Galloping Into The New Year: Crypto’s Key Shifts for The Year of The Horse

.png)

Crypto stands at a pivotal moment going into the Year of the Horse. The space has seen a steady pace of constructive headlines despite disappointing price action, setting the stage for a potential reversal later this year.

The latest selloff at the start of February has led to the question of whether crypto is in a temporary bear market or extended winter. In the report, we highlight current market trends that could answer this and flag the market shifts that may accelerate throughout the Year of the Horse.

Trends Coming Out of the February Selloff

Key Indicators Point to Oversold Levels

BTC’s move down from its all-time high of $126K in October to breaking under $60K in February has culminated in several indicators suggesting we may be close to forming a bottom at the beginning of the Year of the Horse, if history repeats.

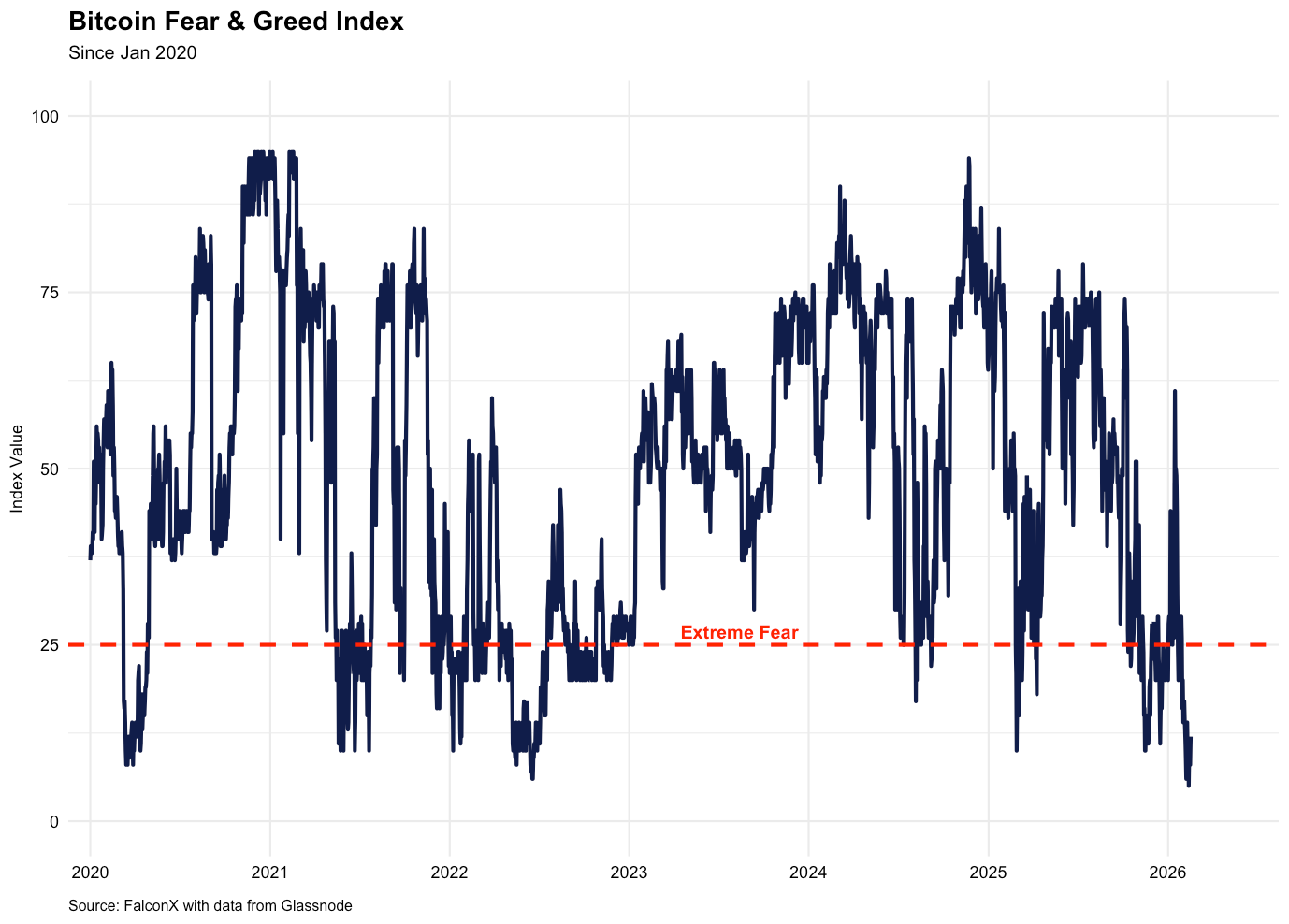

The Fear & Greed Index stood at its lowest point ever as of February 10, 2026, highlighting crypto sentiment is very low and that market participants may be cautious to engage in the market. Sentiment is worse than FTX, Celsius, and the March 2020 crash, despite no obvious triggering event this time around driving prices lower. In those prior situations with similarly low readings, the market ultimately rebounded, suggesting a potential opportunity for positioning.

Another indicator suggesting BTC is oversold is NUPL (net unrealized profit loss), which suggests holders today are deeply underwater relative to the price when they last moved their coins on-chain. Historically, sharp drops under -0.2, have coincided with capitulation or bottom events. On Feb 5, short-term holder (accounts under 155 days) NUPL stood at close to -0.48 per data from Glassnode.

The Mayer Multiple, a gauge of how far BTC is from its 200D moving average, also suggests oversold conditions. It has most notably flashed around market bottoms in 2020, 2021, and 2022.

