The 3 DEPIN Protocols Seeing Record Activity

In a period when many crypto apps are seeing declining metrics, several DEPIN projects stand out for growing adoption that has translated into record token burns. While crypto activity is often cyclical, DEPIN is tied to off-chain uses, making traction more insulated from market swings.

Helium (HNT)

Decentralized wireless network Helium is seeing increasing adoption. Helium Mobile DAUs climbed to as much as 2.5M in late December 2025, increasing ~10X from a year ago. This has been driven largely by Helium Mobile sign ups as well as carrier offloading arrangements. Helium Mobile sign ups grew to nearly 600K at year end, climbing roughly 5X in the year. Sign ups accelerated from April onward, in part on new partnerships and its freemium plan introduced in Q1. This also coincided with the resolution of the SEC’s lawsuit against Nova Labs, the core contributor of the Helium Network.

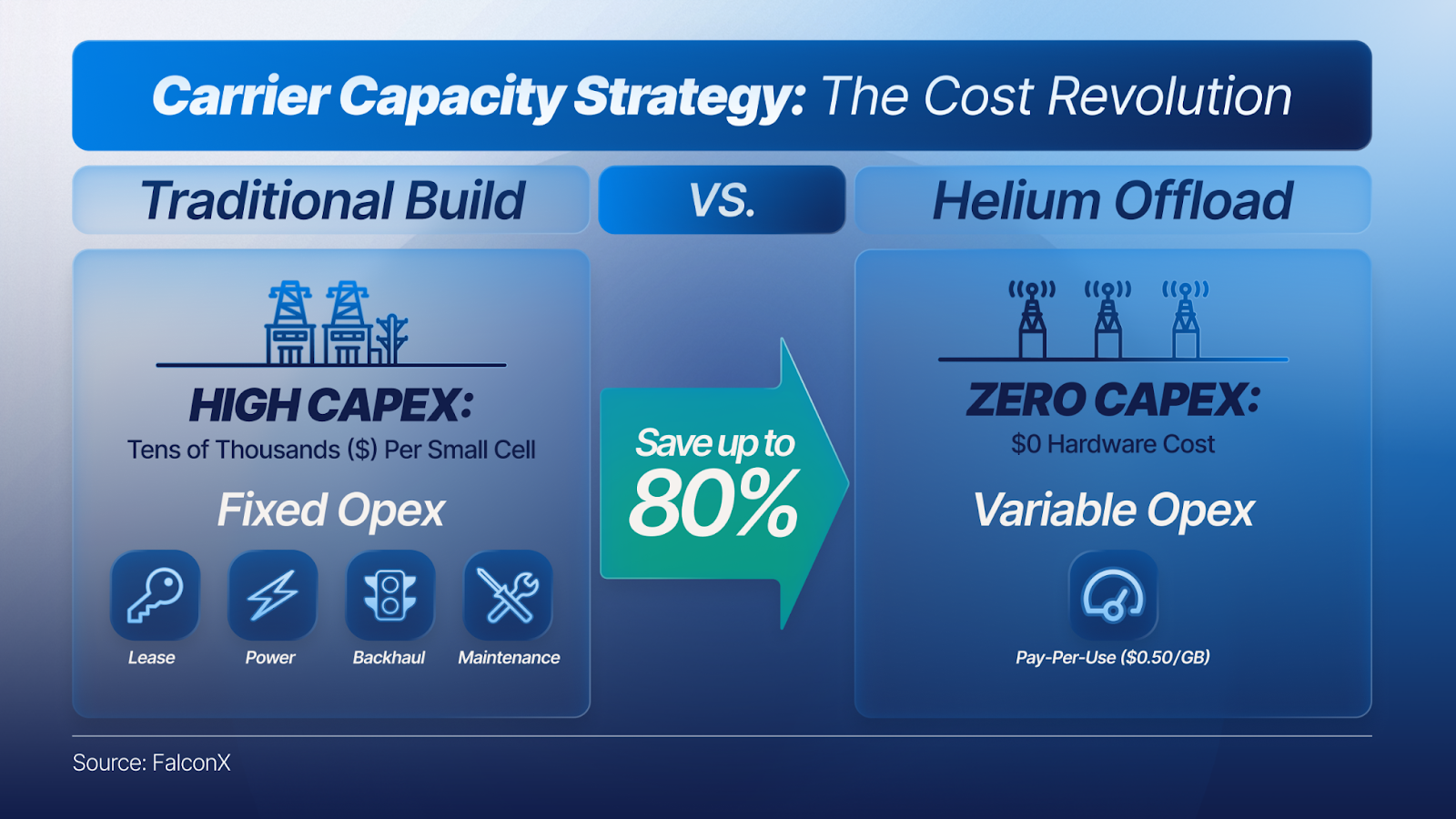

For data offloading, Helium’s growth has been driven by partnerships with Telefonica/Movistar in Mexico and AT&T in the U.S.. It now counts 7 carriers that are able to connect and transfer data through its hotspots. When subscribers to these carriers pass through an area covered by the Helium Network, their data is transferred over to Helium nodes for improved coverage, especially useful for dense/indoor areas that 5G signal may have difficulty penetrating. For carriers leveraging Helium, this offers significant cost savings (Helium can be up to 80% cheaper than traditional roaming charges, and eliminates the need for high upfront capex to build out coverage on their own). Helium’s daily data transferred increased over 150% in 2H25 alone, outpacing DAU growth of 113% over the same period, highlighting expansion in carrier offloading.

Growing user demand is just part of the picture. To help expand its network coverage, Helium rolled out its Helium Plus offering in July 2025, which enables businesses and public Wi-Fi providers to connect their existing routers onto the Helium Network via software. This is a significant unlock as new contributors to the network are no longer required to purchase specialized Helium devices to participate and add coverage to the network. This leads to a more streamlined process to grow the network, expands the potential userbase, and helps eliminate supply chain bottlenecks to expanding the network (previously production and delivery of Helium hardware were a potential constraint).

