GBTC Outflows Quickly Receding; Macro Likely to Become a More Important Driver

It is starting to feel like we’re now over the hump of GBTC withdrawals. The latest outflow print came in at less than $400 million, which is still more than what the other issuers gathered in inflows over the past few days but increasingly to a lesser extent.

The total crypto market cap shrunk by 8.9% (or 9.6% excluding stablecoins) to $1.52 trillion (or $1.38 trillion excluding stablecoins). The trend we anticipated last week has largely played out: The two major forces driving BTC spot flows (Blackrock and Fidelity gathering strong inflows, but GBTC bleeding about $500 million in outflows daily) are both tapering off, with the former shrinking faster than the latter. Over the long haul, however, I remain confident that inflows will significantly outweigh these short-term outflows.

It is starting to feel like we’re now over the hump of GBTC withdrawals. The latest outflow print came in at less than $400 million, which is still more than what the other issuers gathered in inflows over the past few days but increasingly to a lesser extent.

There seems to be a market perception that the GBTC outflows, now at $4.8 billion in 10 days, mainly comprise ETF holders flocking to other cheaper alternatives. Although there’s certainly a component related to this, most of the GBTC selling pressure is likely happening due to other reasons.

One example is the FTX bankruptcy estate, which reportedly sold 22 million shares worth about $1 billion. Another potential example is investors who acquired GBTC eyeing the ETF launch and are now moving to new pastures.

This public could be larger than some think. GBTC has traded a little over 300 million shares since the ETF launch. But it has also traded about 600 million shares since the possibility of a spot ETF came into the spotlight: 200 million shares since its NAV discount shrunk to less than 10% as ETF was considered a done deal, another 200 million between then and the Grayscale lawsuit win, and another 200 million between then and Blackrock filling for a spot BTC ETF.

Even considering a high turnover, a small portion of the large amount of GBTC shares traded in the months before the ETF launch selling after the event would translate into meaningful selling pressure. On the other hand, this flow is likely to exhaust itself relatively quickly, which is the trend that we might have started to see over the past few days.

This might be behind the recent partial recovery to above the $40k level.

However, what makes the near future more complex are potential changes in the global liquidity environment that can impact risk assets more generally and crypto in particular.

Just this week, the Fed announced that it will not renew its Bank Term Funding Program (BTFP) on March 11 (as most expected), Q4 U.S. GDP crushed expectations and came in at a solid 3.3%, and the December core CPE just clocked in at below 2.0% annualized over the last three and six months.

The always insightful Arthur Hayes recently did an excellent job identifying the critical macro factors that can drive risk assets, and crypto by extension, throughout 2024, including the path the Fed will take to cut rates, the 2024 presidential election, new supply chain pressures, and more.

CME Fed Funds futures are pricing 98% odds of a no change in the next FoMC meeting next

Wednesday. After that, however, the field looks a lot more open.

Overall, I expect macro to become a more meaningful driver for crypto going forward.