Market Structure Update: Volumes Spike to Highs, Options Activity Dominate

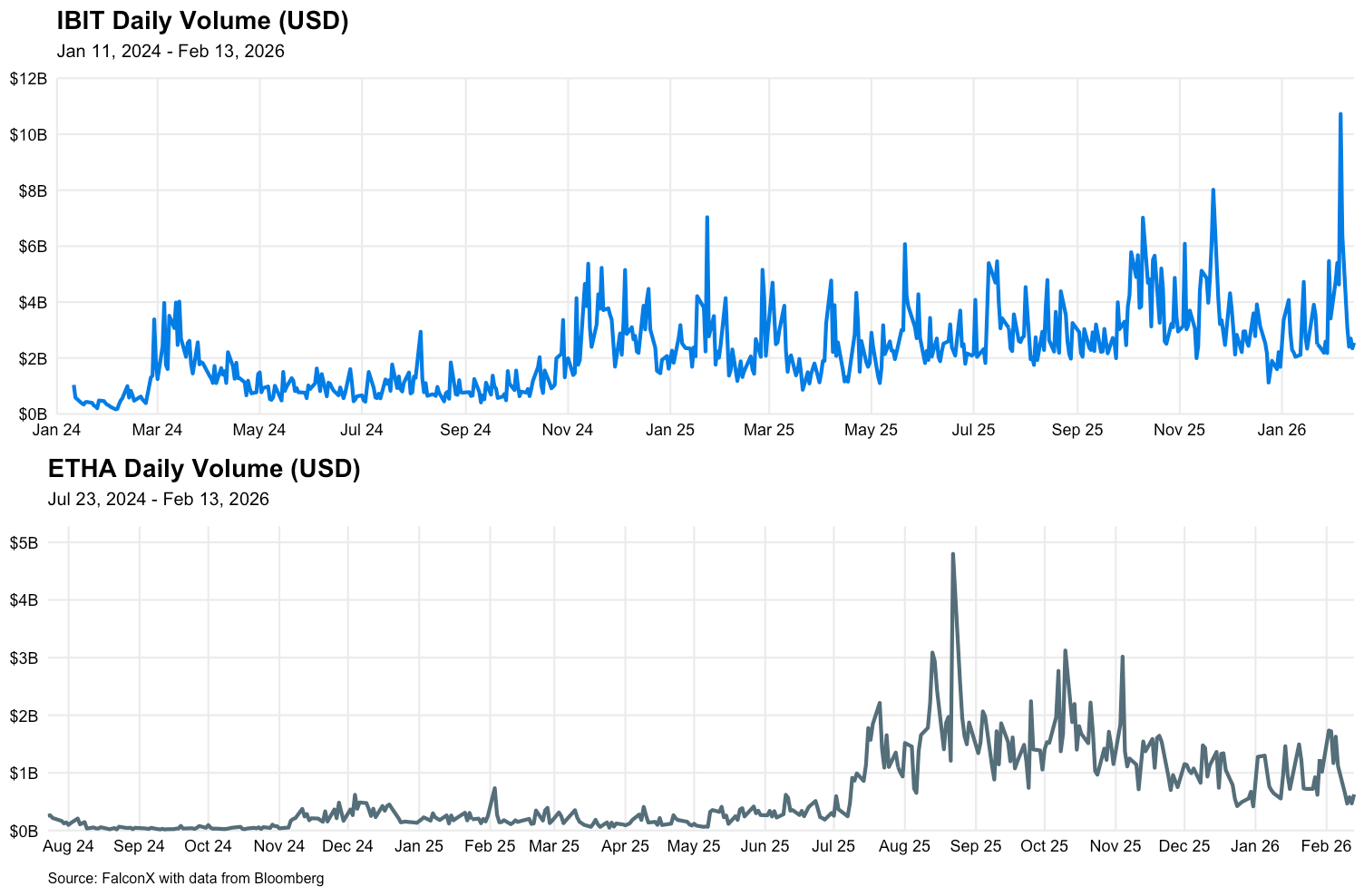

A key component that has marked prior capitulation events is a surge in volumes, as participants rush to exit positions. This was seen both in traditional crypto instruments and spot crypto. IBIT saw record volumes ($10.7B) on February 5, 2026, 53% above its volumes on October 10th, per data from Bloomberg. This coincided with record IBIT options activity that day in contract terms, with put volumes nearly exceeding call volumes. On the other hand, volumes the same day for ETHA, the leading ETH ETF, were 48% below its volumes on October 10th, 2025, further suggesting the move was largely BTC-driven.

Spot Volumes

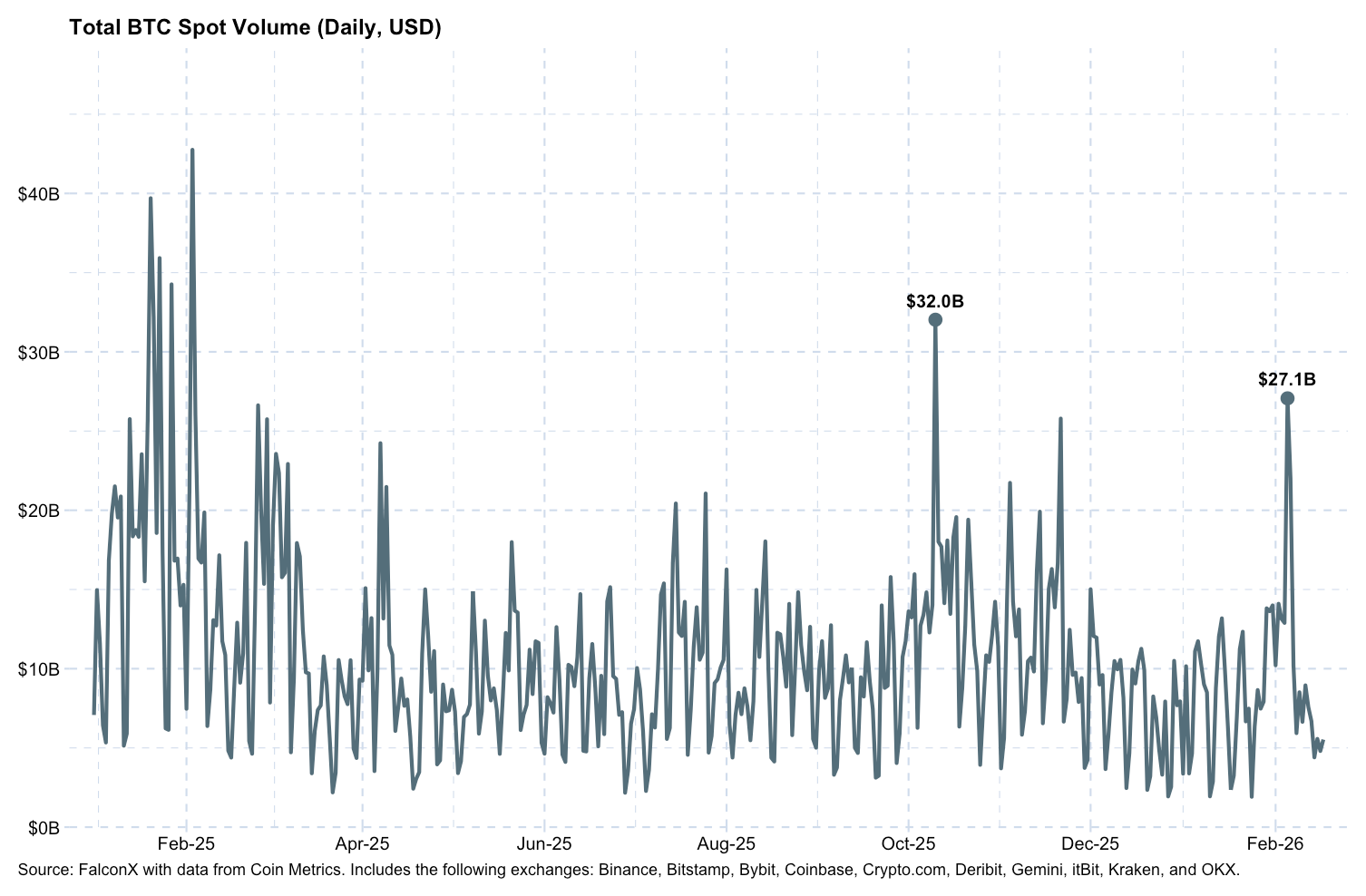

Combined BTC volume across leading venues also approached 10/10 highs, with volume of approximately $27B on February 5, 2026, comparing to $32B previously (-15%), according to data from Coin Metrics. U.S. venues saw relatively higher spot BTC volumes, with Coinbase’s spot BTC volumes 25% above its 10/10 levels, while Kraken’s increased roughly 33%. Gemini and Bitstamp saw spot BTC volumes 77% and 54% above those prior levels, respectively. This suggests activity may have been concentrated in the U.S. session or could imply a shift in volumes to regulated venues.

