BTC Spot Buying Fades, ETH Scaling Drives Record Transactions, PUMP Activity Surges

January kicked off an explosive month for crypto as BTC rallied up to $97K, with data suggesting the move up was spot driven. Concurrently, ETH saw record wallet and transaction activity in part due to spam transactions enabled by the reduction in gas fees from its December Fusaka upgrade. Meanwhile, token launchpad PUMP saw a spike in activity the past few weeks, with tokens launched and PumpSwap volumes climbing to multi-month highs.

BTC

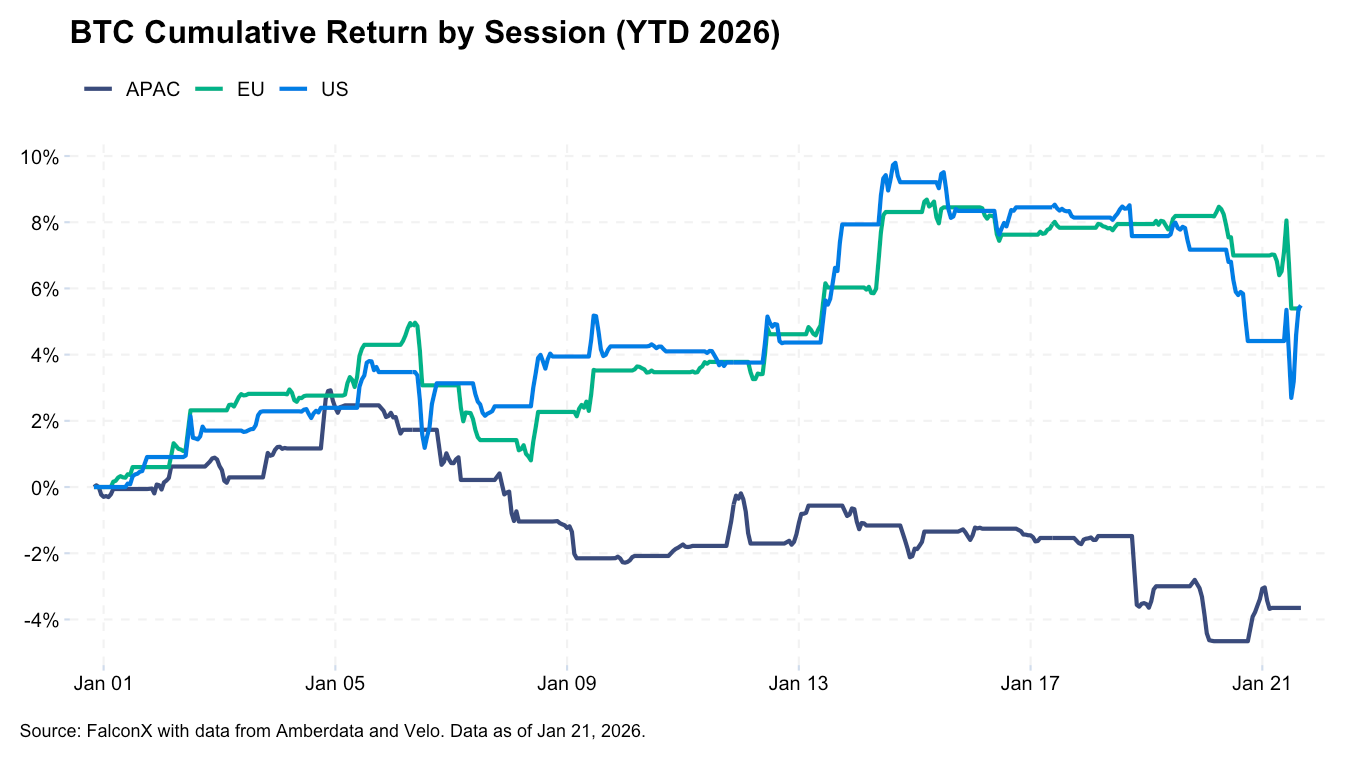

BTC saw a strong start to the month before paring back gains on macro headlines. Perps leverage did not move very strongly in the initial legs of the rally ($88K-$94K) the first week of January, suggesting this move was more spot driven, per CVD data on Velo. The second leg mid-month from $90-$97K saw stronger perp buying, especially on Binance.

Other data seems to support this including very strong ETF inflows during those two moves up. For example, January 13 and 14 printed $753M and $841M of inflows, respectively, some of the largest single day prints in months. Meanwhile, CME basis trended down over the period, per data from Velo, suggesting the move may not have been as driven by the basis trade as has been the case historically.

