Exploring Derive's Record Options Surge

Derive is seeing a jump in options and perps activity. BTC options volumes are soaring, while HYPE perp volumes have picked up substantially.

After years of building, Derive’s activity is ramping up around recent market volatility, with record on-chain options volume of $294M for the week ending March 7, 2026. It comes as the crypto options complex has grown immensely in the past year. BTC options notional open interest totals around $63B across leading venues as of Mar 10, 2026, up from roughly $39B a year ago.1 Derive is just 0.8% of this market today in open interest terms, per data from Coin Metrics, but could capture a growing share over time as one of the few decentralized players in this space. Indeed, its daily notional option volumes have grown to nearly 8.0% of Deribit’s as of March 10. Hyperliquid demonstrated decentralized exchanges could compete with centralized venues in perps, and Derive may deliver the same in the options space as on-chain options trading proliferates.

Derive’s Evolution

Derive was originally founded as Lyra Finance in 2021 as an application on the Optimism L2 with a primary focus on options. In 2023, it transitioned to its own app-chain built on the OP stack. It later rebranded to Derive in 2024, as it expanded its focus to a broader suite of derivatives products, now offering options, perpetual futures, and spot. The protocol’s investors reportedly include Framework Ventures, GSR, and most recently Variant.

Lyra Finance was built around the Synthetix ecosystem, using sUSD and other synths as collateral. It allowed users to trade cash-settled European options via its AMM. Challenges with this primitive included the potential for impermanent loss and options mispricing, as well as the limitations of a fully collateralized model. The capital inefficiency was amplified by the protocol’s reliance on sUSD, which was typically required to be overcollateralized by several hundred percent.

The protocol solved these pain points by transitioning to a Central Limit Order Book (CLOB) with its appchain launch, and by shifting away from Synthetix assets toward less capital-intensive collateral assets like USDC. Derive’s appchain is built on the OP Stack.

The project initially launched its LYRA token in 2021. In May 2024, it announced a token revamp and migration plan to the new token, DRV, which went live in January 2025.

