Velocity of Value: The Ascent of Tokenized Stocks

New integrations and growing demand for 24/7 trading are fueling a boom in tokenized stocks.

FalconX is not a registered broker-dealer with the U.S. Securities and Exchange Commission (SEC) or a member of the Financial Industry Regulatory Authority (FINRA). Further, FalconX is only able to offer tokenized stocks or equities from and to all jurisdictions in accordance with applicable law, regulation and licensing restrictions. Investing in digital assets or tokenized equities involves a substantial degree of risk. Market prices can be highly volatile and unpredictable. Movements in the market can result in significant, rapid, and potentially total loss of your invested capital. Before allocating capital, you should carefully evaluate whether such investments align with your financial situation, experience, and risk tolerance. For further information regarding potential risks, please refer to the disclaimer below.

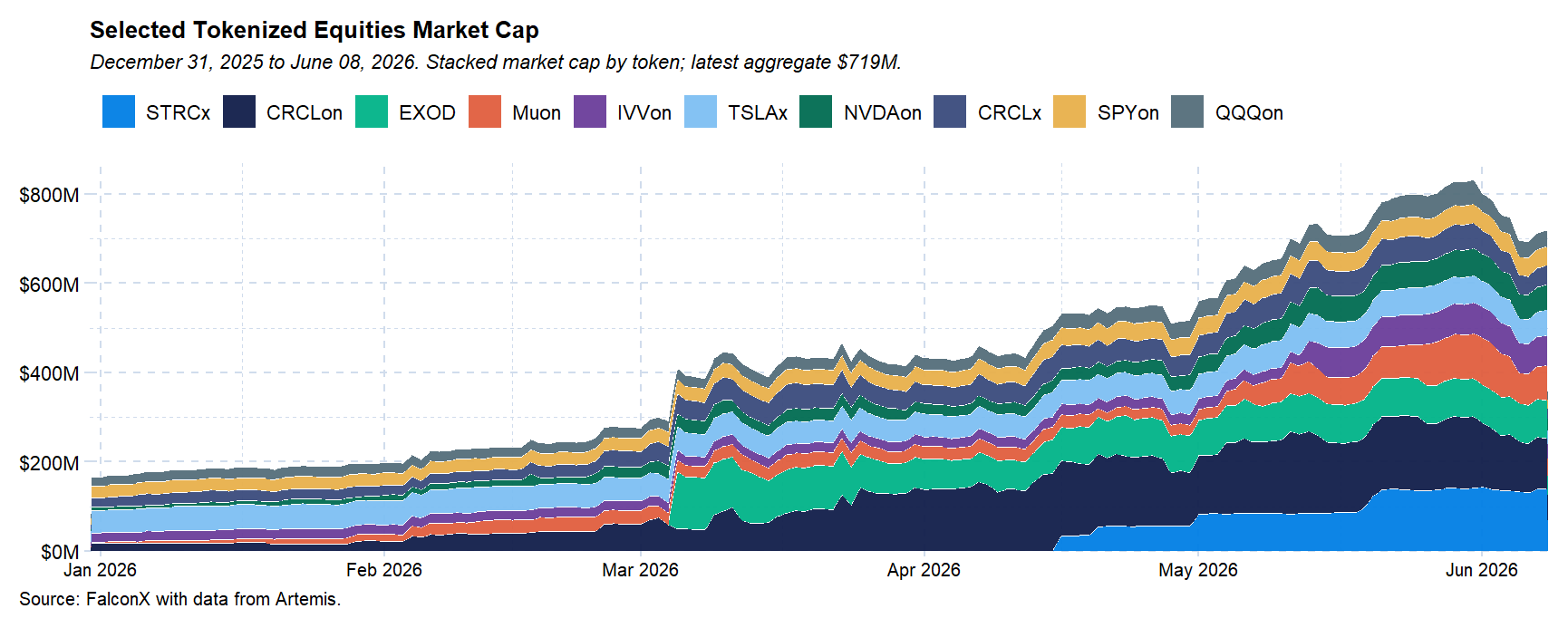

The global market cap of tokenized stocks has grown nearly 5x since 2025 to $1.5B as of June 9, 2026, according to data from RWA.xyz. The total value of these instruments has climbed 2x YTD alone. Key benefits of tokenized stocks include fractional ownership, near-instant settlement, the potential for 24/7 trading, and use in DeFi. A confluence of factors is powering the boom: more platform integrations, growing on-chain utility, and rising demand for 24/7 access to financial instruments.

