Inside the Crypto Options Boom: Three Significant Shifts Shaping this Market

The crypto options market is now large and diverse enough to matter for price discovery in its own right. Open interest has scaled to futures-like territory, IBIT and Deribit are cultivating different client bases, and the vol surface is sending interesting signals.

Those looking for a year-end crypto rally have reasons to be encouraged. As this note goes to press, BTC is hovering near all-time highs; XPL and 2Z have launched their networks with highly anticipated token debuts, and Token 2049 in Singapore runs in full swing, with a steady stream of announcements. The ten best-performing tokens with a circulating market capitalization over $10 billion are all delivering double-digit gains in the past seven days.

Despite its relative underperformance this week, however, BTC is grabbing the broadest headlines. In what JP Morgan dubbed “the debasement trade”, the largest crypto asset seems to be rehearsing a catch-up with gold’s stellar performance of late and maybe ending a flat market over the past many months.

But if spot market price action has felt becalmed these past six months, don’t mistake that for stasis in the entire market. The crypto options market has been anything but quiet.

The chart below tracks notional open interest in the two dominant BTC option instruments, Deribit’s contracts and options on IBIT. We’re now approaching the $80 billion mark, roughly ten times the early-2024 levels, with the majority of this growth occurring over the past six months. That scale puts Bitcoin options on par with the BTC futures complex (including both perpetuals and dated contracts), a remarkable trend in how views are being expressed in the crypto market.

Two reasons make the crypto options tape essential reading now for those seeking additional market context.

First, the market is large enough that options flows from both the buy-side and from dealer positioning can feed back into the underlying asset price. As a result, option market dynamics are likely shaping the underlying market price action more than ever before. Second, because options allow investors to express finely tuned views (through different strikes, maturities, and skew), this market also functions as a real-time poll of positioning and risk appetite, offering a clear window into the thinking of a sophisticated slice of the market.

We take up the thread with three focal points: the deepening links between traditional finance and crypto; a comparative profile of the leading options venues; and what today’s implied-volatility surface is signaling.

Trend 1: The stunning rise of TradFi crypto options

It’s now commonplace to note that traditional finance price action is exerting more influence on crypto. We flagged the growing role of TradFi flows in price formation back in May, and the theme has only gained traction since.

More recently, it’s becoming clear that this trend might be even stronger in options than in the spot market.

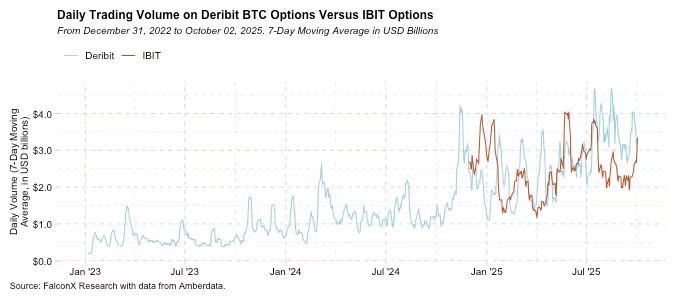

The chart below plots open interest in Deribit BTC options (blue) versus IBIT options (brown). Although we need to acknowledge that Deribit’s post-quarterly-expiry open interest dip is likely temporary, IBIT options are, before their first anniversary, already matching Deribit’s nearly decade-old BTC option contracts.

Volumes tell a slightly different story. IBIT options briefly eclipsed Deribit’s just after launch, probably helped by debut enthusiasm, before slipping behind in recent months. Even so, IBIT has been changing hands at a solid $2–3 billion a day, within shooting range of Deribit’s $3–4 billion daily average.

Put simply, Deribit’s open interest and volumes remain deep and growing, but the crypto options’ center of gravity is starting to shift to TradFi venues just like in other corners of the market.

Trend 2: The increasing sophistication and diversity of crypto options market participants

Trading venues can cater to different audiences, and some of those differences can be seen through simple market indicators.