Activity Trends

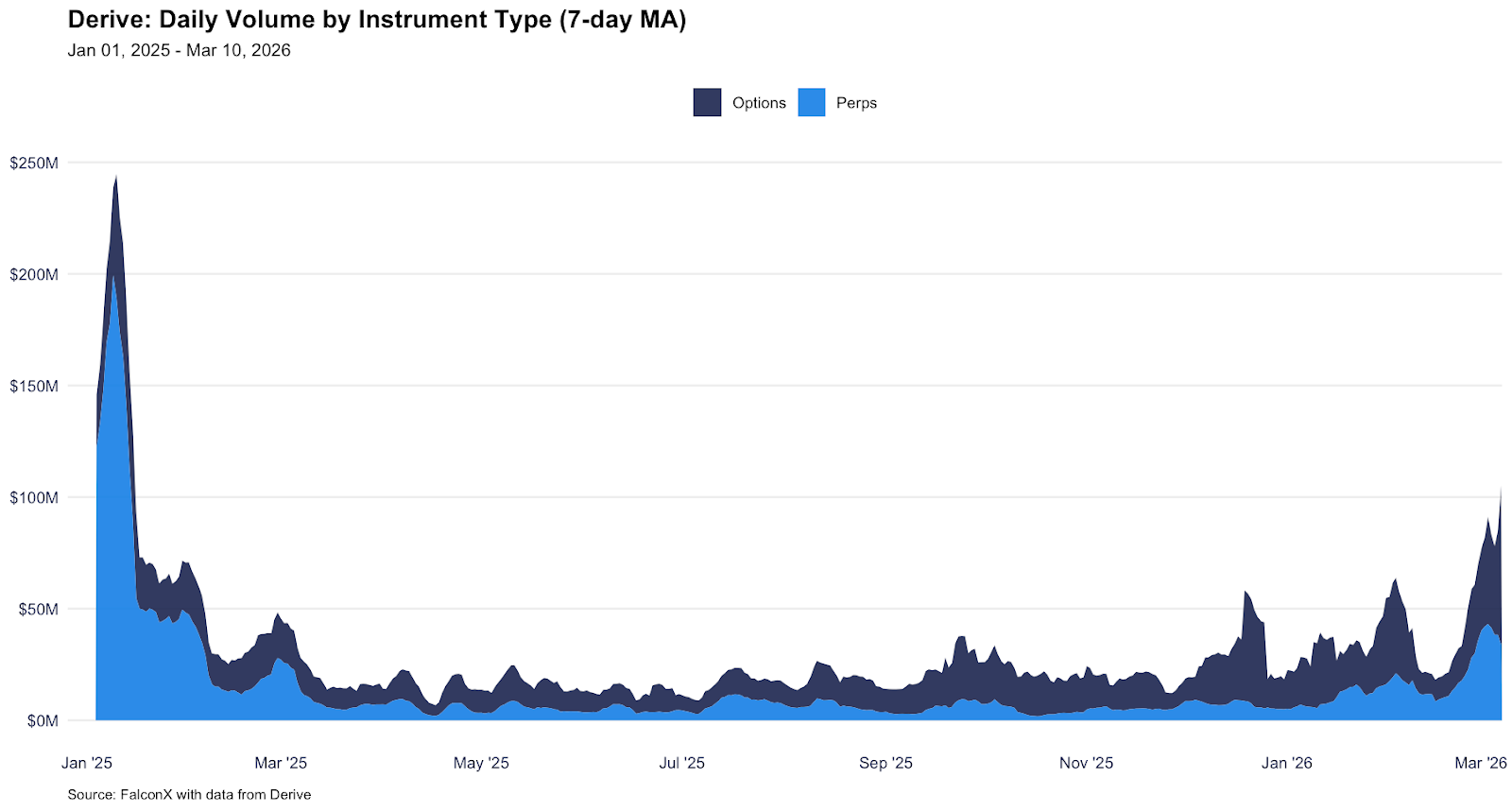

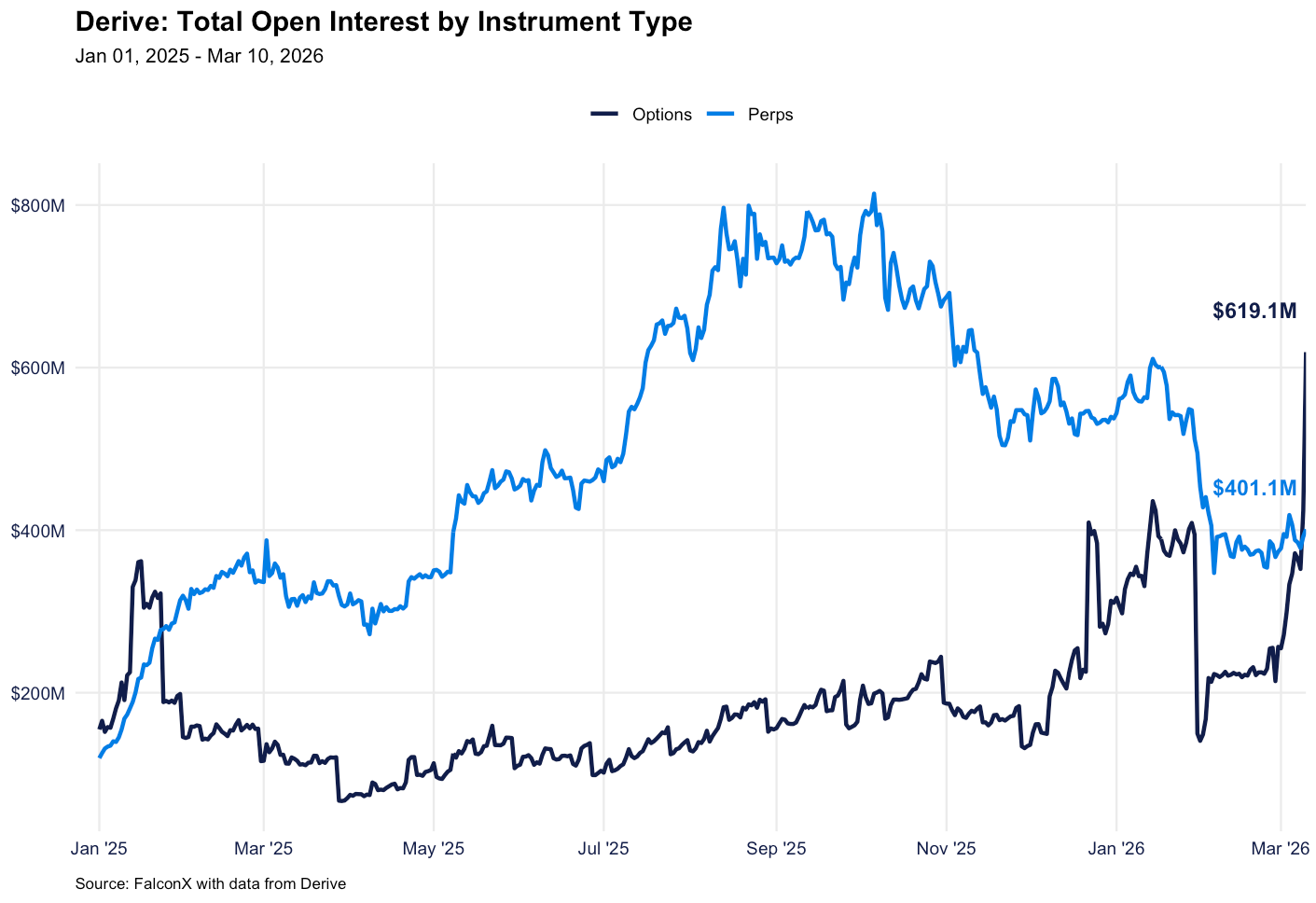

Activity on Derive has ramped up sharply in recent weeks, posting volumes of over $1B notional in February 2026, a record when comparing its post-airdrop activity. This momentum has accelerated into March, pushing total open interest over $1B as of March 10. This latest surge has been aggressively driven by options, which now comprise 61% of total open interest compared to 39% for perps, a rapid structural shift from the end of February when perps still held the majority share.