Across time zones, price action suggests buying began broad-based MTD, with the EU and US sessions leading buying early on, before the US session took the lead. This compared to the US and EU sessions as sellers in December, while APAC sessions were bidders. As the first rally this month sputtered out, the APAC session turned to sellers. In recent days, the US session has driven negative returns, likely as equities sold off.

Despite the more constructive set up, BTC is still struggling against a macro environment that has favored gold and other commodities. In Q4, the narrative was that BTC lagged gold due to long-time holders exiting and on deleveraging after the October 10th market crash. Now, it seems that a standstill in progress on the crypto market structure bill and renewed concerns over the quantum risk to BTC may be driving an overhang.

ETH

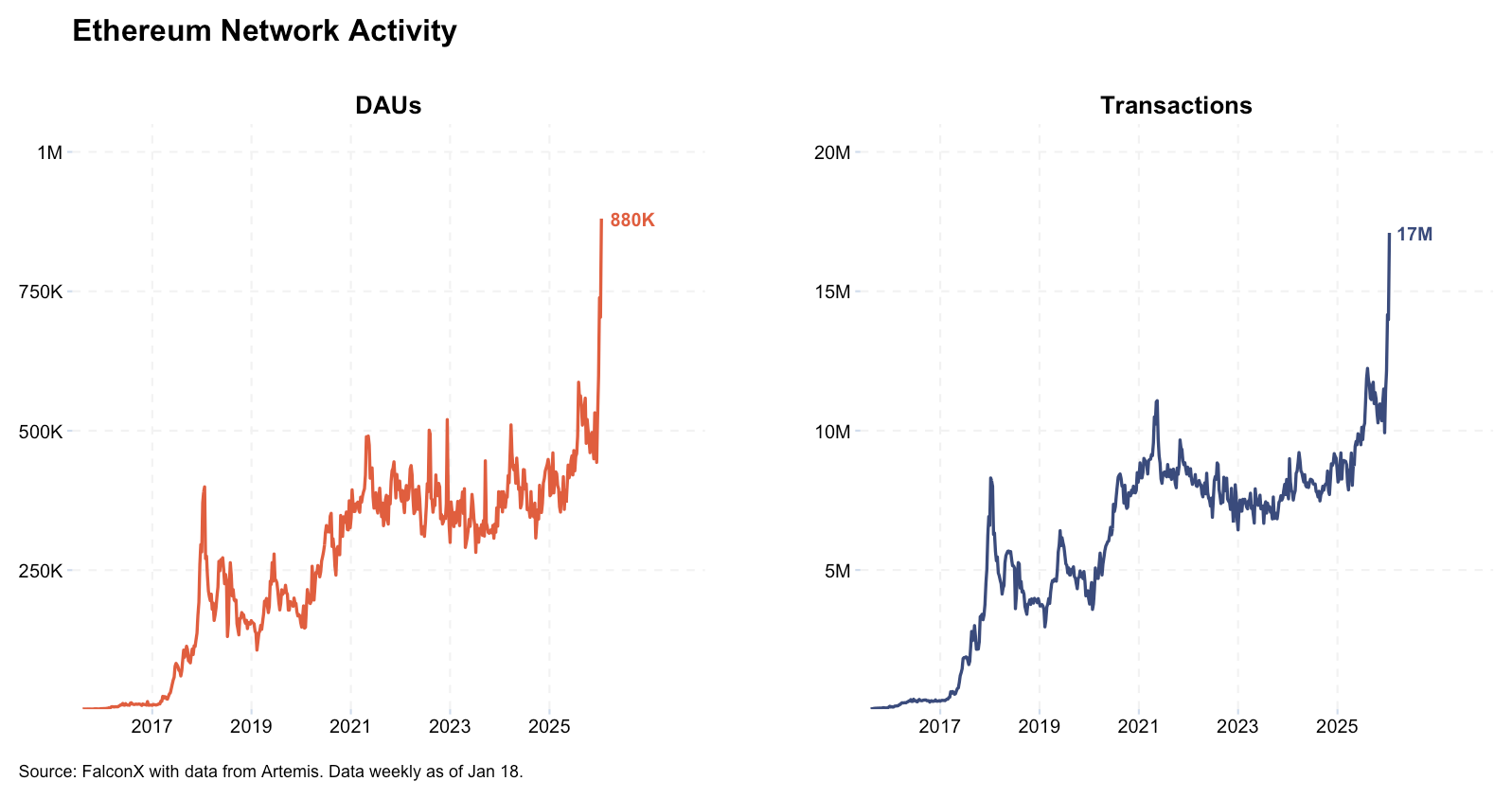

Ethereum DAUs and transactions are at all-time highs, jumping sharply since late December, per data from Artemis. This comes shortly after its Fusaka upgrade was implemented at the start of the month. The upgrade brought important scaling improvements, such as the gas limit being raised to 60 million gas, increased blob capacity, and data availability sampling.

