 2023/1114). It is also licensed as a Financial Institution (Cap. 376) exclusively for EMT payment services.

"FalconX" is a marketing name for the FalconX Group and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.