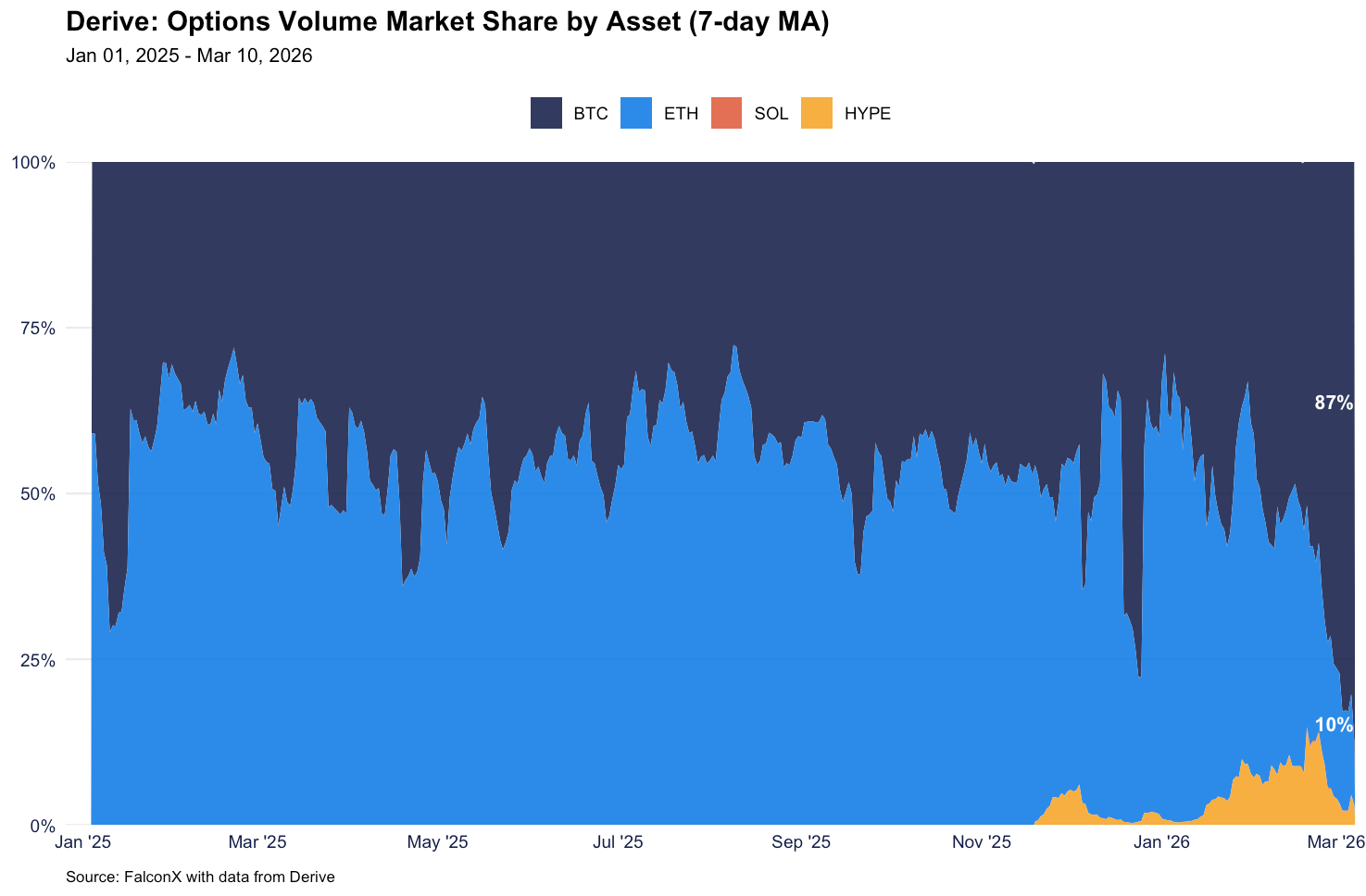

Similar to derivatives activity on CEXes, BTC and ETH dominate activity on Derive. Per data from Derive, BTC (79%) and ETH (17%) comprise the vast majority of its options open interest. On the perps side, ETH has relatively more activity (61% of perps open interest vs BTC at 36%). SOL and HYPE round up remaining markets with meaningful activity.