Given few of the leading L2s are seeing all-time high DAUs or transactions as of late, it seems that the activity is largely confined to ETH L1. The activity has been linked to spam transactions, including address-poisoning activity. Average gas fees have declined by roughly 35% since before the upgrade, highlighting the scaling impact supporting the record transactions.

While having gas fees cheap enough to enable these kinds of transactions may not seem immediately fruitful, it demonstrates Ethereum is now competitive in cost with cutting edge blockchains that have encountered similar issues with spam transactions before. Assuming the cheaper fees will eventually help Ethereum drive activity for productive use cases over time, scaling at these levels and further should be a net positive for the protocol. In the long run, given Ethereum’s fee market, incremental demand for productive applications (DEX trading, etc.) stands to drive transaction fees up to a point that could price out spam transactions.

ETH is also seeing a record amount staked, with the ETH staking ratio climbing to over 30%. This was largely driven by Ethereum DAT Bitmine, which had staked 1.8M ($5.9B) as of January 19. Considering Bitmine still has another 2.4M of ETH, the sheer scale of incremental stake added could further drive ETH staking yields down for all participants, which stood at 3.17% as of January 21.

PUMP

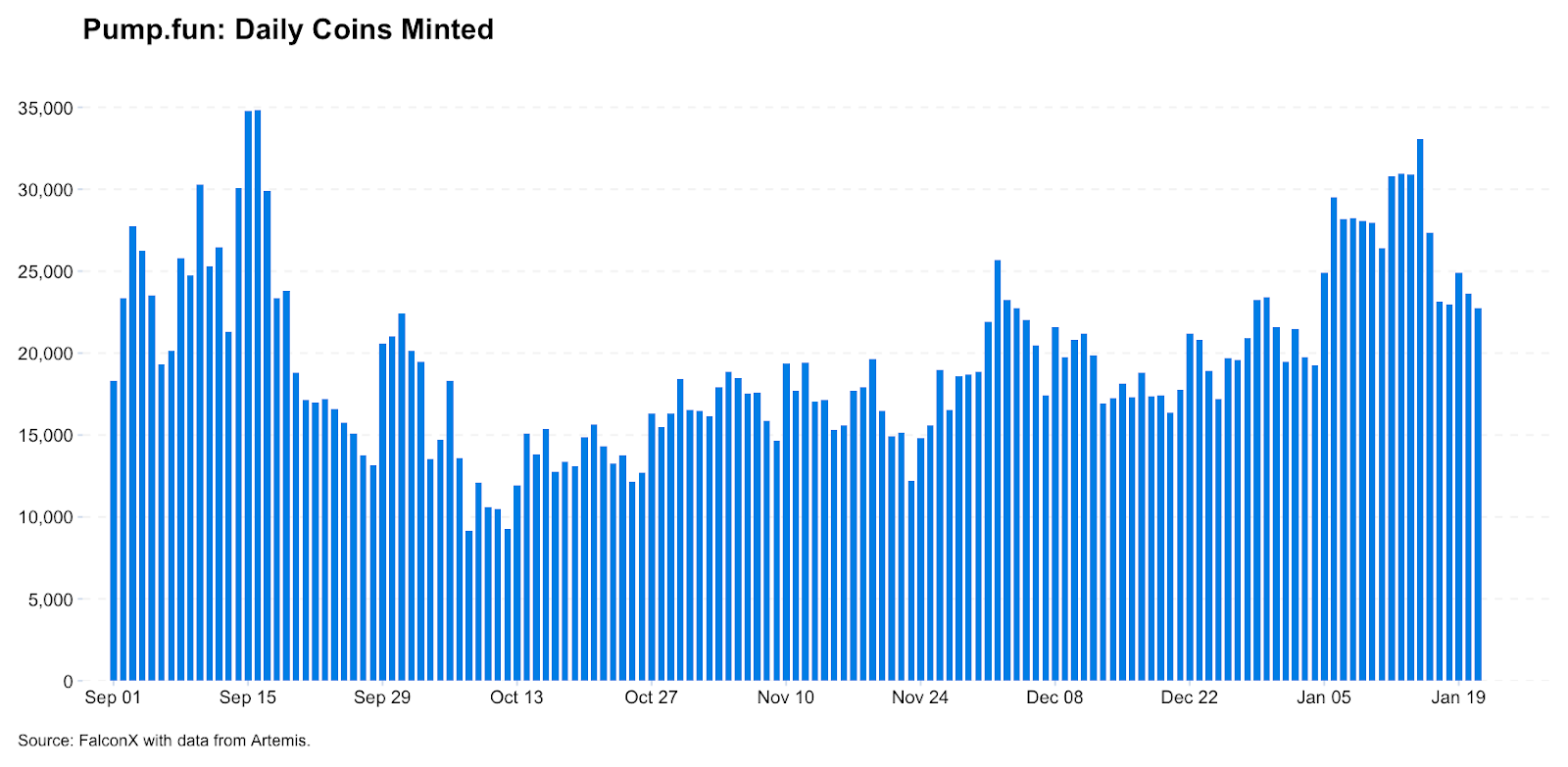

As we lap the 1-year mark of some of the largest memecoin launches in Q1 last year, PUMP is seeing notable traction in several areas. PumpSwap, the platform’s DEX, saw volumes spike to ATHs in the first few weeks of January, while fees have increased to the highest levels since September 2025, per data from DeFi Llama.

PumpSwap activity started ticking up in mid-December, with DAUs rising to over 400K on Jan 10th, the highest since at least May 2025. Interestingly, daily tokens created have been increasing since their local lows in October. Daily tokens launched hit 33,000 on Jan 15, with only ~200 graduating to PumpSwap pools, however.

The activity occurred around a period when 1) Crypto was broadly picking up again, with BTC rising to $95K, 2) Solana memes rallied (PONKE, BONK, WIF rose 70%+ in early Jan), and 3) Solana DeFi exhibited strength (RAY, MET jumped 30-40%). There were also some on-chain runners, such as WHITEWHALE, which ran up to a $200M FDV, something that did not occur in a long time despite how ephemeral these token moves can be (it is now -82% its high). The markets seems to have responded to Pump’s own activity and these adjacent developments, rallying as much as 70% mid-January from its ATL in December 2025. While many alts sold off strongly on recent macro headlines, PUMP remains +44% from late December as of writing.

These developments come after creator fee sharing was introduced in January, helping drive transparency and trust with tokens created on its platform. This grows on the release of dynamic fees in September 2025 where creator fees decrease as their coin’s market cap increases to push more sustainable token launches and to support trading volumes.