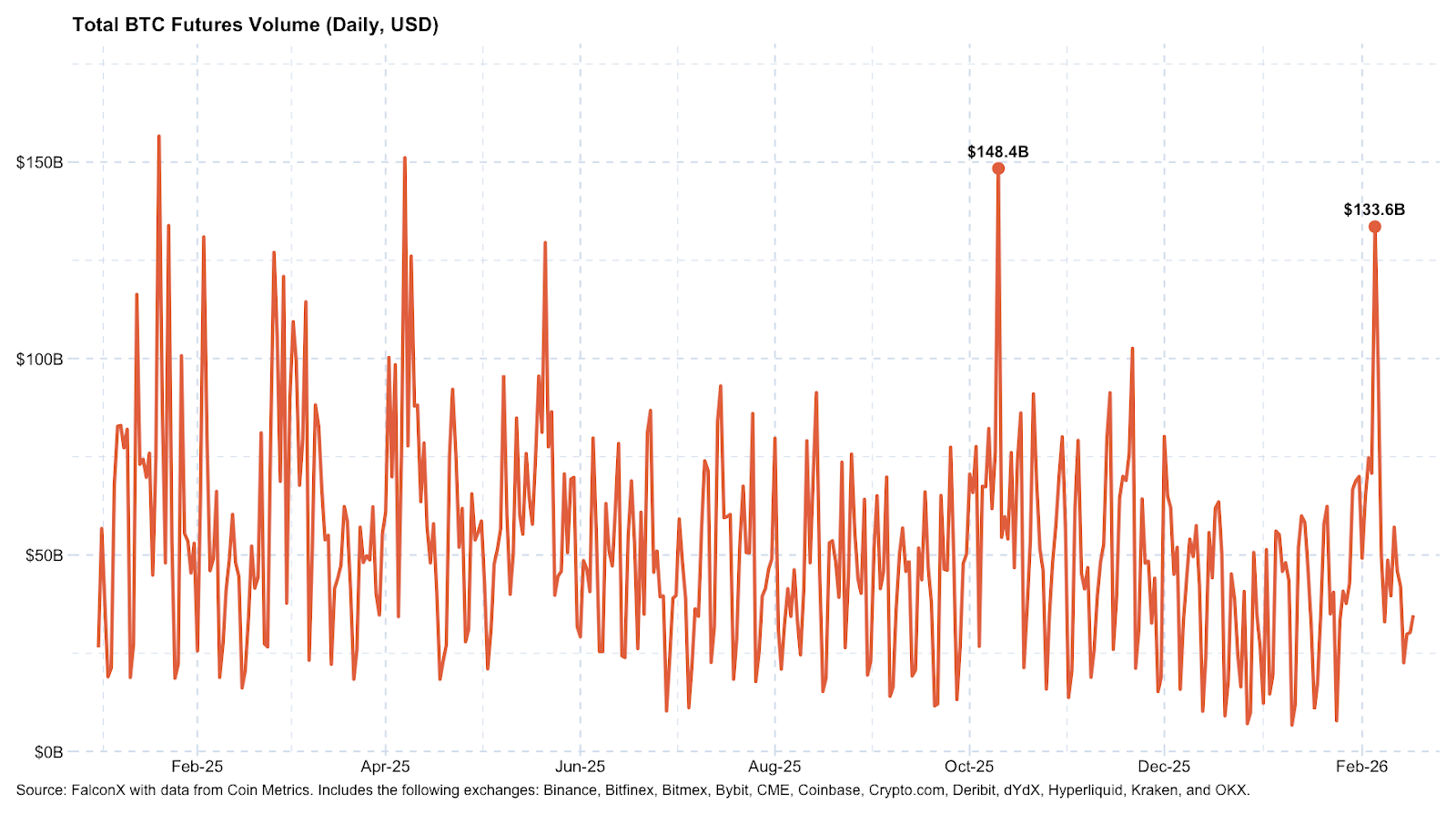

Futures volume showed a similar story, with aggregate BTC futures volumes of $134B on February 5, 2026, which compares to $148B (-10%) on October 10, 2025. Binance BTC futures volumes of nearly $58B compared to $61B in October, also demonstrating elevated levels. Notably, BTC futures volumes on CME and OKX were above their 10/10 levels, rising 20% and 9%, respectively. The elevated CME volumes also suggest the selloff was US-session driven.