The Drivers Behind the Traction

Platform Integrations. Some of the largest centralized exchanges have moved to offer tokenized stocks. Kraken began offering these in 2025, with Bybit and OKX following suit. Most recently, Binance rolled out its tokenized stock offering (bStocks) in June 2026, while Coinbase stated plans to offer tokenized stocks soon.

Global Access and On-chain Utility. Traders are beginning to demand 24/7 trading of traditional asset classes, as evidenced by growth in related markets, such as Hyperliquid’s HIP-3. This is spilling into tokenized stocks and a small but growing DeFi ecosystem is growing around them. Tokenized stocks enable traders to quickly and permissionlessly get economic exposure to equities while staying on-chain. Additionally, tokenized stocks may provide exposure to US stocks for traders in jurisdictions where accessing US stocks may be difficult or costly.

The Issuers Behind the Activity

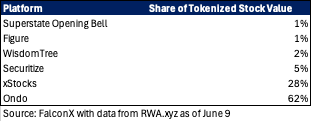

Ondo and xStocks alone are behind nearly $1.3B of the $1.5B of total tokenized stock value outstanding, with Ondo’s tokenized stocks valued at $0.9B while xStocks totaled $0.4B, per data from RWA.xyz as of June 9, 2026. Ondo has 231 individual stocks issued, while xStocks has 163. Other issuers with meaningful market share include Securitize, WisdomTree, Figure, and Superstate.

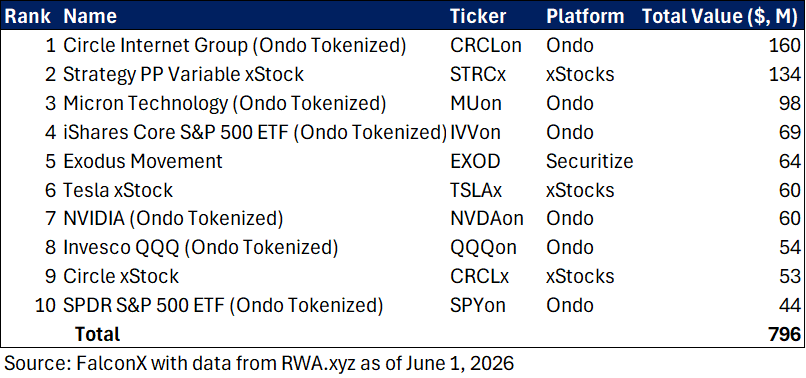

The top 10 tokenized stocks by value as of June 1, according to RWA.xyz, are as follows. These include a mix of crypto-specific names (Circle, Exodus, Strategy’s STRC), indices (S&P 500), and tech stocks (Micron, Tesla), indicating the kind of instruments driving demand. Together, the largest 10 instruments make up over $700M of value, nearly half of all tokenized stock value today, suggesting these instruments are relatively concentrated at this point.

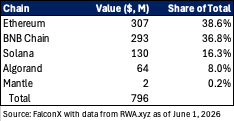

Most of these tokenized stocks are issued on several chains; they are not limited to just one, improving distribution and access. ETH and BNB dominate as blockchains with the most tokenized stock value, while Solana sees the third most aggregate value of the set. Of this group, the Tesla xStock has the most holders (~30K), while the rest largely have a few thousand holders, indicating the current reach of these assets.

Considering the dominating presence of Ondo and xStocks in the top 10 tokenized stocks set, we dive deeper into those names.

Ondo (ONDO)

Ondo Finance is an RWA issuer whose offerings span a tokenized stock and ETF platform, an L1 blockchain geared for RWAs (Ondo Chain), as well as the yieldcoin USDY ($2.1B MC) and tokenized US treasury vehicle OUSG ($500M TVL). Its Global Markets platform brings public securities on-chain as tokenized stocks, which can be freely transferable and usable in DeFi. It notes its stock offerings are not available in the US.

Ondo tokenized stocks are designed to give holders the same economic exposure as they would receive if they owned the underlying asset and invested the dividend back into the stock. Its tokens are designated by the on (Ondo/on-chain) suffix. Ondo tokenized stocks are fully backed with the underlying asset, with all Ondo Global Markets holdings held with one or more US-registered custodial broker-dealers. However, given they reinvest dividends, a certain token may provide economic exposure to more than one share. Therefore, the token price may become more than that of the underlying stock. These tokens are essentially ‘total return tracker tokens’, with no voting rights. Given the ownership structures involved as well as secondary market liquidity, the price of such tokenized stocks may differ from the underlying.

Ondo tokenized stocks generally trade 24/5 on its platform. It has an instant mint and burn, with no mint or burn fees. This helps arbitrageurs align tokenized stock prices to their off-chain prices. Holders can redeem the tokens for cash or stablecoins. To buy or sell directly from the platform, users must successfully complete KYC.

