Arbitrum: The AWS of Blockchains

Arbitrum is evolving from an L2 to a major infrastructure provider for enterprise blockchains, a shift set to be driven by its role in powering Robinhood Chain.

Vitalik Buterin’s recent comments on Layer 2 blockchains highlight the growing dichotomy between leading L2s and generic ones. In this piece, we explore how Arbitrum, a top L2 by economic activity, is differentiating itself across DeFi, RWA, and its tech stack that supports partner chains. All these components help drive economic value accrual to the Arbitrum DAO through the form of transaction fees and Arbitrum Expansion Program fees.

Moreover, Arbitrum’s key focus now sits as infrastructure for enterprise blockchains, such as Robinhood Chain. This has parallels to Amazon Web Services (AWS), which became a key provider of cloud tooling for businesses around the world. Arbitrum provides the customizable blockspace and tooling, enabling corporations to quickly bring their offerings to market. Through its own L2 offering and the Arbitrum Chain stack, Arbitrum is emerging as a major provider for blockchain infrastructure needs.

Setting the Stage: Vitalik’s View

In February 2026, Ethereum co-founder Vitalik Buterin provided a thought-provoking assessment of L2s, noting the original rollup-centric roadmap is no longer valid. He argues part of this is because many rollups have been slow to advance to stage 2 decentralization, which may be limiting full adoption. If L2s do not have strong security or decentralization guarantees, they are just bridges and should be viewed accordingly.

Furthermore, Vitalik points out ETH L1 is scaling effectively, noting low transaction fees and further plans to increase the gas limit, enabling capacity for more activity.

Consequently, he makes the case for why L2s should be seen as separate chains, not just extensions of Ethereum. He therefore argues they need to differentiate to attract activity and generate value-add for users. This could include altVMs, app-specific efficiency, extreme levels of scaling, unique designs for non-financial systems, or features such as privacy. L2s shouldn’t merely extend L1 properties, they should add to it.

Arbitrum’s Lens

Vitalik’s comments may be more geared towards generic L2s. In practice, the top 3 L2s by total value secured (ARB, Base, OP), as calculated by L2Beat, have been steadily building towards greater decentralization and are currently all at stage 1 (which compares to many other L2s at stage 0). Arbitrum itself was the first major L2 to reach these milestones and remains amongst the most advanced within that stage.

Moreover, Arbitrum co-founder Steven Goldfeder argues that rollups are now as much about customization and dominion as they are about scaling, especially for enterprises and apps that require their own environment. For the needs of these kinds of builders, the L1 may not be on the table.

On the customization front, Arbitrum innovations such as Stylus (enables writing smart contracts in multiple languages, such as Rust, C, Solidity), unique transaction ordering policies (Timeboost), and ultra-fast blocktimes (250ms), help attract developers and enterprises looking for more than what the L1 offers.

Moreover, Arbitrum has already differentiated itself through its significant activity on its L2, and now is evolving to engage in the enterprise blockchain space through its Arbitrum Chain stack. We explore these below.

Stablecoin and DeFi Presence

Arbitrum is a top L2 by DeFi TVL ($1.9B) and DEX activity, per DeFi Llama, as of April 1, 2026, and has $4.0B of stablecoins. Arbitrum is the 7th largest chain (including L1s) in terms of stablecoin market cap and is #2 in this regard amongst L2s. Per stablecoin market cap issued, Arbitrum is ranked #1 amongst L2s at $6.7B.

DeFi has a significant presence on Arbitrum. It is home to one of the largest Uniswap deployments across the space, trailing only Ethereum L1 by chain volume as of March 2026, per DeFi Llama. On a TVL-basis, Arbitrum has the third largest Uniswap deployment, with TVL as of $267M as of April 1, 2026. Moreover, Arbitrum is known as the home of several unique DeFi protocols, such as GMX, a pioneer AMM-style perp DEX.

Arbitrum is also a leading platform for lending applications. It sees the third largest Aave deployment across all chains ($745M TVL), behind Ethereum and ($20.0B) and Plasma ($1.4B).

