What ETH's Relative Liquidity Dynamics Tell Us About the Potential Price Impact of Initial ETF Flows

However, consensus already expecting bearish initial flows and ETH’s relatively strong current liquidity trends can mean that this potential underperformance could be short lived or relatively muted, resulting in a buy opportunity for those with a longer time frame.

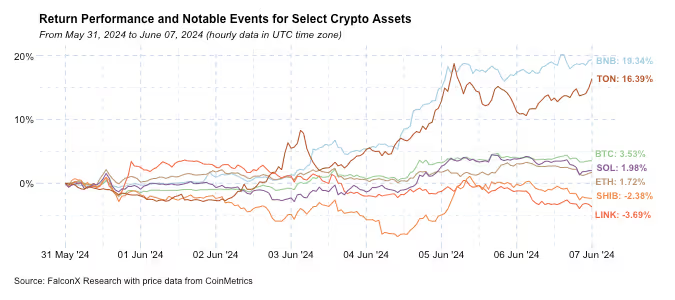

Crypto continues to grind higher on the back of a supportive macroeconomic environment. Both majors and SOL recorded positive returns over the past seven days, but those remain supported by relatively weak volumes. Spot volumes in BTC, ETH, and SOL so far in June have been 40-45% lower than March levels.

Among alts, BNB and TON were the two best performers within assets with a circulating market cap of over $10 billion. On the other hand LINK, correcting from a relatively good performance over the past 30 days, and SHIB, which has been out of favor among memecoins, were the laggards over the past week.

As of last Friday, all spot ETH ETF issuers submitted their S1 forms (or S3 form in the case of Grayscale) to the SEC for what will likely be the last couple of rounds of reviews before these ETFs can launch. This final approval process is expected to take from a couple of weeks to a couple of months at the very most.

The following key theme is how initial inflows will look like and what this could mean for ETH's price performance.

The consensus expectation is that initial inflows will be an adverse price action event. While gross inflows are expected to be 15-25% of BTC’s, there is a significant potential initial overhang from Grayscale’s ETHE, similar to what happened with GBTC and BTC.

This is likely a critical factor currently capping the ETH/BTC ratio at the 0.055 level. It represents a substantial recovery from the recent three-year lows but is still timid versus its historical record.

There are many moving parts that will impact how ETH’s price action will behave in the first couple of weeks after its spot ETF launches, but liquidity trends suggest that the current bearishness could be somewhat overstated.

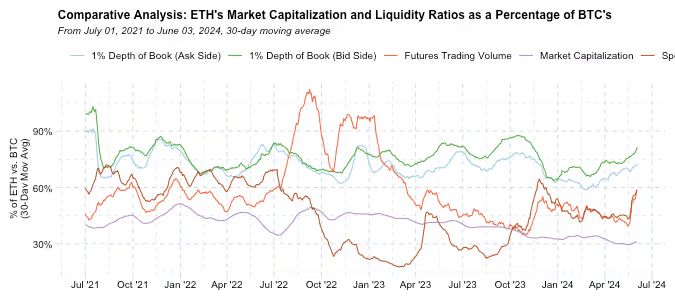

The chart below shows the relative size of ETH versus BTC according to different metrics. The purple line indicates the market cap ratio, which is the one most are familiar with and indicate that ETH is about one third of BTC.

Things get more interesting when we look at liquidity metrics, which suggest that ETH punches above its weight than some would initially guess. The orange and brown lines indicate futures and spot trading liquidity, respectively, which are currently running at 50-60% of BTC’s turnover. The green and blue lines at the top indicate 1% depth of book (bid and ask sides respectively) in spot markets, which is a surprising 70-85% of BTC’s.

ETHE currently has an AUM of $11.1 billion, which represents 39% of GBTC’s AUM at the launch of BTC spot ETFs on January 11. Over the first two weeks, GBTC faced outflows of $5.6, or almost 20% of its AUM at launch ($28.5 billion). If ETHE follows the same pattern, it would face $2.2 billion of outflows in the first couple of weeks after launch.

This would be a significant outflow volume that could weigh on ETH’s short-term price performance. However, consensus already expecting bearish initial flows and ETH’s relatively strong current liquidity trends can mean that this potential underperformance could be short lived or relatively muted, resulting in a buy opportunity for those with a longer time frame.

