Unpacking the January 31 Liquidation Cascade

BTC tapped $75K over the weekend, with the move appearing to be driven by perpetual futures liquidations rather than specific headlines. $2.5B liquidations occurred across the day, per data from Coinglass, reported to be crypto’s 10th largest liquidation day ever. Perps DEX Hyperliquid led venues in liquidations, with over $1B in 24H liquidations, notable considering CEXes still dominate in terms of volumes and open interest.

Recap

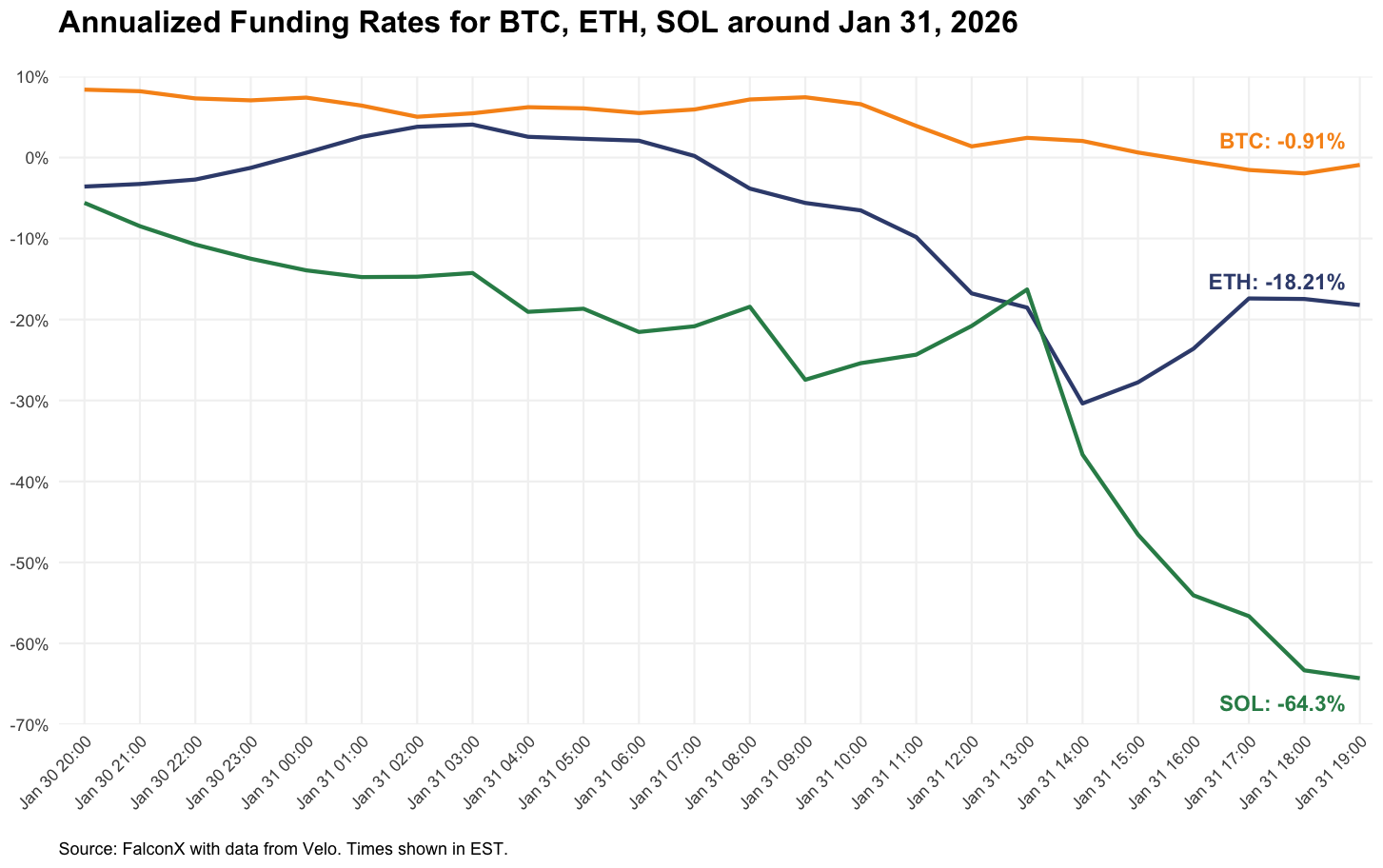

As BTC traded down to $81K around 9:30am ET on January 31, sparking some long liquidations, open interest increased markedly as traders added to shorts, driving funding meaningfully lower. Two further waves of liquidations occurred as BTC broke under $80K, culminating with a wick down to $75K around 1:40pm ET, ultimately stabilizing around the $78K area later in the day.

While BTC funding was still positive (2% annualized, longs paying shorts), ETH and SOL funding flipped meaningfully negative (-30% and -35% annualized at 2:30pm ET). By evening, BTC funding turned negative.