Real World Assets (RWA)

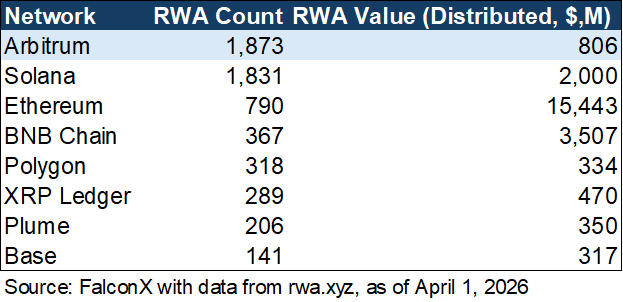

Arbitrum is a leader in the real-world asset space in terms of RWA count and RWA TVL, per data provider RWA.xyz. It is the #1 network in terms of RWA count (1,873 RWAs, as of April 1, 2026) valued at $806M, more RWA tokens than on Solana or Ethereum. Per the Arbitrum team, drivers behind this include growth in tokenized equities (including Robinhood's deployments), tokenized treasury growth (in part through its STEP program), and other assets like commodities and real estate.

Arbitrum L2 Activity

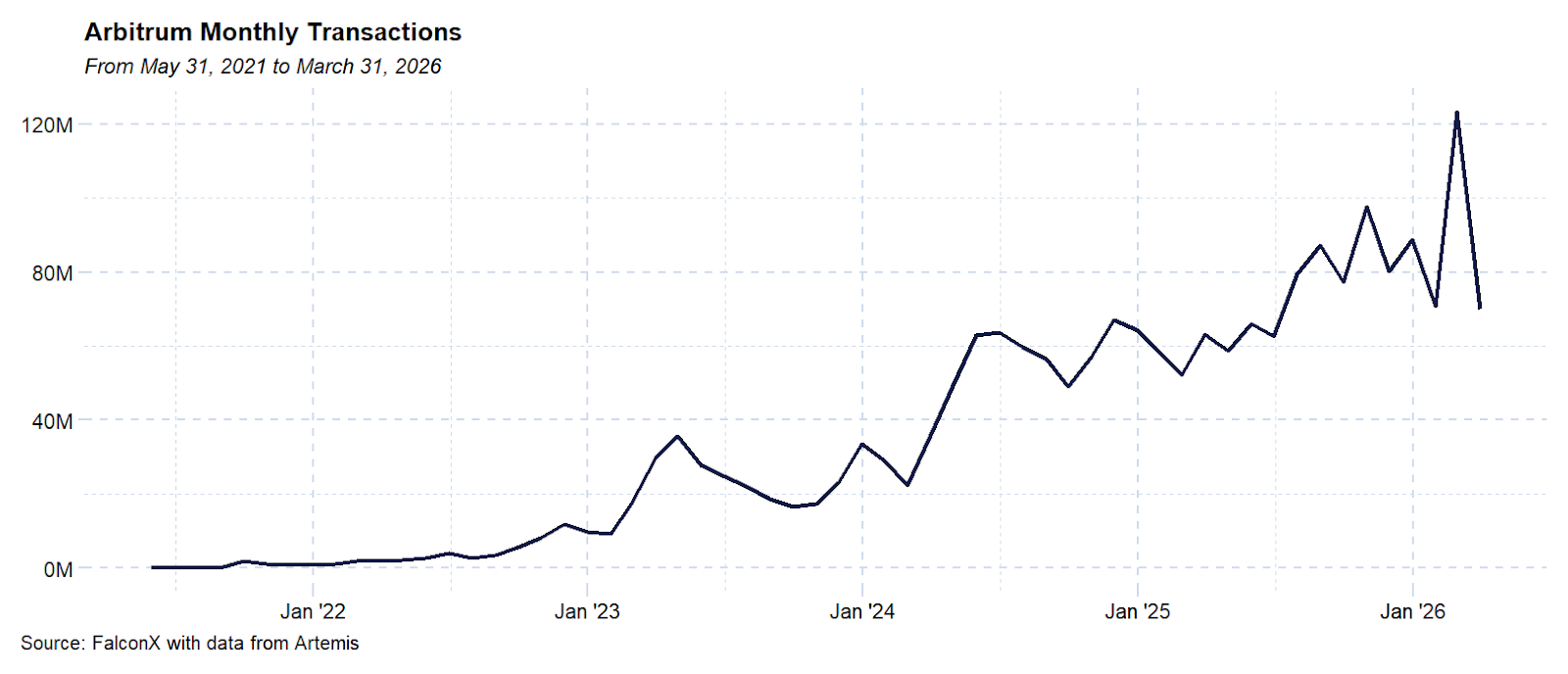

On its Layer 2 itself, Arbitrum is seeing activity surge in certain areas. Transactions have climbed to record highs. Meanwhile, its TVL has remained relatively sticky since 2023, hovering between $2B-$3B. The growth in transactions is largely due to the ArbOS 51 Dia upgrade in January 2026, allowing for greater capacity while reducing fee volatility. This upgrade reduced fee spikes but also raised the minimum base transaction fee. This improved user experience while demonstrating some pricing power on Arbitrum’s end.

Given such activity, Arbitrum is often compared to L1s directly rather than L2s. With its 250ms block times and soft finality of 1-2 seconds, Arbitrum is competitive with many top L1s (although it has a 7D challenge window before being able to withdraw to L1).

Moreover, Arbitrum has an edge in distribution. It has billions of dollars of liquidity and leading exchange and wallet support, making it a compelling solution for a project to launch on. Builders benefit from access to capital and top protocols on-chain, as well as access to leading vendors and tooling supporting Arbitrum.