Regardless of the short-term reaction, however, it’s important not to understate the impact of the ETH ETF spot launch over the medium to long terms.

For ETH itself, the recognition of its commodity status and the unveiling of crypto use cases beyond digital gold among mainstream investors could continue to fuel its performance catch-up over the next many quarters. For the industry more broadly, the policy and regulatory shift that is contextualizing the approval is one of the most important market tailwinds, a perception that still seems underappreciated in beyond crypto specialist circles.

Other Trends We're Watching

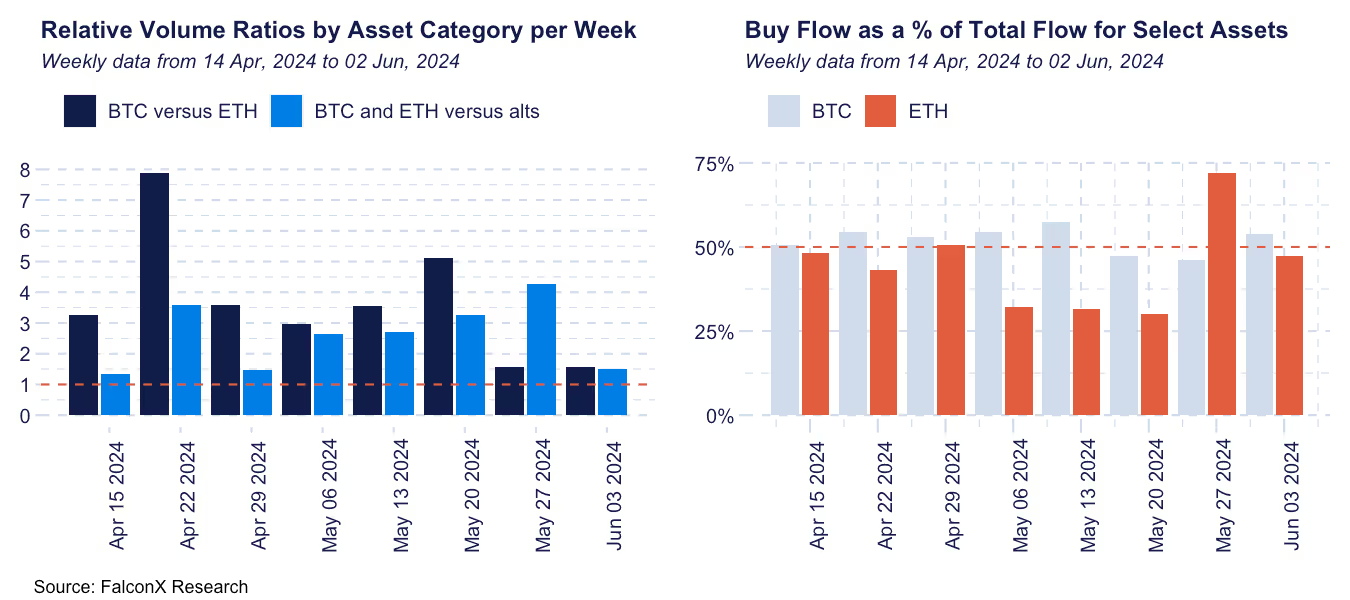

FalconX Trading Desk Color: Most investor personas have been better buyers at our desks. Retail aggregators were one of the main exceptions with net seller flow in majors and alts. BTC continues to dominate our activity, but activity in ETH has also been increasing relative to alts after the spot ETF approval. ETH’s buy/sell ratio shrunk compared to the past week but are still significantly above what it was in May, while BTC’s buy/sell ratio remained around 1x. Alts activity remains concentrated in relatively few names, with SOL, DOGE, and AVAX attracting bullish interest.

Token Unlocks Calendar Heats Up in the Coming Month: Recent data from TokenUnlocks highlight a series of notable upcoming releases, including APT (2.6% of circulating supply on June 12), STRK (4.92%, June 15), ARB (3.2%, June 16), OP (2.9%, June 30), SUI (July 1), and WLD (9.7% in the next seven days). These tokens are among the assets we recently identified as having the highest USD values of non-circulating supply.

The potential for a sustained supportive market environment could help soften the impact of these new supplies. However, it remains essential to monitor these events closely, especially considering that the recent positive returns have not widely spread to altcoins and are supported by relatively low trading volumes.