Ondo’s platform leverages a request for quote (RFQ) system. A user requests a quote for a trade, and Ondo provides a firm quote for approximately 30 seconds based on real stock market liquidity and conditions, allowing it to pass through the same liquidity and depth from the underlying stock markets. The user can then apply the quote to the minting/redemption smart contract to create or redeem the Ondo GM tokens for stablecoins (USDon). Because Ondo takes around 30 seconds of price risk, it adds a small volatility buffer to its quoted price.

Regarding trading and liquidity mechanics, Ondo stated its platform achieves spreads in line with brokerages (up to 5 bps). According to the Ondo team, secondary market trading for Ondo tokenized stocks often routes through intents platforms, enabling solvers to mint/redeem on Ondo’s primary market so they can provide liquidity to users without having to take inventory risk or have capital tied up. This is the primary difference vs xStocks, where the secondary market trading primarily occurs through DEXes. However, minting/redeeming on the primary market is only available 24/5 at this point.

As far as investor protections, Ondo leverages a bankruptcy-remote legal structure using a SPV with at least one independent director, full asset backing with overcollateralization, first-priority security interest held by a third-party security agent, daily attestations of assets held at regulated US entities, reporting via daily updates, monthly reconciliation, and annual audits. Ankura Trust Company serves as the Verification Agent and Security Agent for Global Markets.

Ondo also launched 24/7 RWA perps on June 9, 2026, where its tokenized stocks are usable as collateral.

xStocks

xStocks is a tokenized stock framework developed by Backed Finance. The legal issuer of xStocks is Backed Assets (JE) Limited, a private company incorporated in Jersey. In December 2025, Kraken announced it agreed to acquire Backed Finance.

xStocks are fully backed by the underlying asset held with a regulated custodian. Issuance and redemption through the issuer operate 24/5. Corporate actions such as dividends, stock splits, and reverse splits are reflected through an on-chain rebasing mechanism. Token balances always reflect a 1:1 exposure of the underlying equity. As rebasing can add friction to on-chain composability, xStocks leverage Solana Token Extensions (Scaled UI), which allows the issuer to provide a multiplier that is used to represent on-chain corporate actions like stock dividends.

xStocks were initially launched on Solana, before expanding cross-chain. Today, they largely live across Solana, BNB Chain, and Ethereum.

xStocks’ structure includes a bankruptcy-remote issuing SPV, full 1:1 collateralization on an asset-by-asset basis with no commingling between products, segregated custody accounts governed by a three-party Account Control Agreement, an independent Security Agent with visibility over collateral, publicly verifiable proof of reserves, and audited smart contracts.

xStocks have 2 layers: a primary issuance layer where tokens are issued or redeemed, and a secondary permissionless layer where tokens move freely across exchanges, wallets, and DeFi protocols. Access to the primary market requires onboarding (KYC/AML). Issuance and redemption can be done with either stablecoins or with the underlying equity through its In-Kind flow (xPort). Primary issuance and redemption operate 24/5, while secondary trading can occur 24/7, such as on DeFi or crypto exchanges.

Each xStock provides economic exposure to a specific underlying equity; it does not confer shareholder voting rights. An xStock is a tracker certificate. These provide economic exposure to the underlying equity but do not convey shareholder rights, such as voting rights.

Collateral is held in segregated accounts under a three-party structure involving the issuer, custodians, and an independent security agent. In the event of issuer default, the security agent may assume control of the collateral accounts and distribute proceeds to token holders in accordance with the prospectus terms.

Exchanges As a Distribution Layer

One important distribution channel for these products is centralized exchanges. While some of these crypto venues have moved to offer real stock trading, many also offer access to tokenized stocks such as xStocks (Kraken, Bybit), Ondo (OKX), and Binance (bStocks). Coinbase does not offer tokenized stock trading as of writing, but has stated plans to offer such products in the future. These platforms stand to play a key role as on/off ramps to tokenized stock products and could help funnel users on-chain with such assets.

Kraken was a first mover in this area with the launch of xStocks support in June 2025 for non-US clients. These trade on Kraken 24/5 and can be withdrawn to self-custodial wallets for 24/7 flexibility to use xStocks on-chain in DeFi. Kraken launched tokenized equity perps in Feb 2026.