Value Accrual and the Arbitrum Chains Approach

What further differentiates Arbitrum is its value accrual framework, which involves direct capture of sequencer fees from its primary L2 network and revenue-sharing from its Arbitrum Chains (L2s or L3s using the Arbitrum tech stack that settle to other chains). This structure supports a high-margin business model with zero token issuance for protocol security. These business lines are complimentary as they hedge for both a general purpose L2 model and the appchain model, both of which are playing out.

Arbitrum utilizes a "community source" model as part of its Arbitrum Expansion Program fee. While the code is publicly available, the Arbitrum Chain stack requires a 10% fee on net protocol revenue for chains that do not settle directly to Arbitrum One or Nova. This fee flows 80/20 to the ArbitrumDAO and Arbitrum Developer Guild, giving the DAO 8% direct value accrual from Arbitrum Chains.

The project has seen major corporate players select its tech stack for their on-chain efforts. Robinhood has been the most notable, launching tokenized stocks in 2025 on the main Arbitrum L2, with the goal of eventually shifting to its own chain. That vision is now being fulfilled with the testnet launch of Robinhood Chain in February 2026, a standalone L2 built on Arbitrum’s stack. This helps support the case that Arbitrum’s tech stack can be compelling for marquee partners. It also places Arbitrum at the forefront of tokenization activity through Robinhood’s efforts.

