Paradex Gains Market Share, HYPE’s Commodity Markets Surge, USDE Inflects to Growth

The perp-DEX wars are heating up with Paradex gaining market share in recent weeks, while Hyperliquid is seeing record activity in its HIP-3 markets, driven by silver and gold markets. Meanwhile, Ethena’s USDE stablecoin has inflected back to growth, historically a barometer for a broader crypto recovery.

Paradex

Paradex is among the next generation of perp DEXes seeing traction as it approaches a potential TGE of its DIME token. It had previously extended its Season 2 rewards program by another 6 months at the end of July 2025, and it is now coming up to the end of this period.

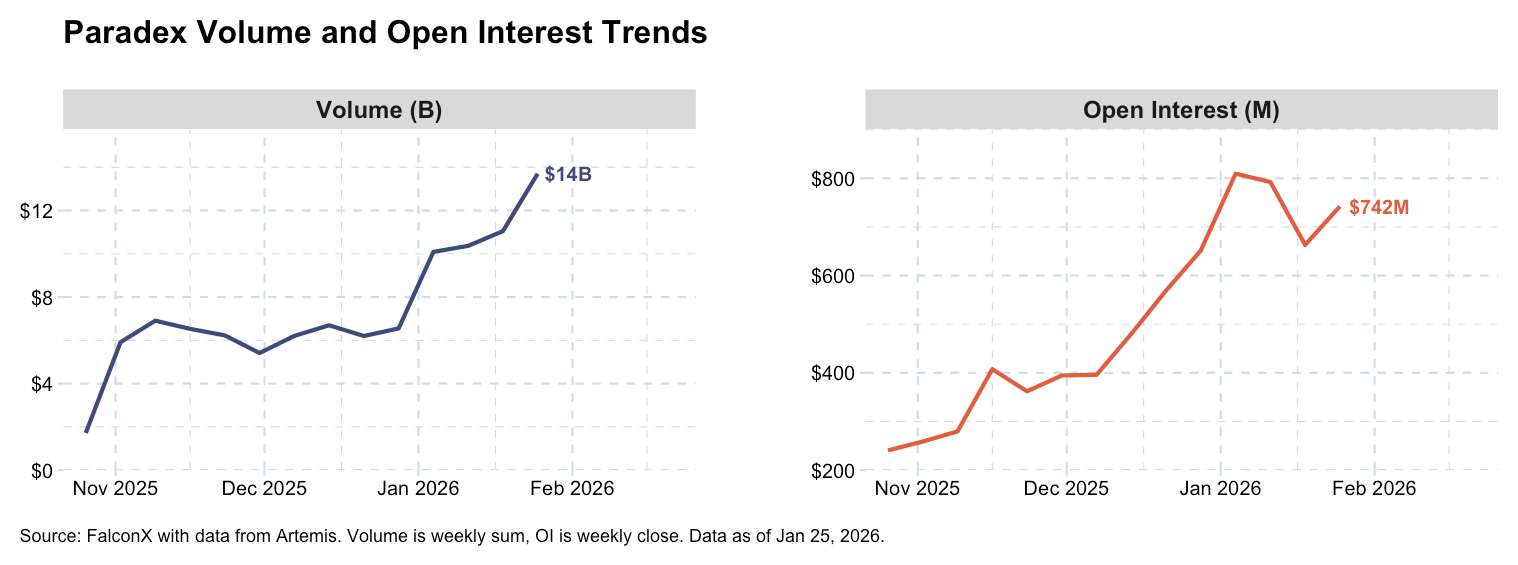

Its 30D volumes, as of January 25, 2026, are up 71% sequentially, according to data from Artemis. The trend has accelerated most recently with 7D volumes rising 8% from the prior week. Open interest of $743M is nearly 3x higher than in September 2025, highlighting its rapid growth. This is despite an incident on Jan 19, where a technical bug during a maintenance upgrade caused erroneous pricing, triggering liquidations. Paradex later performed a chain rollback to restore balances and positions to the pre-incident state, and refunded impacted accounts.

Paradex is a perps DEX built as an L2 appchain (Starknet/CairoVM). While it leverages off-chain order matching and on-chain settlement, similar to its peers, it has several key differentiators:

Zero Fees for Retail Traders. Paradex does not charge fees for retail traders, which it classifies as traders using the UI. Instead, only API traders (‘Pro’) traders pay up to 0.3/2 bps maker/taker fees.

No auto-deleveraging (ADL). Paradex uses a socialized loss mechanism instead, where losses are deferred until withdrawal vs being immediately realized. This is a key consideration for traders after the October 10th, 2025, crypto crash, where ADLs across the industry demonstrated the drawbacks of these mechanisms.

Privacy. Account and position data are private to the account holder on Paradex, whereas many perp DEXes have this information publicly available. This is a feature large traders looking to shield their positions from being hunted or front-run could benefit from. This is enabled in part by a custom RPC configuration and by encrypting blob data posted to the Ethereum L1.

