SOL ETFs, Token Buybacks, and Declining Pre-Launch Valuations

.avif)

Despite a slow bleed in the crypto markets, there were several noteworthy developments for crypto investors in the past week. The successful launch of spot SOL ETFs, a proliferation of buyback programs amongst DeFi projects, and compressing pre-launch valuations for upcoming TGE projects highlight how traders and projects are reacting to market conditions.

SOL ETFs go Live

Last week saw the launch of the first US spot ETFs for SOL, LTC, and HBAR despite the government shutdown, thanks to a process outlined here. The most anticipated launches were for Solana, as a top 5 Layer 1 project by market cap. There, Bitwise’s BSOL and Grayscale’s GSOL products went live, notably both with staking. BSOL saw impressive traction by all accounts, with analysts noting it was the top ETF launch of 2025 by day 1 volume ($56M).

The launches were successful, with both vehicles seeing net inflows ($275M and $9M, respectively). BSOL launched a day ahead of GSOL, which may help explain why it saw meaningfully greater flow, in addition to its lower fees (gross expense ratio of 20 bps vs. 35 bps, respectively). Note both products are offering a fee discount for their first 3 months of trading.

There are some nuances in the staking activities of these vehicles. GSOL targets staking 100% of its SOL holdings and intends to pass on 77% of net staking rewards to investors. BSOL, on the other hand, intends to stake 100% of its SOL holdings and will pass on 100% staking rewards initially. The high staking rate makes sense considering BSOL has T+2 redemptions, while the unstaking period for Solana is typically under 2 days. Per its filings, for any delay in unstaking to meet redemption requests, BSOL will trade with a third party to source the SOL in time.

The inflows for these SOL ETFs were strong in aggregate and helped dispel fears that DATs may reduce demand for these vehicles, in part due to their availability on brokerages and greater ability to participate in yield generation activities. Given spot ETFs now have staking, it is possible this pushes DATs to further dip their toes into DeFi, such as by restaking or yield farming, to remain competitive vs ETFs.

We note that on a market cap-basis, the SOL ETF launch was just as strong as that of the BTC ETFs and stronger than the ETH ETF launch. By day 6, SOL ETFs had taken in net inflows equivalent to 0.33% of its market cap, which compares to 0.14% and -0.10% for the BTC and ETH ETF launches, respectively. One contributing factor here may be a smaller presence and more competitive fees from the converted Grayscale SOL trust. The conversions of Grayscale’s BTC and ETH trusts into ETFs were long-awaited liquidity events for their investors, leading to heavy outflows from these products in the days after trading began.

Day 1-6 Comparative Spot ETF Flows ($, M)

Buyback Proliferation

Token buybacks continue to be a preferred method of value distribution for leading crypto projects, with several DeFi powerhouses recently announcing new buyback programs.

Aave is contemplating a $50M annual AAVE buyback program using protocol revenue. While in line with its previous buyback pilot ($1M/week over 6 months), this further cements the program and demonstrates to investors it is serious about delivering value to token holders in the long run. The current program has some flexibility in the buyback amounts, which can range from $0.25M-$1.75M/week, allowing the DAO to take advantage of market conditions. The proposal passed a snapshot vote for the program on Oct 31.

EtherFi proposed an open-ended buyback program of up to $50M, where its foundation would use a portion of the treasury for buybacks when ETHFI trades below $3. For context, ETHFi has not traded above $3 for an extended period of time since 2024. Considering its trading volumes tend to be below that of AAVE, its buyback program of the same amount could have a more meaningful impact on its token price. While Etherfi previously conducted occasional buybacks, cumulative buybacks as of late October totaled $7.8M. The proposal passed a snapshot vote as of Nov 3.

Maple Finance also voted on a new buyback proposal. It calls for using 25% of protocol revenue for SYURP buybacks (currently generating $20M in ARR from fees) and sunsetting staking. The buyback ratio compares to 25% and 20% of revenue in earlier programs this year. The snapshot vote for the proposal passed on October 31.

TGE Valuations Are Collapsing

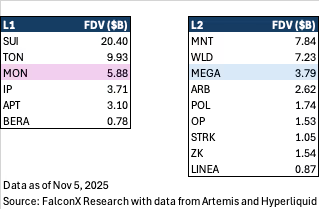

Pre-launch trading of upcoming token launches may be foreboding for the broader crypto market, with valuations collapsing for leading projects. Excitement from a relatively strong initial launch week for XPL has kept attention on high profile projects Monad (MON) and MegaETH (MEGA), both of which are expected to launch their tokens this quarter. Monad had its airdrop allocation reveal last week, while MegaETH had a massively oversubscribed token sale the same time.

In less than a month since pre-launch Monad perps on Hyperliquid launched, traders now price in an FDV of $5.9B for MON, vs. $10B+ earlier in October. MegaETH is seeing similar action, with pre-launch markets now trading at a $3.8B FDV vs a high of $5B+ in October, highlighting how traders are quickly souring on the prospects of these new launches.

Versus its peerset, MON now sees a 40%+ discount to newer L1s like SUI and TON, but is trading closer to IP, another L1 launch this year. The slide in implied valuation brings it closer to its $3B private valuation from 2024.

On the other hand, MEGA’s implied valuation would still place it amongst the top of its peerset, and would be the greatest FDV of a pure play L2 in the table below. Notably, the FDV compares to its recent token sale at a $1B FDV.

Of course, it’s important to keep in mind that volumes and open interest remain relatively low on these pre-launch markets (less than $10M in daily volumes in recent days) and thus may not be reflective of broader investor reaction come launch day.

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd. nor Banzai Pipeline Limited service retail counterparties, and the information in this material is NOT intended for retail investors. This material is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this material is not and should not be regarded as investment advice, investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over the counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a Swap Dealer with the U.S. Commodities Futures Trading Commission and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is licensed by the MFSA as a Class 2 Crypto-Asset Service Provider (Regulation (EU) 2023/1114). It is also licensed as a Financial Institution (Cap. 376) exclusively for EMT payment services.

"FalconX" is a marketing name for the FalconX Group and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.

.jpg)