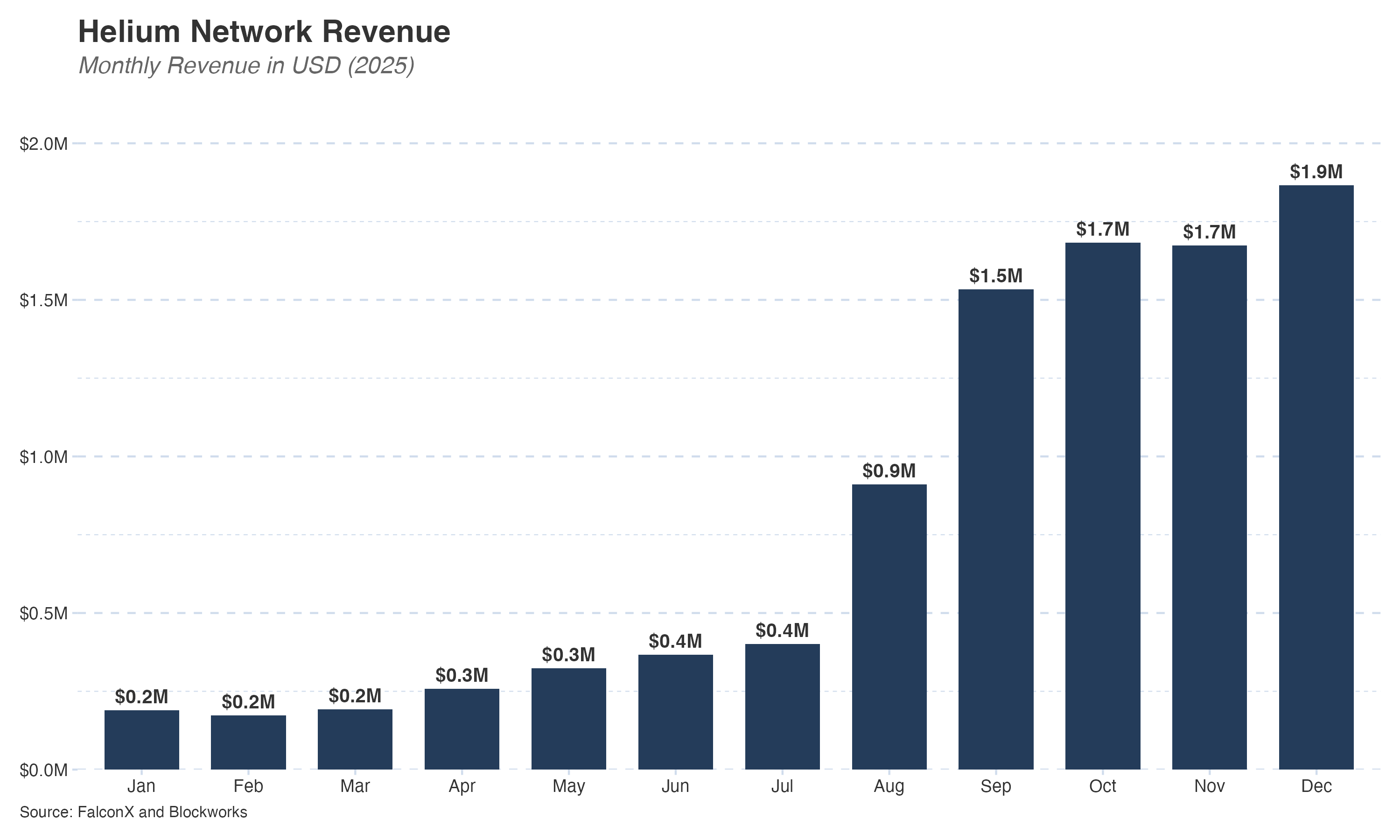

Helium’s tokenomics leverages a Burn and Mint Equilibrium (BME) model. Customers (ex: carriers) pay in fiat which are used to buy and burn data credits, which are priced in HNT, causing buying pressure on HNT. Network revenue across Helium Mobile and carrier offload is annualized at $35M, per Blockworks, but Helium Mobile revenue largely accrues to Nova Labs. Moreover, HNT has been deflationary in recent weeks, and comes after HNT’s halving occurred in August, helping support more constructive supply dynamics.

To better align Mobile traction with tokenholders, Nova Labs began HNT buybacks with Mobile subscriber revenue in October 2025. However, citing a lack of market response to the buybacks, Helium’s Founder and CEO of Nova Labs Amir Haleem announced in early Jan 2026 that they will pause discretionary HNT buybacks in favor of investing the funds back into the business. Buy and burns will continue from carrier offloads. In the announcement, Haleem mentioned Helium + Mobile generating $3.4M in October. While an impressive stat, it raises questions on how or if future revenues will flow back to tokenholders. To contextualize this, Mobile only accounted for only ~10% of data credit burns earlier in 2025, per Messari, despite its relatively substantial revenues, suggesting its direct impact on token price remains limited.

Despite lingering concerns around the token vs equity rights (Nova Labs vs HNT holders) and sustainability of the network, Helium stands out as one of the most widely used crypto applications. Looking ahead to 2026, key growth areas include expanding into new countries, driving awareness and adoption, and boosting coverage in locations with high volumes of traffic.

Hivemapper (HONEY)