Options

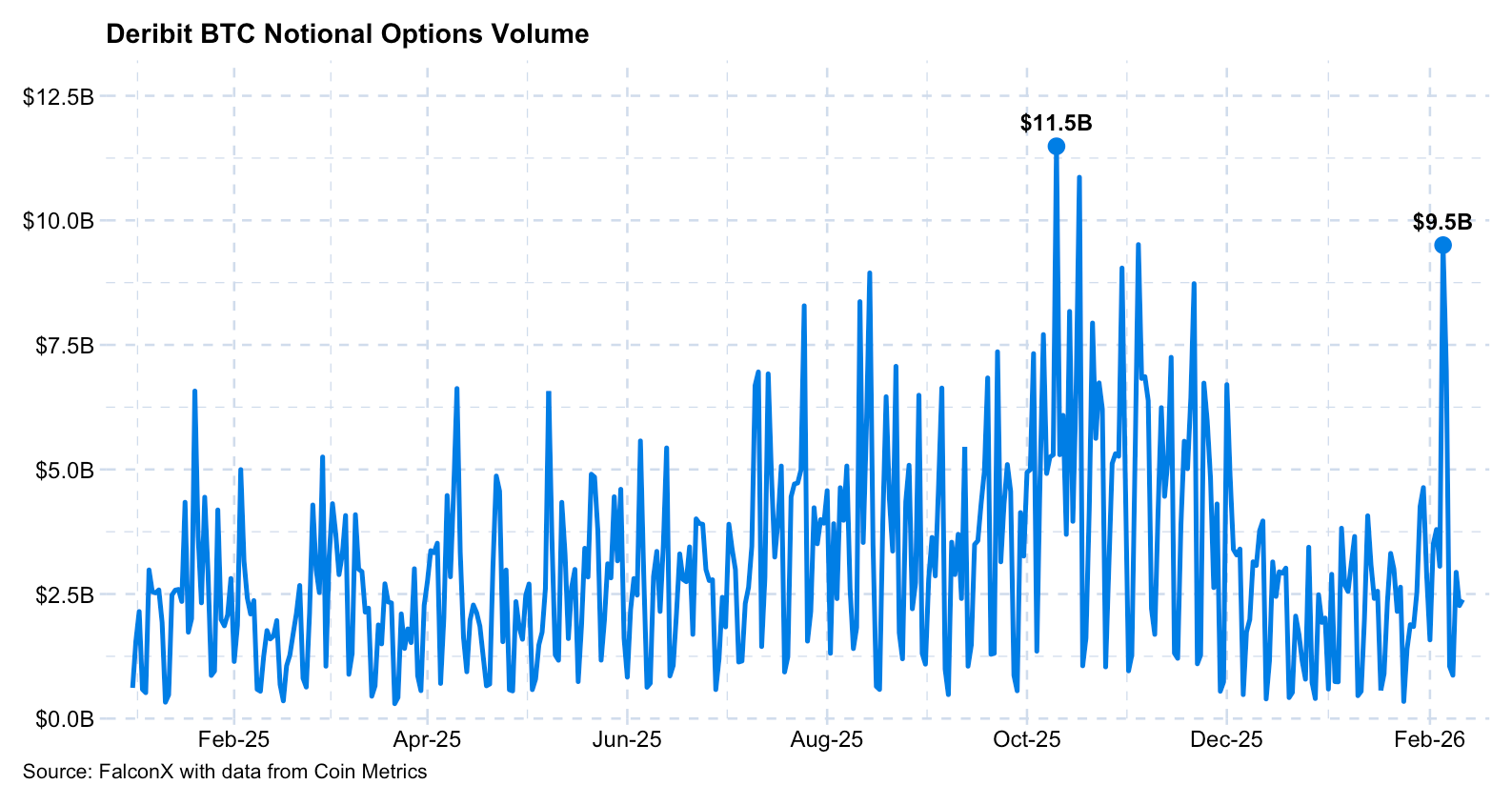

Deribit also saw elevated notional BTC options volumes, highlighting the record IBIT options activity was also reflected in crypto-native markets.

IBIT Becomes Meaningful Player in Options

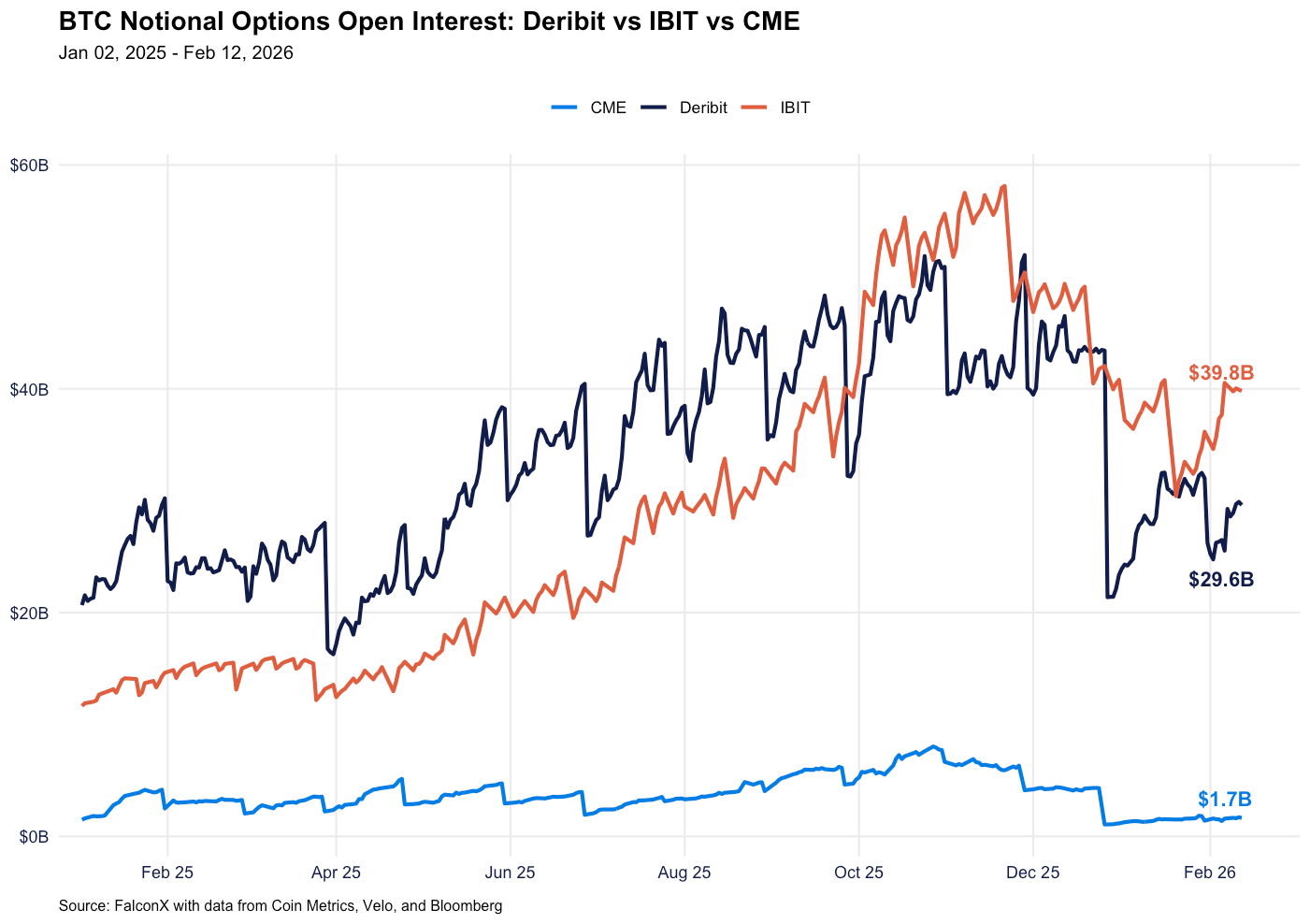

As we enter the Year of the Horse, BTC options OI across Deribit and IBIT have both trended up YoY, with IBIT OI more than doubling over this period. IBIT has emerged as a dominant player in the BTC options space, flipping BTC in September 2025, and has remained as the leading venue by notional open interest since then, with nearly $40B of open interest as of February 12, 2026, which compares to $30B of BTC open interest at Deribit. This translates to a market share of 56% for IBIT across BTC options and exemplifies the broader theme of crypto convergence with traditional finance. Underscoring the growth in IBIT, Nasdaq requested permission in November to increase the position limits for IBIT options by 4x, for which the SEC has designated February 24, 2026, as a deadline to make a decision.