In March 2026, Kraken announced a partnership with Nasdaq to build a gateway that connects tokenized equity capital markets with decentralized blockchain networks, combining Nasdaq’s regulated market infrastructure with Kraken’s xStocks framework. At that point, it said xStocks had surpassed $25B in total transaction volume since launching, with $4B+ settled on-chain and 85K+ unique holders across networks. Nasdaq’s equity token design is expected to become operational in 1H27 and is described as preserving issuer control, existing regulatory frameworks, and the underlying rights of company shares.

Assessing On-chain Activity of Ondo and xStocks

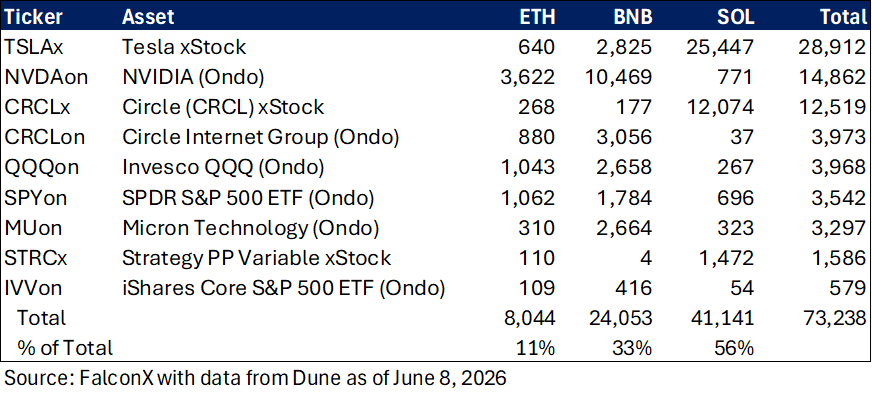

To determine how these instruments live on-chain, we examined the set of the largest 10 tokenized stocks by value, outlined earlier, leveraging data from Dune and DEX Screener. We limited our analysis to Ethereum, BNB Chain, and Solana, due to tooling accessibility (drops EXOD as it is on Algorand), leaving us with 9 tokenized stocks to examine.

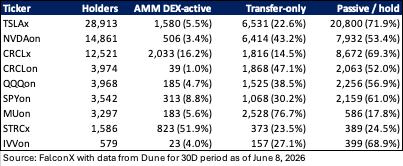

For the set, we calculated approximately 73K combined on-chain holders of these assets. Of these holders, over the last 30D period as of June 8, 2026, 7.8% are DEX-active with the tokenized instrument (traded it on an AMM DEX), 30.3% are transfer-only (sent it to another address), and 61.9% are passive (hold only).

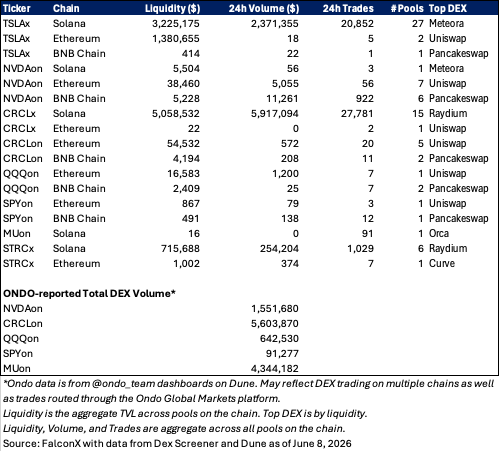

AMM DEX trading for the cohort was concentrated in xStocks on Solana: CRCLx ($5.9M/24H volume as of June 8), Tesla xStock ($2.4M), NVIDIA xStock ($1.9M) and SP500 xStock ($1.8M). In contrast, Ondo tokens trade mainly on centralized exchanges/Ondo Global Markets and see relatively thinner AMM DEX pools and volumes, at least for the DEXes monitored by DEX Screener.

Holder Counts Across Chains

We find that of the set of the largest tokenized stocks by value, xStocks have the most holders, with approximately 43K or 59% of the set, with most of these (29K) in the Tesla xStock (TSLAx), followed by CRCLx and STRCx. Ondo tokenized stocks had around 30K holders in the set, mostly in NVDAon (15K), followed by CRCLon (4k) and QQQon (4K).

By blockchain network, Solana had the majority of holders (56% of the set), largely driven by xStocks. BNB Chain had the 2nd most holders (33%), followed by ETH (11%). Given xStocks is Solana-native, these findings make sense and could be reflective of adoption by retail users through Kraken and other centralized exchanges. However, the results could also reflect user preferences or exchange/wallet integrations that skew to low cost blockchains.