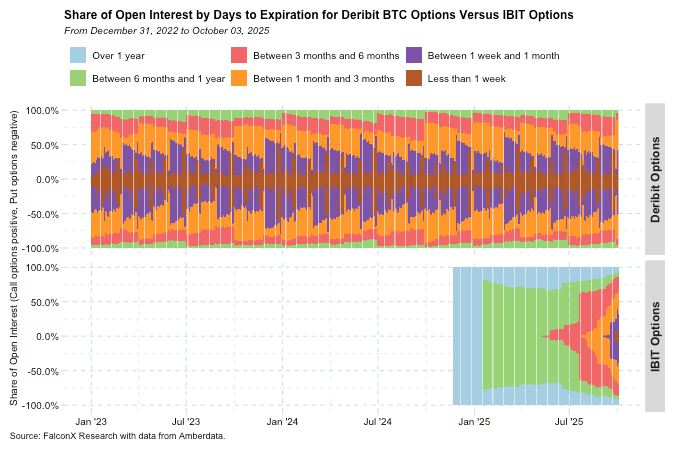

The chart below splits open interest by days to expiration for BTC options on Deribit (top) and IBIT (bottom). Bars are stacked by tenor, with calls plotted above zero and puts below. The main message there is that Deribit remains dominated by sub-three-month tenors with a weekly/monthly cadence, underscoring classic crypto-native flow.

IBIT, on the other hand, launched with an outsized long-dated call footprint (six months to over a year) consistent with institutional hedges, long-tenor upside optionality, and overwrite programs. While through 2025 the belly (1–6 month tenors) has filled in, the long-tenor bias versus Deribit options remains.

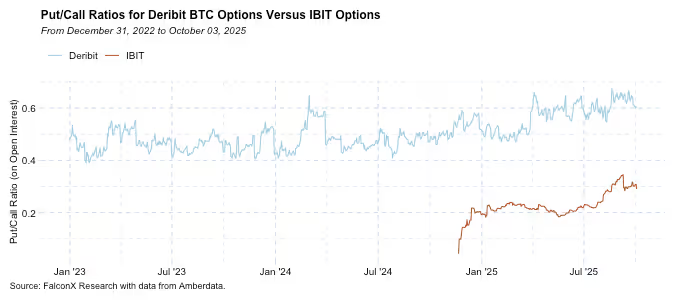

Put/call ratios (on open interest) also show a significant difference across both venues.

As the chart below shows, put/call ratios run significantly higher on Deribit (hovering around the 0.5-0.6 range) and lower on IBIT (just recently building into the 0.3s). A credible interpretation of this data is that dealers and fast-money vol desks that need to hedge delta/gamma/vega continue to gravitate to Deribit; IBIT books must absorb close-to-open and weekend gap risk, so the flow could be skewing more toward programmatic call overlays and longer-dated structures that tolerate less re-hedging.

All in, these two venues are complementary but distinct. Deribit sets the near-term rhythm with short tenors, expiry-driven gamma, a higher put share, and true around-the-clock risk management. IBIT imports a TradFi options DNA, with longer horizons and call-centric positioning.

This dynamic can change in the future, especially now given how fast market structure is changing. CME’s move to 24/7 Bitcoin futures trading in 2026 is an early marker, and maybe a prelude to more listed venues adopting the clock the underlying keeps. Over time, crypto-native and TradFi venues may converge on hours, depth, and tenor mix. For now, however, there are important distinctions across venues.

Trend 3: Implied BTC vols continue to dive but also diverge from ETH’s

If there’s been one constant in 2025 options chatter, it’s that BTC implied volatility has stayed remarkably low.