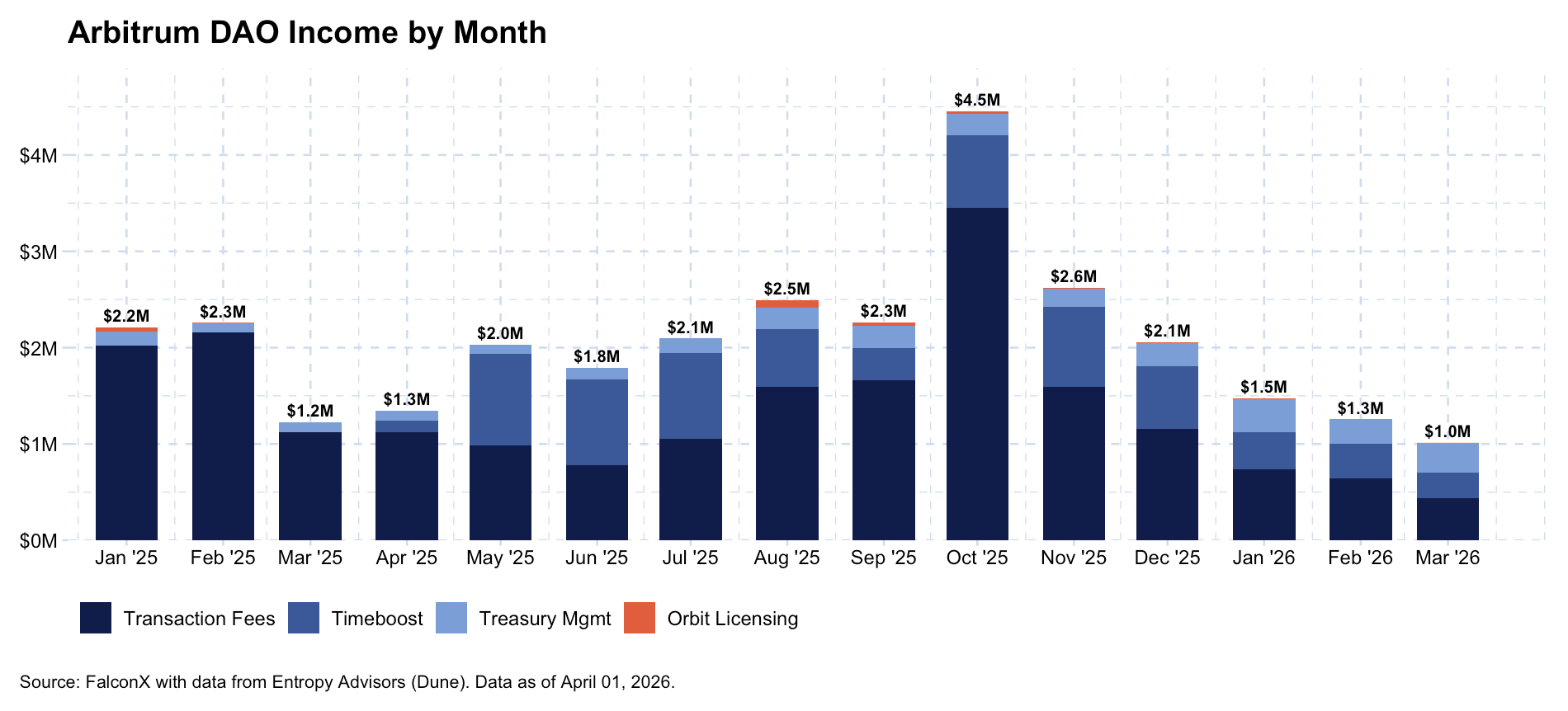

Other core revenue generating activities for the Arbitrum DAO involve Timeboost (MEV capture) and treasury management activities. Timeboost is a transaction ordering policy for Arbitrum chains, allowing chain owners to capture a portion of maximal extractable value (MEV) that would otherwise go to searchers. This process auctions off the right to a time advantage ahead of normal transactions, allowing them to capture certain MEV. Consequently, MEV seeking actors spend on auctions instead of hardware to win latency races, with 97% of Timeboost proceeds going to the Arbitrum DAO. Timeboost is annualizing over $3M of fees for the Arbitrum DAO, per its March 2026 figures, according to data from Entropy Advisors, generating around 26% of total DAO income. However, considering it has generated $7M of fees within its first year, it is possible the lower run rate reflects softer crypto activity more broadly.

Arbitrum, which has the 8th largest treasury across crypto projects, per DeFi Llama, also engages in active treasury management to generate income. This can include holding yield-generating assets, such as tokenized treasuries, or participating in staking or DeFi. 20% of Arbitrum’s revenue in February 2026 came from treasury management, increasing from approximately 5% in October 2024. Arbitrum stands out amongst many projects in that all protocol upgrades and all spending of the treasury is fully controlled by ARB token holders, underscoring protocol revenue flows and token-related governance.