AMM DEX Activity by Asset & Chain

We found that most of the tokenized stocks in the set had a low share of holders trading the tokens on AMM DEXes, but their relative DEX activity was far greater when compared to certain crypto-native DeFi tokens.

xStocks had a much larger presence on AMM DEXes than Ondo tokenized stocks, especially on Solana. The asset with the most on-chain liquidity (aggregate pool TVL) and trading volume was CRCLx on Solana with $5M liquidity and 24H volume of nearly $6M. Activity for the xStocks shown in the below figure was heavily concentrated in Solana. ETH and BNB had negligible activity, in contrast, which may be explained by incentives specific to protocols on Solana. The relatively greater xStocks activity on AMM DEXes may also be due to a significant portion of Ondo assets trading on centralized exchanges and through its Ondo Global Markets platform, which DEX Screener does not capture. There may be a chicken and egg problem when bootstrapping a new ecosystem; holders may see no reason to LP on DEXes if volumes are perceived to be low. Another consideration is execution; traders may prefer to access tokenized stocks on primary markets if AMM liquidity is too thin to support larger sizes without significant slippage.

While Ondo instruments showed relatively low AMM DEX activity per data from DEX Screener, the Ondo-reported DEX volumes were markedly higher, with CRCLon ($5.6M), MUon ($4.3M), and NVDAon ($1.6M) posting multi-million dollar daily volumes, in line with some of the largest xStocks. The step up in volumes may reflect DEX/wallet trading that is routed through intents where solvers tap into primary market liquidity on Ondo Global Markets, rather than source directly from AMMs.

Holder Behavior

Examining on-chain activity shows that for the most part, the majority of the holders of these assets in the set are passive. Generally, only a small share of holders transferred the tokens between addresses, and even less traded the asset on an AMM DEX over a 30D period. For instance, the largest xStocks by holder count (TSLAx) saw only 5% of holders trade the instrument on a DEX in the period.

While such headline numbers may seem small, this kind of DEX participation among holders appears significantly higher relative to some crypto-native tokens. For example, our analysis of MORPHO holders across Ethereum and Base saw around 1K DEX-active holders across nearly 148K holders (0.7%). Of course, a much larger holder base could be at play here. On the Solana side, for example, JTO saw 2% of its 78K holderbase trade the token on DEXes over the period.

For the tokenized stock set, the instrument with the most active DeFi holders was STRCx, where roughly 52% of its holders traded it on an AMM DEX over the 30D period, which may be supported by recent developments in MSTR and the proliferation of STRC-related TVL across DeFi yield and lending protocols. CRCLx was the second most AMM DEX-active asset (16% of holders). Interestingly, Solana xStocks (TSLAx, CRCLx) carry almost all AMM DEX trading in this set, yet only 5-16% of their holders traded these assets on an AMM DEX in the 30D period. Ondo EVM tokens (NVDAon, CRCLon, QQQon, SPYon, MUon) were dominated by transfer-only + passive holders and have <10% AMM-active holders, supporting the case that much of Ondo DEX trading is not happening on AMMs, but is instead routed through intent-based solvers that interact with the Ondo Global Markets platform.

Takeaways

While tokenized stock value is growing rapidly, in part due to broader platform support and integrations, the DEX presence of tokenized equities remains nascent. Part of this may reflect the venues where many users are acquiring these assets (on a CEX, which by nature encourages users to hold balances there to trade), while incentives may not be meaningful enough to participate in DeFi with these assets. Relatively low DEX liquidity and volumes are telling, while only some lending markets, such as Kamino, support tokenized equities as collateral. However, initial DeFi traction relative to certain crypto tokens suggests there is demand from holders to use these on-chain. As these instruments continue to grow, their on-chain presence stands to expand as further use cases spring up for these instruments.

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd., nor Banzai Pipeline Limited service retail counterparties, and the information on this website is NOT intended for retail investors. The material published on this website is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this website is not and should not be regarded as investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

No discussion of a particular company or product shall be considered an endorsement of such company or product. Past performance is not indicative of future results. FalconX, and its affiliated parties, including 21shares, may hold positions in, act as a market maker for, or otherwise have a financial interest in, assets discussed herein, and may benefit from any price movements or transactions involving the subject company. This may change without notice. Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory, and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over-the-counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a swap dealer with the U.S. Commodities Futures Trading Commission (CFTC) and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is a registered Class 3 VFA service provider with the Malta Financial Services Authority under the Virtual Financial Assets Act of 2018. FalconX Limited is licensed to provide the following services, Execution of orders on behalf of other persons, Custodian or Nominee Services, Transfer services, and Dealing on own account. FalconX’s complaint policy can be accessed by sending a request to complaints@falconx.io

"FalconX" is a marketing name for FalconX Limited and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.