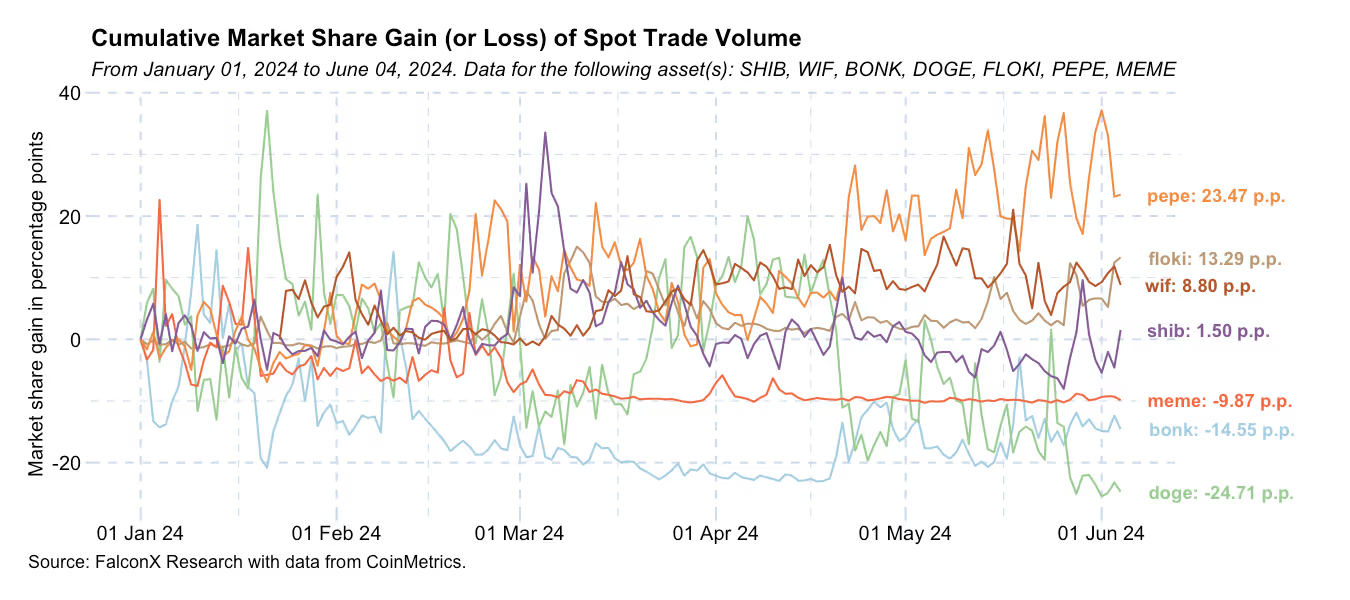

Memecoin Spot Trade Volumes in Centralized Exchanges Fall to the Lowest Values Since March: During the most recent memecoin frenzy in March, the top memecoins (DOGE, SHIB, WIF, PEPE, FLOKI, and MEME) traded an incredible $5.8 billion per day on average in spot markets, as we highlighted months ago. This liquidity metric shrunk to $2.7-2.8 billion in April and March, falling further to under $2.0 billion in June.

The drop hasn’t been uniform, however. PEPE, FLOKI, and WIF gained substantial spot volume market share from DOGE, BONK, and MEME. The chart below shows these cumulative changes throughout this year.

The 68% reduction in memecoin trading volume in June, compared to the average seen in March, underscores a broader trend of declining spot volumes across the market. However, during the same timeframe, this decrease is notably steeper than the 58% drop observed in the trading turnover of major cryptocurrencies, BTC and ETH. The significant shifts in market share further support may indicate a pivot by investors towards emerging names in the space, possibly in search of novel opportunities.

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd. nor Banzai Pipeline Limited service retail counterparties, and the information in this material is NOT intended for retail investors. This material is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this material is not and should not be regarded as investment advice, investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over the counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a Swap Dealer with the U.S. Commodities Futures Trading Commission and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is licensed by the MFSA as a Class 2 Crypto-Asset Service Provider (Regulation (EU) 2023/1114). It is also licensed as a Financial Institution (Cap. 376) exclusively for EMT payment services.

"FalconX" is a marketing name for the FalconX Group and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.