Exploring the Impact of Robinhood Chain on Arbitrum

This partnership showcases a major traditional player (HOOD, $63B market cap as of April 1, 2026) ramping up on-chain activities. It is a significant vote of confidence in the Arbitrum tech stack, but especially when considering the size of Robinhood’s activities and the potential scale it may require on-chain.

Key technical specifications of Robinhood Chain include 100ms block times, validating the ultra-low latency and app-specific efficiency requirements Vitalik mentions (this is faster than L1s such as Solana at 400ms).

For this arrangement, the Arbitrum ecosystem receives back 10% of net protocol revenue (80/20 DAO/Developer Guild split) because Robinhood Chain settles on the Ethereum L1, not Arbitrum One. Net revenue here is effectively sequencer profit (gas fees less Ethereum settlement fees).

Robinhood Chain and other Arbitrum Chains stand to drive incremental indirect activity to the Arbitrum L2 itself through cross-chain launches and swaps, bridging, and spillover activity. However, it is also possible such chains cannibalize activity on the Arbitrum L2.

The clear use case for Robinhood Chain will be tokenized stock trades, given equities are at the core of Robinhood’s business and considering that it already has rolled out tokenized stocks. DeFi could add another key source of activity (DEX activity and other DeFi interactions, such as lending against stock collateral). Stablecoin payments and movements, token transfers, and automated transactions could further drive overall activity on the chain. It is possible Robinhood Chain could unlock widespread use of RWA in DeFi, something we have not seen at scale yet, outside of stablecoins. However, this may be contingent on further regulatory clarity in the U.S.