Pump also announced an investment fund to advance its ecosystem, starting with a $3M hackathon. By funding projects building on Pump fun, it could draw in more serious creators who could in turn drive activity. The goal seems to be attracting teams that aim to build real products around a token rather than memecoins, signaling a potentially broader shift. The team has also signaled further updates to creator fees and its mobile offering.

As of Jan 23, 2026, PUMP is tracking $454M of annualized revenue, amongst the greatest revenue run-rate in the industry, with a Price/Revenue multiple of 3.2X, one of the lowest, according to data from Artemis. At current run rates, PUMP is generating similar revenue to HYPE ($514M annualized) but trading at 1/3 the valuation. This could indicate a dislocation given PUMP has successfully been able to fend off launchpad competitors, while HYPE is seeing competition from newer perp futures platforms such as LIT.

PUMP has allocated approximately 100% of its revenue to buybacks since late July 2025, and has offset over 20% of its circulating supply from buybacks to date. With rising activity, the questions turn to whether the market will continue to discount future prospects for its platform, or whether the buybacks will finally drive price action. With the token recovering YTD, it’s possible both conditions are inflecting constructively.

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd., nor Banzai Pipeline Limited service retail counterparties, and the information on this website is NOT intended for retail investors. The material published on this website is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this website is not and should not be regarded as investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

No discussion of a particular company or product shall be considered an endorsement of such company or product. FalconX, and its affiliated parties may hold positions in assets discussed, which may change without notice. Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory, and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over-the-counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered with the U.S. Commodities Futures Trading Commission (CFTC) as a swap dealer and a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is a registered Class 3 VFA service provider with the Malta Financial Services Authority under the Virtual Financial Assets Act of 2018. FalconX Limited is licensed to provide the following services to Experienced Investors, Execution of orders on behalf of other persons, Custodian or Nominee Services, and Dealing on own account. FalconX’s complaint policy can be accessed by sending a request to complaints@falconx.io

"FalconX" is a marketing name for FalconX Limited and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.