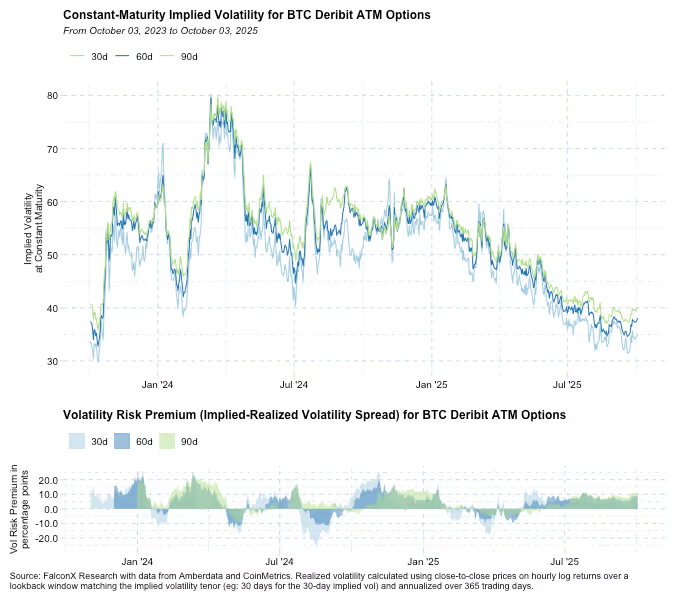

The top panel in the next chart tracks constant-maturity BTC implied vol at 30, 60 and 90 days. We focus on Deribit for its longer history, which makes the time-series comparison cleaner. The downtrend is unambiguous: After last year’s spikes, implieds have eased into the high-30s to low-40s, roughly half the levels that were common just a year ago.

But there’s an important caveat.

The lower panel plots the volatility risk premium (implied minus realized). The key message is that despite low absolute implieds, the spread remains positive and not far from its historical band. Option sellers are still earning typical carry, and buyers aren’t necessarily getting a fire sale at these levels. In short, it appears that implied volatility is low mainly because realized volatility has collapsed, not necessarily because the market is systematically underpricing risk.

The main question is when this setup will change.

A jump in realized volatility could come from many places (a macro shock, a regulatory jolt, or a crypto-specific stress), but the gauge to watch is the implied–realized spread (aka the volatility risk premium). If that cushion compresses or turns negative, short-vol carry becomes less attractive and positioning can unwind. The tells are familiar: a front-end flip (short-dated options bid over longer-dated), a steeper put skew as investors reach for near-term downside, and faster dealer hedging that can amplify spot moves.

In such a regime, option prices often re-rate higher, typically first at the front of the curve, then progressively out the term structure. More importantly, the unwind can tug directly on spot: when dealers are short gamma, hedging compels them to sell into declines and buy into rallies, amplifying swings. A burst of put demand forces additional delta hedging, adding mechanical selling pressure. Given the scale the options market now commands, this is an example of how tracking options flow is central to anticipating the spot price action.

Another, less explored side of the vol compression story is that it has been more of a BTC phenomenon.

The chart below shows implied volatilities of Deribit BTC and ETH options on a constant maturity basis (30d, 60d, and 90d). While BTC and ETH implied volatilities used to move somewhat in lockstep, they started to diverge in mid-2024 and are now significantly apart.

Expect the BTC–ETH vol gap to feature more prominently on options desks’ calls.

On the BTC side, steady yield-overlay supply from covered calls and collars from miners and DATs could keep implieds heavy and help sustain the spread. ETH, by contrast, offers alternative income channels (staking, DeFi), so less yield demand is forced through options.

Another factor that could be helping sustain this spread more recently is the higher ETH realized volatility profile.

On the other hand, a build-out of ETH overwrite programs or structured mandates, or simply a view that a 20-vol-point premium is too rich, inviting relative-value sellers, could make this spread shrink.

All in, indicators from the options signals point in one direction: this market is now large enough, and diverse enough across venues, to matter for price discovery in their own right. Open interest has scaled to futures-like territory, IBIT and Deribit are cultivating different client bases, and the vol surface is sending a nuanced signal: Cheap in absolute terms but not mispriced versus realized, with BTC–ETH dispersion that invites relative-value trades.

For risk managers and allocators, this trend will argue for watching two dashboards: Deribit flows for the 24/7, short-tenor and event-driven tape, and IBIT flows for U.S.-listed options flow that’s more call-centric and longer-dated.

David Lawant, Head of Research

Martin Gaspar, Senior Crypto Market Strategist

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd. nor Banzai Pipeline Limited service retail counterparties, and the information in this material is NOT intended for retail investors. This material is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this material is not and should not be regarded as investment advice, investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over the counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a Swap Dealer with the U.S. Commodities Futures Trading Commission and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is licensed by the MFSA as a Class 2 Crypto-Asset Service Provider (Regulation (EU) 2023/1114). It is also licensed as a Financial Institution (Cap. 376) exclusively for EMT payment services.

"FalconX" is a marketing name for the FalconX Group and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.