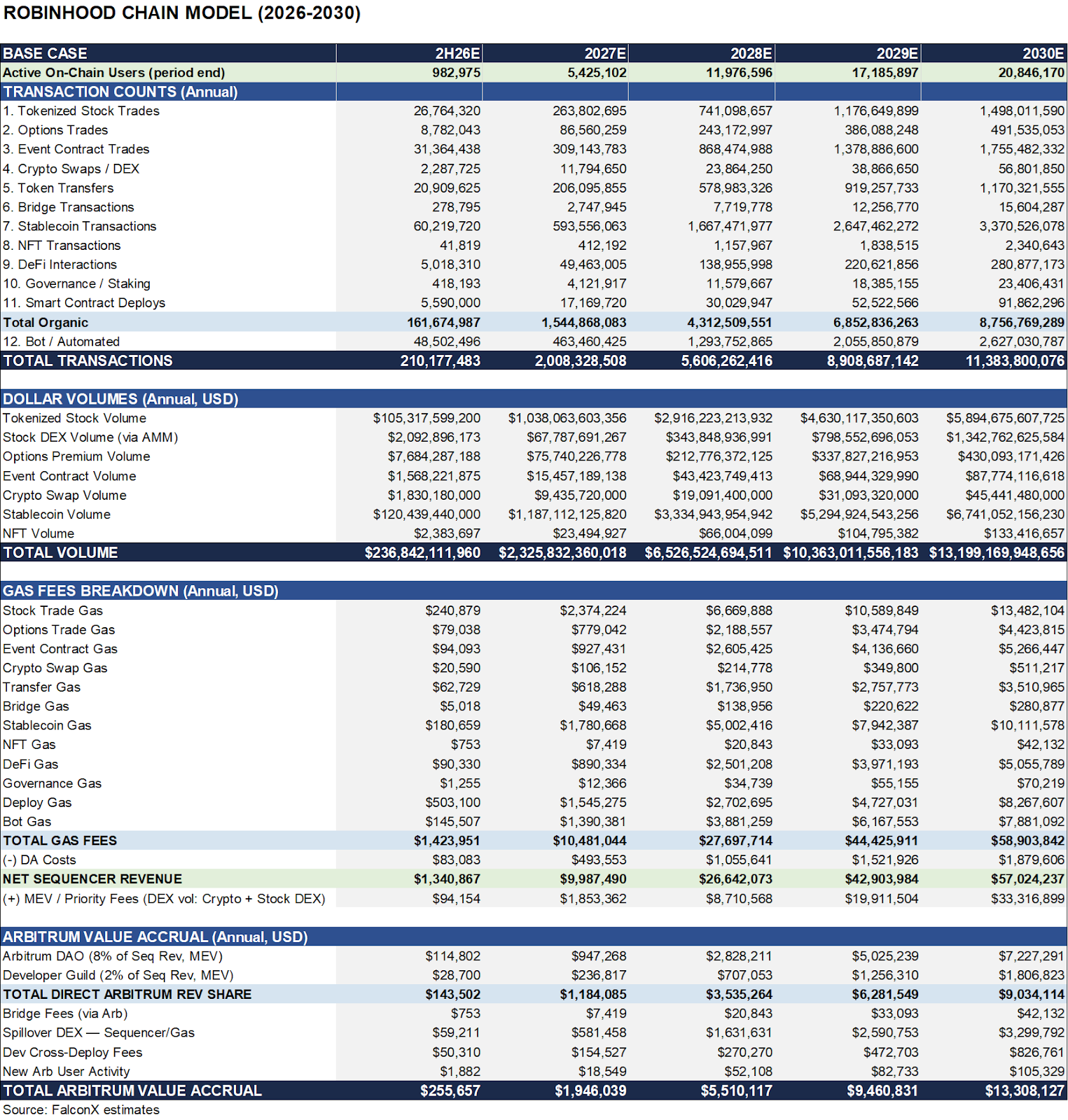

Using Robinhood’s reported February figures as a baseline, we modeled out the potential impacts of Robinhood Chain. Our key assumptions include the following:

Adoption Ramp. We assume Robinhood Chain launches mainnet in 3Q26, starting at 3% of MAU and growing to 100% of users by the end of 2030. We believe that Robinhood could ultimately transition all activity to use its chain, primarily for settlement. Robinhood Chain will likely be on the backend of its app and interface, meaning Robinhood users may not even know they are using blockchain tech for their brokerage activities.

Transaction Mix. Tokenized stock trades, stablecoin transfers and settlements, and options and event contract trading stands to be key drivers of on-chain activity. Typical L2 activity, such as DeFi, crypto-crypto swaps, and automated transactions fill the remainder.

Off-chain vs. On-Chain Trading Share. We anticipate that Robinhood Chain will be used primarily for settlement. This means trades will get matched off-chain and settled on-chain. We estimate only a portion of tokenized activity will end up trading in DeFi (up to 25% over time, compared to the current DEX/CEX volume ratio of 15%), as Robinhood will likely want to retain much of its current model while adopting blockchain efficiencies.

MEV. We assume Robinhood Chain adopts Arbitrum’s Timeboost for MEV on its chain, which could become a major revenue driver over time and relies heavily on DeFi activity on the chain, rather than settlement activity. Per the Arbitrum team, Arbitrum would receive its 10% revenue share from Robinhood Chain MEV if Timeboost is adopted there.

Our base-case scenario for Robinhood Chain estimates annual gas fees could approach $60M by 2030. Key to our projections is that users will move to engage with other apps on the L2 more broadly, such as DeFi, driving incremental transaction activity apart from just trading tokenized stocks. This could translate to as much as $7M and $2M to the Arbitrum DAO and Arbitrum Developer Guild, respectively, as well as an incremental $4M in fees from spillover activity to the Arbitrum L2 itself, driving approximately $13M/yr in total to the Arbitrum ecosystem by 2030. Such a scenario would be meaningful considering run-rate annualized Arbitrum DAO income of $12M as of March 2026, per Entropy Advisors. And this is just one chain – if additional chains adopt the stack, aggregate fee flows could change; the magnitude is uncertain.