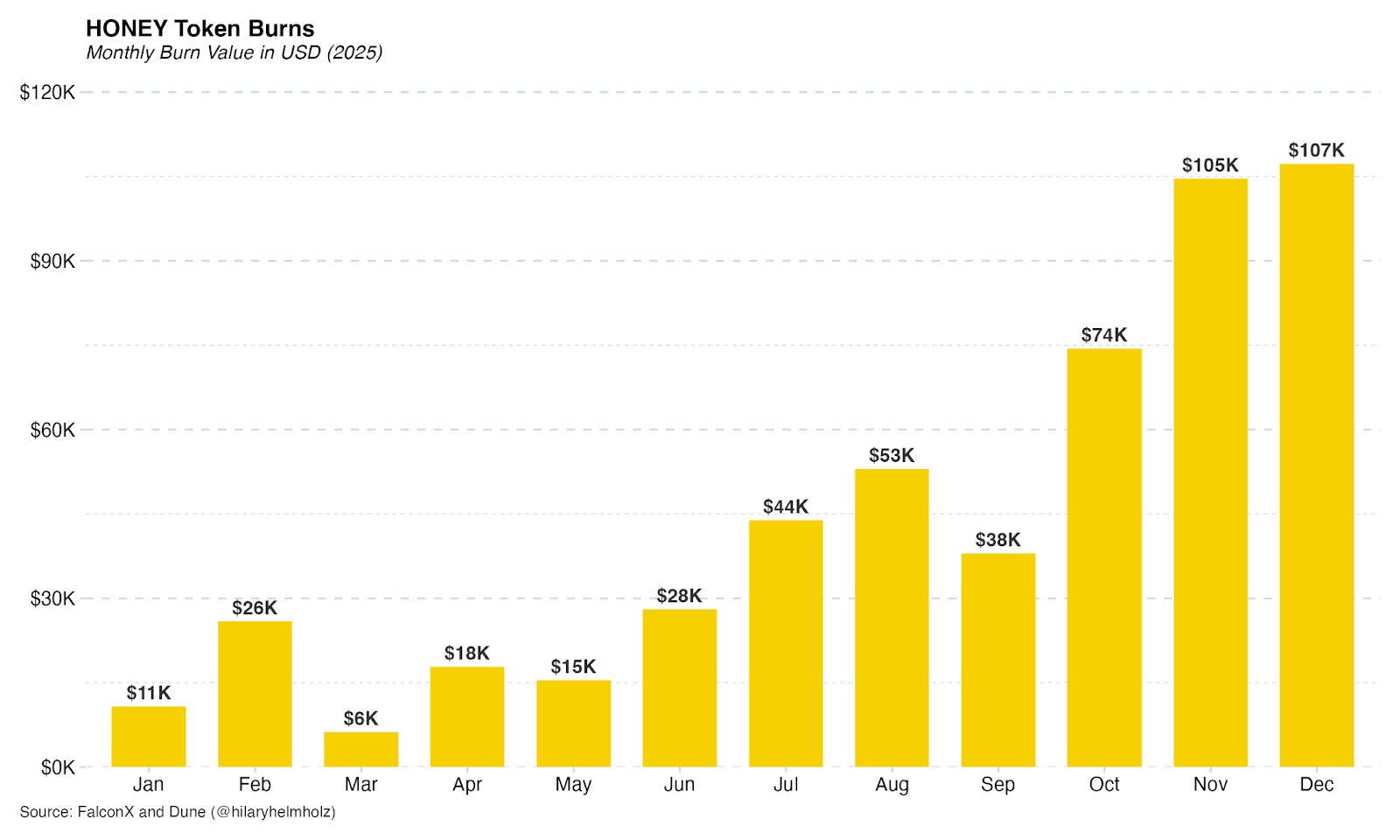

Decentralized mapping protocol Hivemapper saw record burns in token terms ($107K equivalent burned in December) and saw HONEY flip deflationary for the first time in late 2025. The trend helps its circulating supply trends, especially after team unlocks concluded in October.

Up to date road and street data is key for autonomous vehicles and logistics companies to optimize routes. Hivemapper pays users to drive around with their custom dashcams, creating a repository of fresh mapping data.

Following its October 2025 move to establish Bee Maps as a standalone entity, decentralized mapping protocol Hivemapper has seen its B2B-focused pivot translate into a sharp rise in activity. This enables enterprises to have a clear point of contact for interacting with the network; moreover Bee Maps helps convert fiat-based B2B transactions into HONEY burns.

Other drivers include its global road coverage growing to 37% as of writing (compares to ~30% a year ago), with 700M+ KM mapped globally, including 22M unique KM mapped. In Q4, Hivemapper transitioned from charging high initial costs for the cams ($589) to subscription models ($19/month for a 2-year contract), which could make it more viable for fleet operators and help improve network coverage. Such developments could bolster traction with enterprise customers, which include Volkswagen using Hivemapper data for its autonomous vehicle operations, and Lyft leveraging Hivemapper as a source of street-level data.

Geodnet (GEOD)

Geodnet is a decentralized Real-Time Kinematic (RTK) network focused on delivering precise location data to serve use cases such as robotics, drones, and surveying. 80% of its revenue goes towards a buy and burn of the GEOD token while 20% goes to the Geodnet Foundation.