The growth highlights how options dealer hedging can increasingly impact the market by dampening price action and can help anchor price action to US market hours. This would support the recent trends we are seeing in IBIT volumes and options activity around the recent selloff, which was concentrated in US hours.

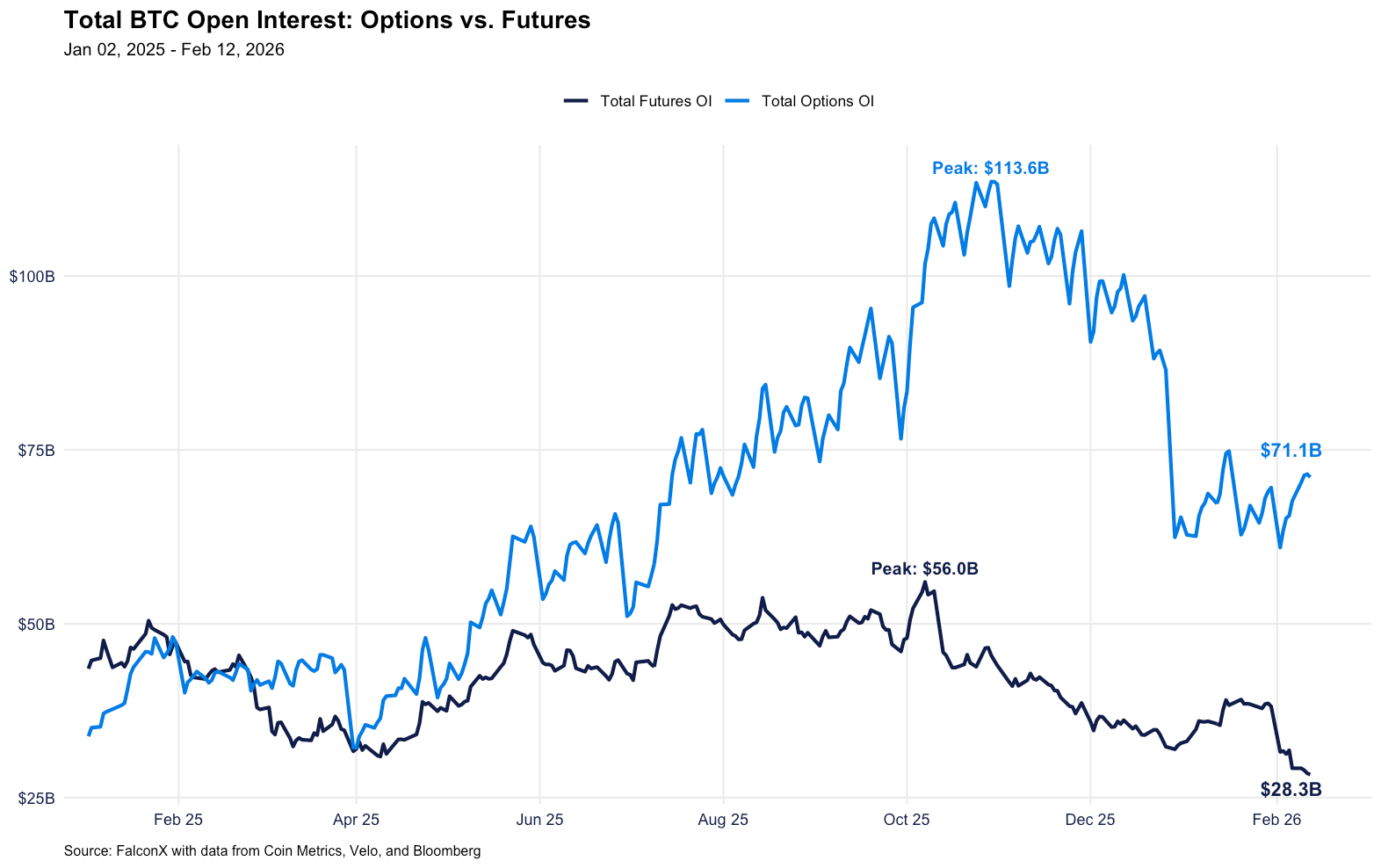

One other trend that will likely continue throughout the Year of the Horse is the options market remaining larger than the futures space. This has accelerated after the 10/10 crash, potentially as traders are more wary of potential ADL risks with perps.

As of February 12, 2026, total BTC options notional open interest (IBIT, Deribit, CME) totaled $71B vs $28B in BTC futures open interest amongst leading venues. BTC futures have been more impacted by deleveraging following 10/10, with open interest declining approximately 50% from their peak in the year, while options open interest declined 37%. BTC options now make up nearly 70% of the BTC derivatives complex versus around 45% a year ago. Within the BTC futures complex, CME and Binance remain the largest players, with market share of 27% and 26%, respectively, although both have seen steadily declining open interest from October.