BTC fell under Strategy’s cost basis of $76K, breaching a closely watched level. While more symbolic than an immediate concern, it adds to growing unease that the market may be closer to losing key sources of inflows (in January 2026, Strategy announced purchases of $4.7B of BTC). MSTR does not have debt due until 2028 and maintains a $2.2B reserve to help cover preferred stock dividends and debt servicing costs of approximately $800M annually, giving it a runway of at least 2 years.

The market was already on edge leading up to the move as Kevin Warsh emerged as Trump’s pick for Fed chair, driving a sell-off across equities and crypto given his relatively hawkish views. Precious metals had also collapsed Friday, with gold falling under $5K, as much as 9%, while silver saw its largest ever intra-day decline (36%). Moreover, it followed headlines of potential US military activity in Iran over the weekend, ramping up geopolitical uncertainty while other markets were closed. The sell-off also coincided with month end, culminating with a decline of 11% for BTC in January. Selling had dominated in earlier sessions with BTC ETFs seeing $1.5B of net outflows in the week.

The technical set up is telling. In the back half of the month, BTC broke under its 50D moving average and has remained under it, building on a negative trend since breaking under its 200D moving average in early November. On Jan 31, its daily RSI flashed oversold for the first time since November 19 (BTC found a local bottom shortly after this instance), which may suggest further downside may be limited.

ETH, SOL

While BTC exhibited weakness, ETH and SOL saw a larger impact, falling over 15% before recovering. ETH saw its largest long liquidations since 10/10, wicking down to $2200, per data from Velo. SOL briefly fell under $100, tapping its tariff sell-off lows from April 2025, before noticeable spot buying helped drive a recovery.

ETH now stands below its 200W moving average, highlighting the severity of the sell-off. SOL funding rates continued to inflect negatively, with funding pushing to -64% towards the evening, suggesting futures traders were positioning for further downside. This was in stark contrast to ETH, whose funding rate improved to -18% over the same period.