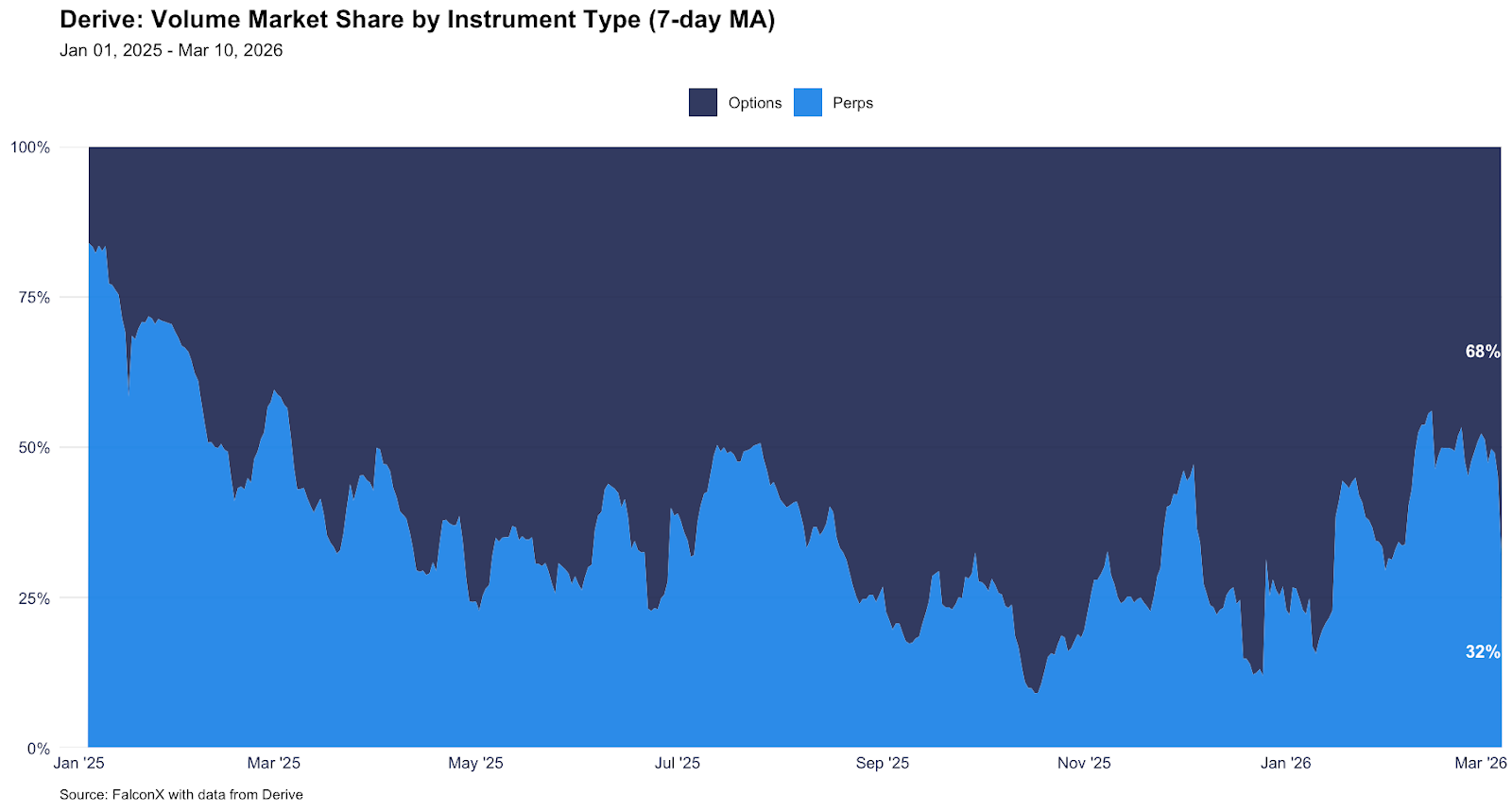

Since 1Q25, options have seen a growing share of volumes, although perp volume has increased in 2026. As of March 10, 2026, on a 7D basis, options and perps comprised 68% and 32% of volumes, respectively. Most recently, Derive experienced a surge in BTC options activity. BTC options OI increased from $161M at the end of February 2026, to $488M as of March 10, jumping roughly 3X. Growth in options volumes was also largely driven by BTC, with the platform seeing its largest trade in history on March 10 ($130M+ BTC options structure).

Another driver of volumes have been HYPE markets, which have increased to 3% of options volume and 4% of options open interest. HYPE has also grown to 41% of perp volumes despite only comprising roughly 1% of perps open interest. This has been attributed in part to larger traders using these markets to hedge, as well as the ability to use wHYPE and kHYPE from Kinetiq as collateral, further increasing capital efficiency.

Drivers Behind the Growth

According to the Derive team, there are several drivers in the past year powering the rise in activity.

Institutional liquidity. The onboarding of market makers, including FalconX, has helped improve depth and pricing to the point where Derive is competitive with leading venues. This has in turn, helped attract activity. Moreover, traders enjoy a competitive fee schedule relative to other venues which may help with flows. The introduction of off-exchange custody this year may also be a catalyst for institutional activity.