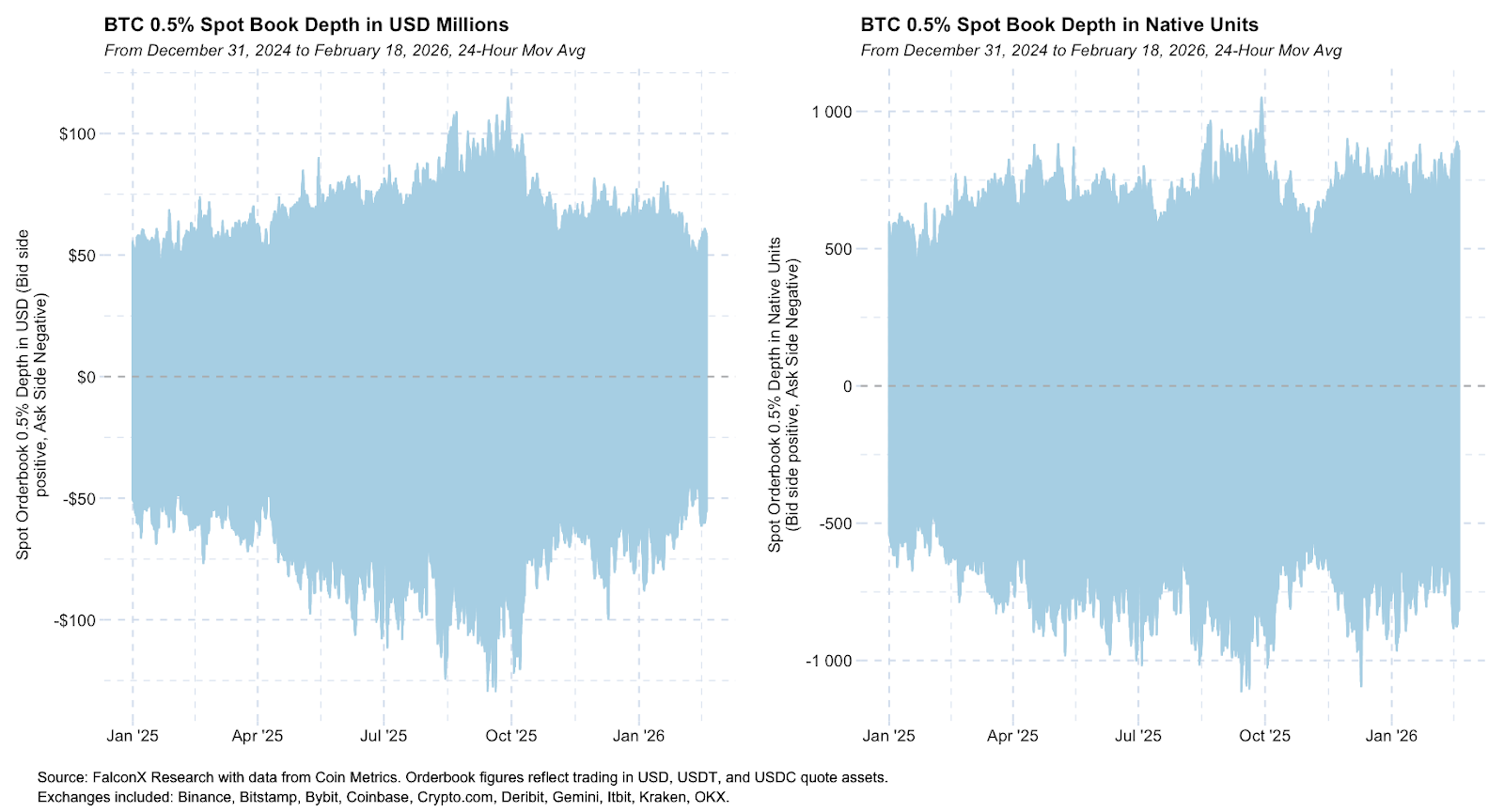

Choppy Waters May Prevail in The Year of the Horse

We anticipate that crypto will remain highly volatile until liquidity returns. Orderbook depth reveals BTC liquidity remains 50% lower in USD terms than its peak last year in September, and is 14% below those levels in BTC terms.

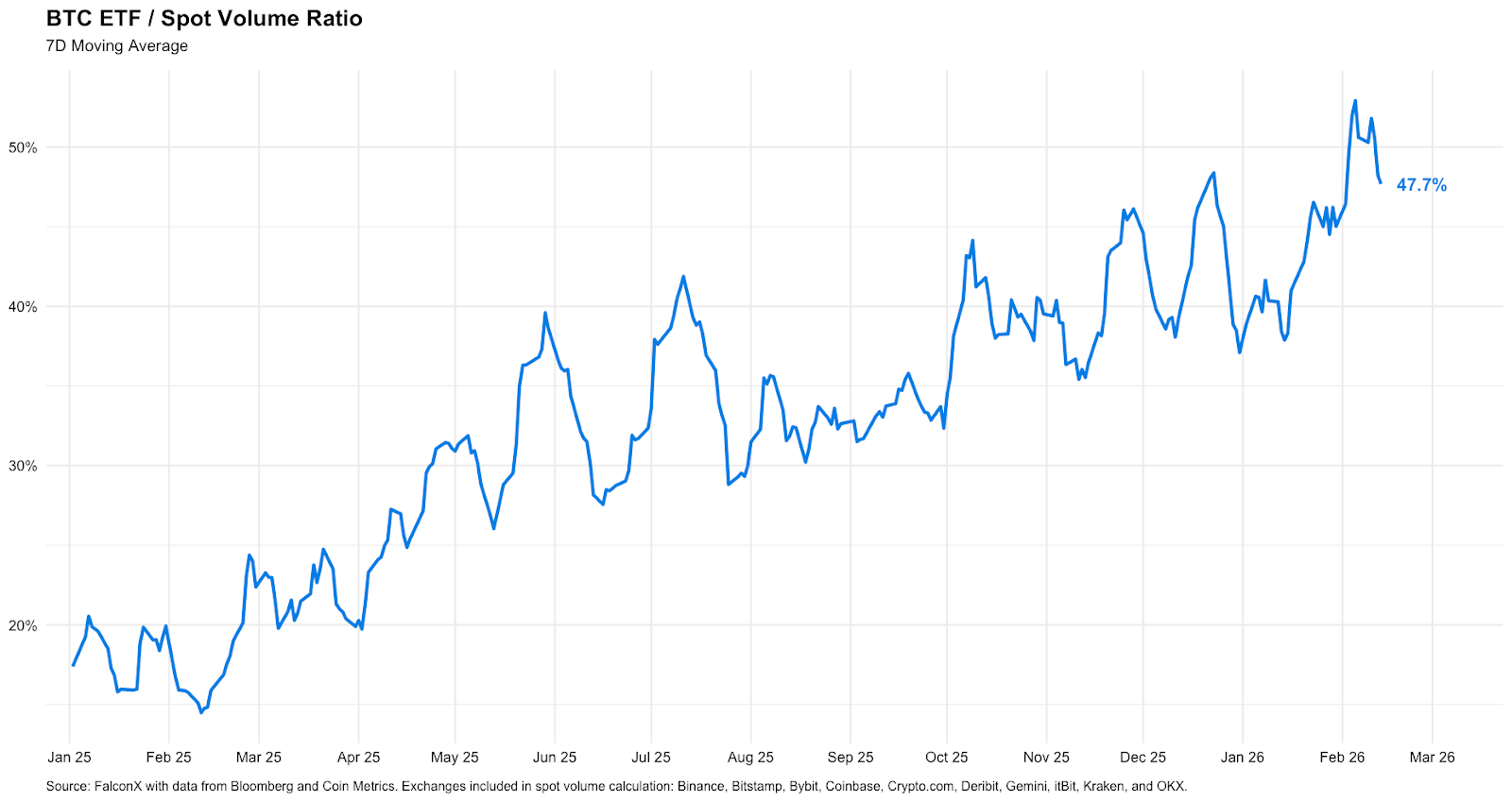

ETFs Taking Growing Share of Crypto Volumes, While DAT Relative Volumes Decline

2025 saw both DATs and ETFs see a surge of interest. DATs proliferated beyond just BTC, with multiple ETH and SOL DATs launching. One key reason DATs may have captured so much investor attention is that they broadened access to crypto for participants whose brokerages may not have supported crypto ETFs yet.