DeFi and Alts

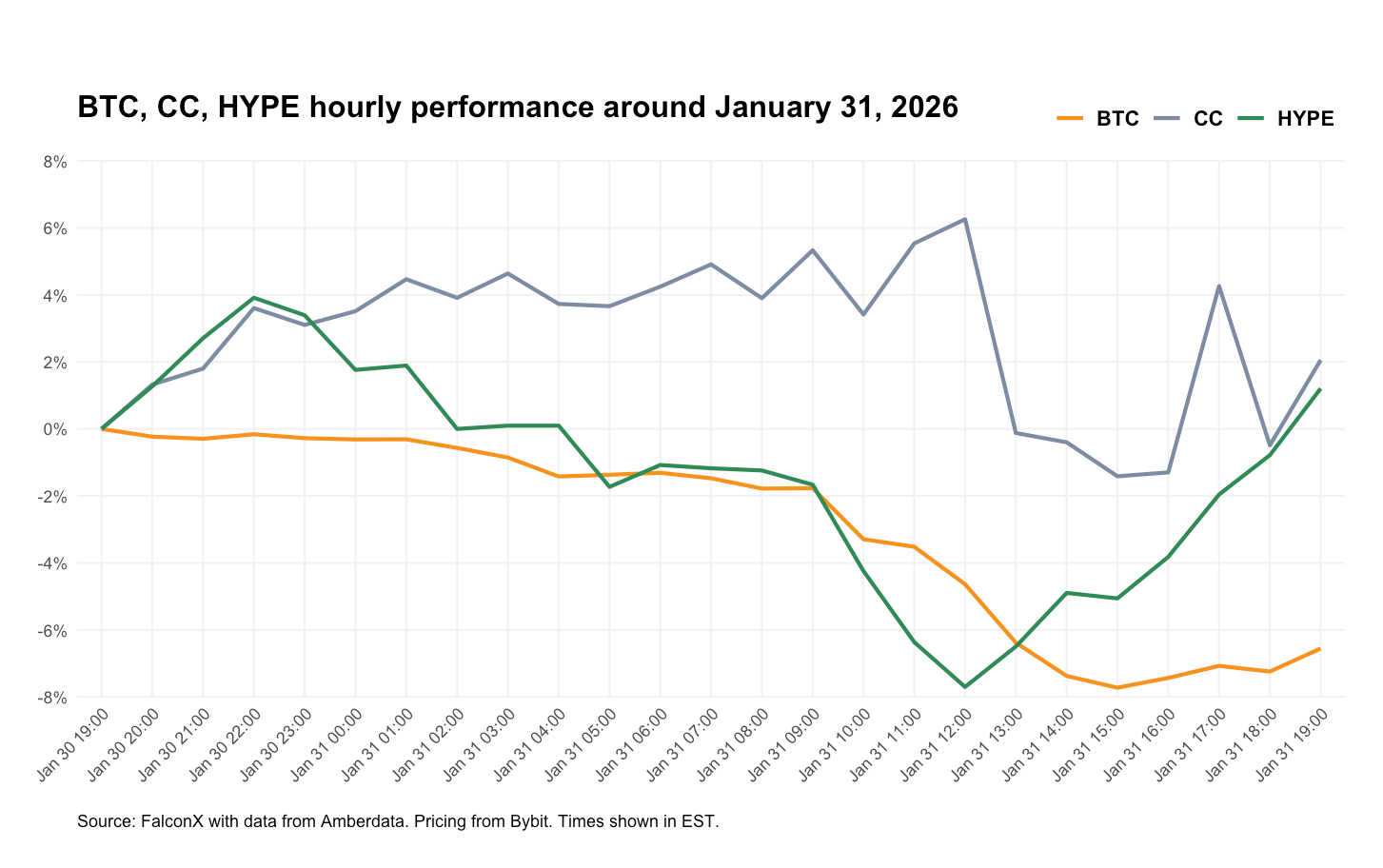

Notable outperformers over the period included HYPE and CC. After dropping with the rest of the market, HYPE bounced strongly and erased all losses, closing the day positive. The traction could be related to its handling of massive liquidations well throughout the day (HLP printed $15M+ from liquidations), and on recent tailwinds from its HIP-3 markets (record volumes). Specifically, Hyperliquid has seen strong activity in its commodity markets, with its silver market recently seeing $250M of open interest and 24H volume of $1.5B, per data from ASXN. Meanwhile, CC had been climbing over much of the sell-off, setting a new all-time high, and only started declining after most names had already fallen sharply. It remains topical as a play on tokenization, considering its partnerships with firms such as DTCC.

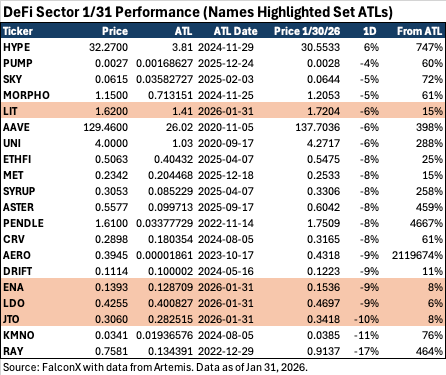

Across DeFi leaders, PUMP and MORPHO were relative outperformers, falling 5% on the day, while SOL-related names underperformed the set (RAY -17%, KMNO -11%). Several notched new all-time lows, including ENA and staking names LDO and JTO. The price action fails to reflect recent growth for some of these names; Ethena has seen its stablecoin supply grow YTD, per data from Artemis, while Lido’s AUM jumped to its highest since 2024 earlier in the month in ETH terms. Overall, buyback names held in the best.

Several crypto projects saw their token prices fall to critical levels. Spot DEX leader UNI fell under $4.00, dropping to levels around its launch price in 2020. Perp DEX LIT traded at a $1.4B FDV, under its last private valuation before its token launch ($1.5B).

Another piece of the broader market, considered more independent from crypto prices, is also starting to show some gaps: stablecoin market cap. After seeing rapid growth throughout 2025, stablecoin market cap has declined from a peak of $310B to $306B as of January 31, 2026, per Artemis.

February Outlook

Given Friday’s blow-off top in metals, traders may be anticipating a rotation back to crypto. While BTC had previously been seen as a beneficiary of strength in gold, capital that may have flowed to crypto off such moves instead funneled to silver in recent months. This could revert as silver cools off.

In the weeks forward, primary catalysts will include any developments on the crypto market structure bill, with key groups set to meet at the White House this week to discuss the bill.

On a flows basis, investors are looking for industry support to stem selling. Last week, Binance announced it would convert its SAFU fund’s $1B of stablecoin reserves into BTC reserves within 30 days. Tether has also been a key buyer, with its Q4 attestation report showing it increased its BTC reserves by 11% in BTC terms from the prior quarter and could be a source of market stabilization.

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd., nor Banzai Pipeline Limited service retail counterparties, and the information on this website is NOT intended for retail investors. The material published on this website is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this website is not and should not be regarded as investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

No discussion of a particular company or product shall be considered an endorsement of such company or product. Past performance is not indicative of future results. FalconX, and its affiliated parties may hold positions in assets discussed, which may change without notice. Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory, and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over-the-counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered with the U.S. Commodities Futures Trading Commission (CFTC) as a swap dealer and a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is a registered Class 3 VFA service provider with the Malta Financial Services Authority under the Virtual Financial Assets Act of 2018. FalconX Limited is licensed to provide the following services to Experienced Investors, Execution of orders on behalf of other persons, Custodian or Nominee Services, and Dealing on own account. FalconX’s complaint policy can be accessed by sending a request to complaints@falconx.io

"FalconX" is a marketing name for FalconX Limited and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.