Relative Metrics (Illustrative)

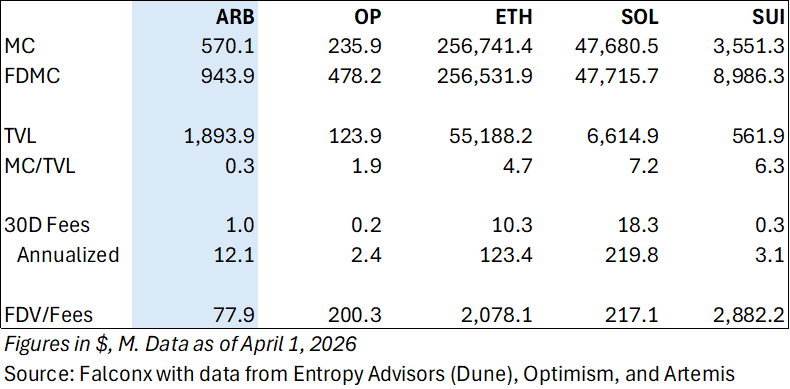

At current levels, ARB is trading at a lower revenue multiple (FDV/Fees) relative to leading L1s. SOL, for example, trades at nearly 3X ARB’s FDV/Fees multiple. Pertaining to its core L2, it trades the cheapest of this peer set on a MC/TVL basis, per data from Artemis.

Perhaps the clearest takeaway is that compared to L2s, major L1s trade at significant premiums relative to their current activity and revenue generation, despite functionally delivering a similar offering. However, the increasing convergence of traditional industries onto blockchain tech often supports separate chains for greater control and customizability, which could favor L2s such as Arbitrum which offer blockchains as a service. L1s do not have a fixed revenue share mechanism for their tech stack, unlike Arbitrum.

Conclusion

Based on how Arbitrum trades relative to its peerset, the market may be discounting the incremental revenue potential of Arbitrum Chain fees, which could improve revenue generation considerably from a recent run rate of $12M. On a relative basis, investors can pay “less” for L2s but still get exposure to growth in blockchain activity. If our estimates for Robinhood Chain activity prove accurate and ARB’s valuation stays the same, it could ultimately trade below a multiple of 40X FDV/Fees, which is comparable to today’s leaders on the app side, such as HYPE. Of course, this is just theory until Arbitrum’s partner blockchains see traction (so far Robinhood’s testnet saw 4M transactions in its first week). The future of L2s like Arbitrum will ultimately depend on the success of these enterprise blockchains.

It’s worth considering the parallels Arbitrum’s model has to that of Amazon, whose AWS offering supported growing demand for cloud needs. Just as AWS provided the scalable and reliable infrastructure that allowed businesses to build and deploy applications without managing their own servers, Arbitrum offers a similar value proposition for the blockchain industry by abstracting away the complexity and high costs of maintaining the tech stack so that developers can focus on building real applications. By lowering barriers to entry, AWS accelerated cloud adoption. Arbitrum could play a similar role in onboarding the next wave of enterprises to blockchains, although this vertical is highly competitive. Much like the years it took for the AWS vision to play out, the market may be underestimating the long-term value of owning the infrastructure layer of an emerging blockchain ecosystem.

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd., nor Banzai Pipeline Limited service retail customers, and the information on this website is NOT intended for them. The material published on this website is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this website is not and should not be regarded as investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

No discussion of a particular company or product shall be considered an endorsement of such company or product. Past performance is not indicative of future results. FalconX, and its affiliated parties, including 21shares, may hold positions in, act as a market maker for, or otherwise have a financial interest in, assets discussed herein, and may benefit from any price movements or transactions involving the subject company. This may change without notice. Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory, and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over-the-counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a swap dealer with the U.S. Commodities Futures Trading Commission (CFTC) and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is licensed by the MFSA as a Class 2 Crypto-Asset Service Provider (Regulation (EU) 2023/1114). It is also licensed as a Financial Institution (Cap. 376) exclusively for EMT payment services. FalconX’s complaint policy can be accessed by sending a request to complaints@falconx.io

"FalconX" is a marketing name for the FalconX Group and its affiliates. Availability of products and services can be subjected to jurisdictional restrictions and operational capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.