That is changing, as more crypto ETFs come to market following the SEC’s generic listing standards, and as major wealth platforms, including Vanguard, Morgan Stanley, and Bank of America, now allow crypto ETFs to be offered to their clients. Consequently, we expect ETFs to be an even greater driver of volumes going forward.

Most recently, BTC ETFs have climbed to around 50% of BTC spot volumes per data from Bloomberg and Coin Metrics. BTC DATs have declined from nearly 80% of BTC spot volumes earlier in 2025, to 38% as of February 13, 2026.

Notably, these figures differ from other majors such as Ethereum and Solana. While ETH ETF share of ETH spot volume generally increased in 2025, it most recently stood at 24%, down from nearly 35% last month. ETH DAT share of ETH spot volumes declined from over 50% in the summer of 2025 to 15% most recently. SOL is also seeing its ETFs in their infancy, but nevertheless taking a growing share of spot volumes. These launched in October 2025 and now comprise 3% of SOL spot volumes.

Demonstrating how ETFs are able to perform well despite recent volatility are newer launches such as the XRP, SOL, and LINK ETFs. These have seen cumulative net inflows of $1.2B, $875M, and $81M, respectively, as of February 13, 2026, despite being just a few months old, per data provider SoSoValue.1

Themes Shaping the Year of the Horse

RWA and TradFi Convergence

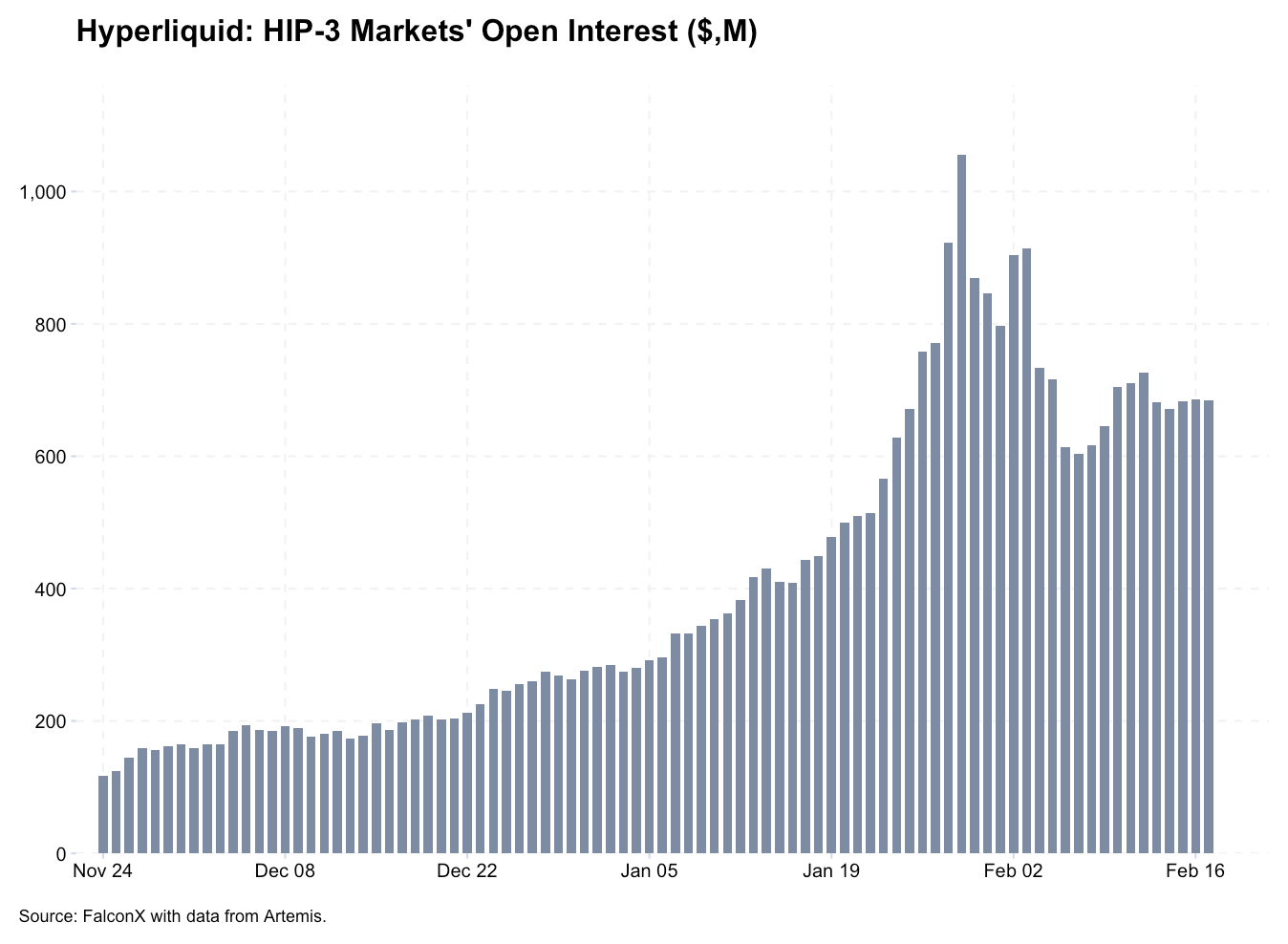

One area of potential opportunity this lunar year is the convergence of TradFi and crypto. Already, we are beginning to see blockchain-based systems be used for trading traditional markets. Hyperliquid is a great example of this, combining its leading non custodial, decentralized perps platform with markets for equities and commodities, also known as its HIP-3 markets.

HIP-3 markets have reached record volumes and open interest in the past few weeks, comprising as much as 15% of total open interest on Hyperliquid. This has been driven by markets on silver, gold, and equity indices (XYZ100), as well as on leading technology stocks. Research suggests that Hyperliquid was able to deliver tighter spreads than traditional silver markets. This has helped drive relative outperformance in HYPE (+23% YTD as of February 17, 2026, which compares to -24% for BTC).

Prediction markets are also seeing record volumes on adoption of trading of real-world event contracts. Several leading prediction markets such as Polymarket are blockchain-based, highlighting the confluence of these areas.

In addition, vaults are becoming a major theme in the RWA space, in theory enabling traditional investment managers to customize and broadly offer strategies. Importantly, given their curation and controls, they are seen as the gateway for banks to enter the on-chain lending space. Most recently, Morpho announced a cooperation agreement with Apollo to support on-chain lending markets on Morpho’s protocol.