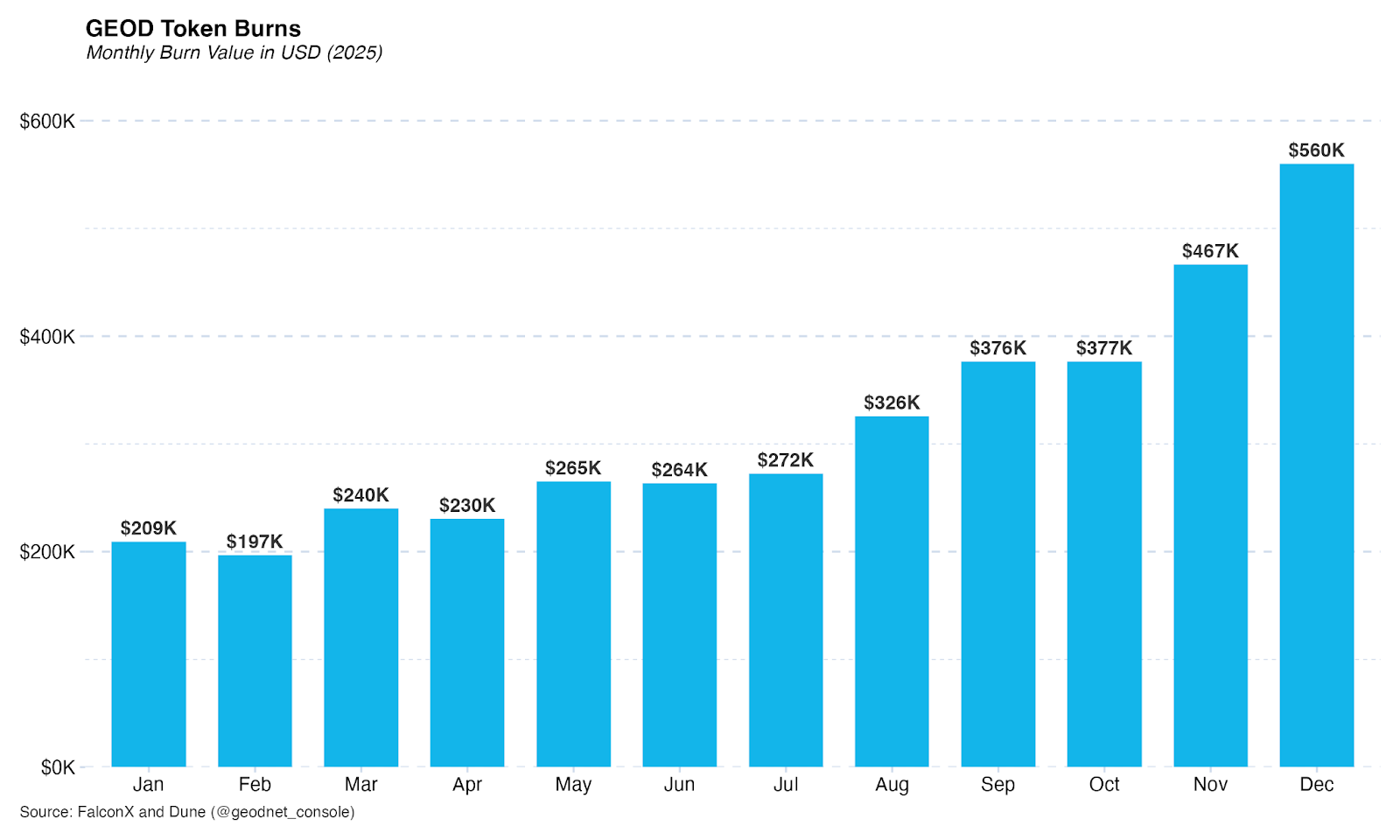

Geodnet saw token burns ramp up to hit ATHs in Q4, with burns in recent weeks offsetting around 70% of issuance, according to data from Blockworks. While Geodnet could soon be deflationary, it still has upcoming team and investor unlocks through late 2026 of $4M/month (6% of circulating supply), per Messari.

The project recently hinted at securing more major enterprise customers, implying the burn could further increase in 2026 as they pay to access data from the network. Geodnet stated it was generating $8.3M ARR as of January 2025, growing 15% from $7.2M mid-December 2025.

Conclusion

2026 could drive renewed interest in these DEPIN names as revenue from their networks scales beyond emissions. Currently, there is a divergence with the usage of these networks and their token prices, with HNT, HONEY, and GEOD down 68% on average from a year ago (Dec 2024). Their real-world use cases, enterprise customers, token value accrual, and recent traction are key differentiators amongst many altcoins in the current environment.

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd., nor Banzai Pipeline Limited (separately and collectively “FalconX”) service retail counterparties, and the information on this website is NOT intended for retail investors. The material published on this website is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this website is not and should not be regarded as investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

No discussion of a particular company or product shall be considered an endorsement of such company or product. FalconX, and its affiliated parties may hold positions in assets discussed, which may change without notice. Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory, and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over-the-counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered with the U.S. Commodities Futures Trading Commission (CFTC) as a swap dealer and a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is a registered Class 3 VFA service provider with the Malta Financial Services Authority under the Virtual Financial Assets Act of 2018. FalconX Limited is licensed to provide the following services to Experienced Investors, Execution of orders on behalf of other persons, Custodian or Nominee Services, and Dealing on own account. FalconX’s complaint policy can be accessed by sending a request to complaints@falconx.io

"FalconX" is a marketing name for FalconX Limited and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.