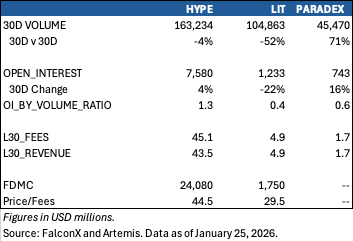

Looking at leaders HYPE and LIT as comps, Paradex could see an FDV of approximately $600-$900M if it trades on similar Price/Fee multiples.1

Hyperliquid

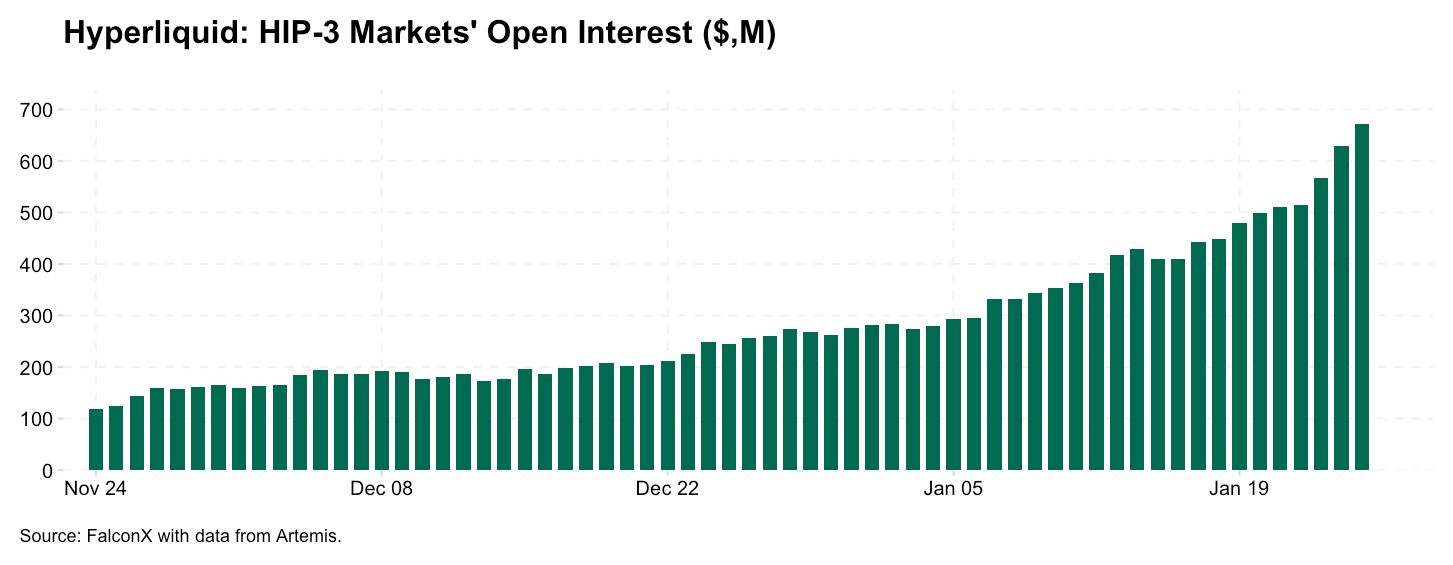

Along the line of perp-market activity, Hyperliquid’s HIP-3 markets are seeing a revival after volumes saw a lull into year end.

Open interest across HIP-3 markets stood at a record $671M as of January 25, 2026 while daily volume saw a peak of $941M on January 21, 2026 according to data from Artemis. Per the project itself, activity is even higher, citing an ATH open interest of $790M, up 3x from a month ago.

Driving the growth are commodity markets, such as silver and gold. It’s a sign that on-chain traders are pivoting to alternative markets when crypto has remained rangebound or down. Moreover, the activity can be partly attributed to HIP-3 deployers enabling “growth-mode” for their markets, a feature that slashes fees by 90%.

And while the growth remains impressive, there may be heightened competition going forward. In addition to other perp DEXes supporting commodity markets, centralized exchanges including Binance have launched similar markets, such as perpetual futures on equities like TSLA.

USDE

One barometer of returning demand for leverage is Ethena’s USDE, given that the stablecoin allows holders to access yield from its basis trade activities. According to data from Artemis, USDE peaked at a $14.8B market cap on October 6, 2025, before declining the rest of the quarter. It bottomed out at $6.3B on Dec 31, and has since increased 5% to $6.6B.

SUSDE, the staked version that offers yield, followed a similar course, peaking at $6.1B around the conclusion of Season 4 rewards in late September and troughing around $3.4B in late December. Notably, SUSDE market cap started picking up a week before USDE’s did and has now recovered to $3.8B.

The prior bottoms for these both occurred around May 2025, roughly one month after the total crypto market cap saw its lows around the tariff sell off. Another instance showed similar results: USDE troughed in October 2024 around when the crypto market started to move higher. If history repeats, this is a signal that more on-chain activity is returning to the crypto market and could support a broader recovery.2 Supporting this notion is an increase in AAVE’s outstanding loans, which have grown from $20B from its November low to over $23B as of writing.

1, 2 This projection is speculative and subject to significant uncertainties, including market volatility and competitive dynamics.

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd., nor Banzai Pipeline Limited service retail counterparties, and the information on this website is NOT intended for retail investors. The material published on this website is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this website is not and should not be regarded as investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

No discussion of a particular company or product shall be considered an endorsement of such company or product. Past performance is not indicative of future results. FalconX, and its affiliated parties may hold positions in assets discussed, which may change without notice. Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory, and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over-the-counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered with the U.S. Commodities Futures Trading Commission (CFTC) as a swap dealer and a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is a registered Class 3 VFA service provider with the Malta Financial Services Authority under the Virtual Financial Assets Act of 2018. FalconX Limited is licensed to provide the following services to Experienced Investors, Execution of orders on behalf of other persons, Custodian or Nominee Services, and Dealing on own account. FalconX’s complaint policy can be accessed by sending a request to complaints@falconx.io

"FalconX" is a marketing name for FalconX Limited and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.