Other Top Trends We're Watching

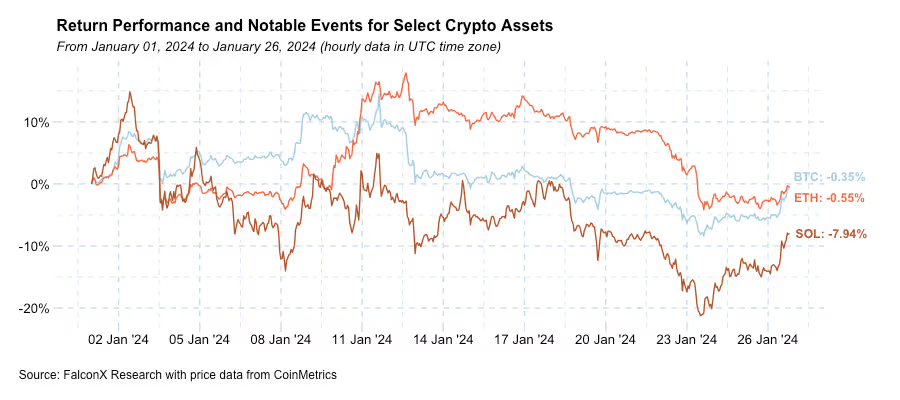

FalconX Trading Desk Color: BTC crossed our desk at 2.6x more volume than ETH, as the leading crypto asset continues to lead institutional trading activity on the back of ETF flows. Buy/Sell ratios varied across different investor personas. Hedge funds and prop desks came in mostly on the sell side, while venture funds and wealth managers were mostly active on the buy side. BTC also continues to print higher buy/sell ratios than ETH, even adjusted for the ETF flow that tends to skew more to the buy side. Among alts, we saw activity in assets such as SOL (both buy and sell side), MATIC (mostly sell side), and other L2 tokens (mostly buy side).

Sharp Price Correction Triggered Remarkably Low Liquidations: Following the intraday local market top on the first day of the spot BTC ETF launches, BTC went through its first correction of over 20% since mid-August. Even though this retracement happened on the heels of open interest in the futures market approaching levels reached only at the highest points of the previous all-time highs, it was surprising to see how smooth liquidations have been.

As the chart below shows, BTC and ETH long liquidations clocked in above $100 million in only one day since the recent local top. One potential reason for this relatively smooth number is that a big portion of the futures OI increase came from the CME, which tends to embed lower leverage than perpetual futures.

Still, more frequent and larger liquidation events than we saw in 2023 will likely remain in place as bull market trends continue to develop.

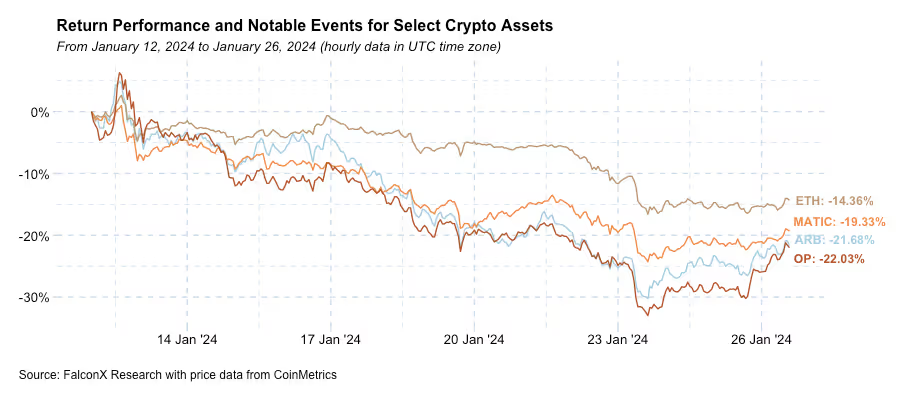

Token Unlocks Season Ready to Reclaim the Spotlight: According to data from TokenUnlocks and DefiLlama, DYDX will add 10.6% to its current circulation supply over the next seven days. Other large assets with significant events in the short term include OP and WLD, unlocking 2.8% and 19.0% of their circulating supply over the next seven days. Further down the road, APTOS and ENS will unlock 7.4% and 3.1% over the next 15 days, respectively.

The leading event, however, will be the large ARB token unlock on March 16, which will unlock 1.11 billion tokens or a whopping 87.2% of the current circulating supply. ARB has been down over the past two weeks but roughly in line with its peers OP and MATIC. Over the next couple of months, however, ARB’s relative performance may falter due to the large upcoming overhang.

Have a great weekend!

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd. nor Banzai Pipeline Limited service retail counterparties, and the information in this material is NOT intended for retail investors. This material is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this material is not and should not be regarded as investment advice, investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over the counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a Swap Dealer with the U.S. Commodities Futures Trading Commission and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is licensed by the MFSA as a Class 2 Crypto-Asset Service Provider (Regulation (EU) 2023/1114). It is also licensed as a Financial Institution (Cap. 376) exclusively for EMT payment services.

"FalconX" is a marketing name for the FalconX Group and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.