Labs vs DAO Alignment

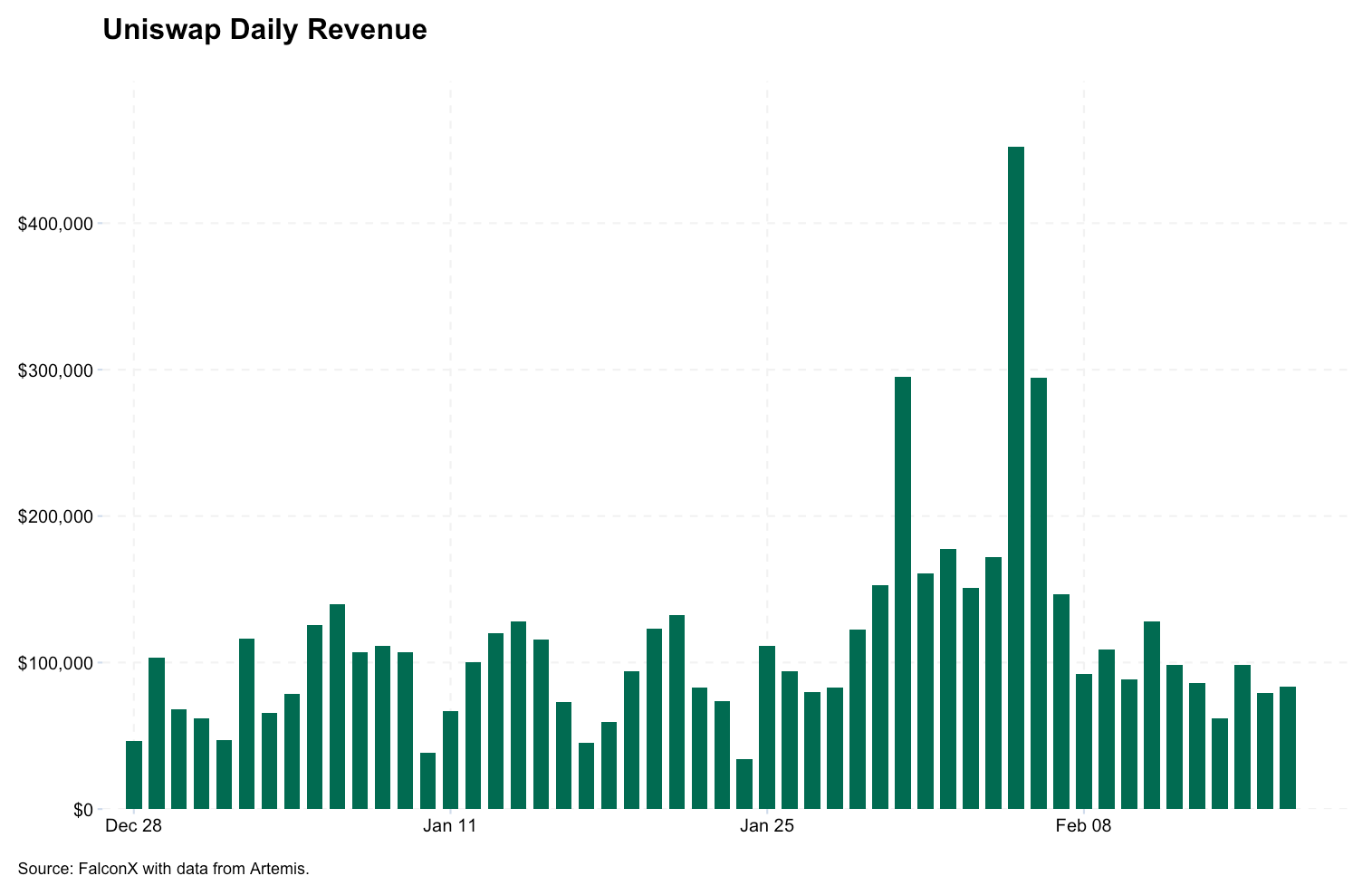

Leading crypto projects are moving to align interests with their token holders, in part on a more favorable regulatory environment in the U.S. Moreover, there seems to be a desire to streamline operations ahead of potential TradFi competition on their turf that further regulatory progress might enable. These actions are unlocking greater revenue opportunities for DAOs, helping align new products with token holders and enabling new features such as fee switches. So far, Uniswap and Aave, two of the largest DeFi projects, have made progress towards these new structures. UNI has consequently turned on its fee switch, driving value back to tokenholders through a buy and burn, currently annualizing at $33M of protocol revenue as of February 17, 2026, per data from Artemis.

When considering what other crypto projects could be candidates for similar moves, crypto investors may want to be cognizant of the potentially high costs involved in what is essentially a reorganization of the capital structure (labs entities may demand payment or tokens to cede revenue claims). For example, Uniswap Labs requested 20M UNI tokens ($140M at the time) in its Unification proposal, while Aave Labs requested $42.5M in stablecoins and roughly $8M in AAVE tokens to align interests going forward. So while these changes could set up these protocols for greater long term success, there could be some near-term headwinds from related token overhangs and cost concerns.

Looking Ahead: Market Structure Bill and Quantum to Set Tone

The U.S. Crypto Market Structure bill will likely dictate sentiment in the coming weeks and is shaping up as one of the major potential market drivers in the Year of the Horse. Crypto and banking groups continue to meet with the White House to hash out a deal. If progress fails to materialize, crypto could see a longer term overhang from uncertain future regulation, especially as the midterms approach and prediction markets show increased odds of Democrats winning.

On a positive note, the crypto industry is taking steps to proactively address the looming quantum threat which has recently weighed on sentiment, as investors begin to consider the threat more seriously. In the past few weeks, Strategy, amongst the largest BTC holders, announced a quantum security program, coordinating with the ‘global cyber, crypto, and bitcoin security community’ to help with Bitcoin’s quantum transition. Coinbase also established a quantum computing and blockchain working group, which will help issue recommendations for industry participants to protect against quantum risks and provide analysis on quantum breakthroughs. Concurrently, several startups are working on developing post-quantum technology for blockchains, such as Project Eleven and BTQ Technologies. These developments indicate the crypto community is proactively working towards solutions and should help alleviate near-term concerns. Any concrete solutions that emerge from these groups could flip the narrative back in favor of BTC.

1 Crypto ETFs analyzed include ETFs from 21Shares, which is a subsidiary of FalconX.

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd., nor Banzai Pipeline Limited service retail counterparties, and the information on this website is NOT intended for retail investors. The material published on this website is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this website is not and should not be regarded as investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

No discussion of a particular company or product shall be considered an endorsement of such company or product. Past performance is not indicative of future results. FalconX, and its affiliated parties may hold positions in assets discussed, which may change without notice. Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory, and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over-the-counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a swap dealer with the U.S. Commodities Futures Trading Commission (CFTC) and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is a registered Class 3 VFA service provider with the Malta Financial Services Authority under the Virtual Financial Assets Act of 2018. FalconX Limited is licensed to provide the following services to Experienced Investors, Execution of orders on behalf of other persons, Custodian or Nominee Services, and Dealing on own account. FalconX’s complaint policy can be accessed by sending a request to complaints@falconx.io

"FalconX" is a marketing name for FalconX Limited and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.