Request-for-Quote (RFQ): Derive launched RFQ for single and multi-leg structures for standard and custom options trading strategies. While single leg RFQs have been popular to trade large blocks, multi-leg RFQs have found traction with sophisticated options traders and funds looking for bespoke risk management, hedging and yield generation strategies. With blocks as large as 1,000 BTC and 100,000 HYPE options, RFQ has been successful in attracting experienced traders and investors.

Position as a decentralized and neutral venue. Derive noted accelerated growth following the Deribit sale to Coinbase, attributing this to Asian desks seeking a neutral venue. Derive may also be seeing a lift in activity after the crypto selloff on October 10, 2025, where ADL concerns and outages are thought to be driving activity to DEXes due to their non-custodial nature and potential for more predictability through transparent mechanics. The platform’s uninterrupted operational performance on October 10 gives it further credibility in this area.

Launch of altcoin options. Derive has differentiated itself by offering options markets on altcoins, while CEX venues often have options markets for just a small set of tokens. HYPE’s growing share of open interest and volume demonstrates increasing appetite for these kinds of markets.

Tokenomics

The DRV token is currently around 58% circulating, according to data from CoinGecko. 25% of protocol revenue is used for weekly DRV buybacks.The remaining 75% of revenue goes to the treasury and insurance fund.

Derive increased its total supply by 50% in late 2025 to help retain contributors and growth initiatives, such as institutional partnerships, integrations, and market maker incentives. 46% of the supply mint (230M tokens) was earmarked for core contributors and vests over 4 years. Moreover, to align this with the growth of the protocol, this allocation is non-transferable until certain conditions are met, such as the 30D TWAP market cap of DRV equal to at least $150M at the time of vesting. The remaining 54% of the mint was for strategic allocations, with 25% vesting immediately and 75% vesting quarterly over 12 months.

In terms of emissions, the platform pays around 50K DRV/week for trading rewards, with anyone trading on the platform eligible. Staking rewards total around 250K/DRV week. With the most recent weekly buyback at 643K DRV, it appears this level of trading activity is more than offsetting the supply, although buybacks remain subject to change by DAO governance.

Looking Ahead

Derive has highlighted plans to focus on growing institutional activity in 2026, with its off-exchange custody arrangements potentially unlocking activity with funds or trading firms that prefer this kind of operational set up. Derive also plans to launch more altcoin markets, building on the success of markets such as HYPE.

Moreover, Derive may benefit from broader demand for on-chain yield generation. As futures basis and on-chain yield remains compressed, traders could look to options to generate yield, such as call overwriting strategies. Given its position as the largest on-chain options venue by open interest, per DeFi Llama, Derive could see activity scale alongside demand for these strategies.

1 FalconX calculation per data from Coin Metrics, Velo, and Bloomberg.

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd., nor Banzai Pipeline Limited service retail counterparties, and the information on this website is NOT intended for retail investors. The material published on this website is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this website is not and should not be regarded as investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

No discussion of a particular company or product shall be considered an endorsement of such company or product. Past performance is not indicative of future results. FalconX, and its affiliated parties may hold positions in, act as a market maker for, or otherwise have a financial interest in, assets discussed herein, and may benefit from any price movements or transactions involving the subject company. This may change without notice. Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory, and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over-the-counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a swap dealer with the U.S. Commodities Futures Trading Commission (CFTC) and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is a registered Class 3 VFA service provider with the Malta Financial Services Authority under the Virtual Financial Assets Act of 2018. FalconX Limited is licensed to provide the following services to Experienced Investors, Execution of orders on behalf of other persons, Custodian or Nominee Services, and Dealing on own account. FalconX’s complaint policy can be accessed by sending a request to complaints@falconx.io

"FalconX" is a marketing name for FalconX Limited and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.