Pendle: One Venue, All of Fixed Income

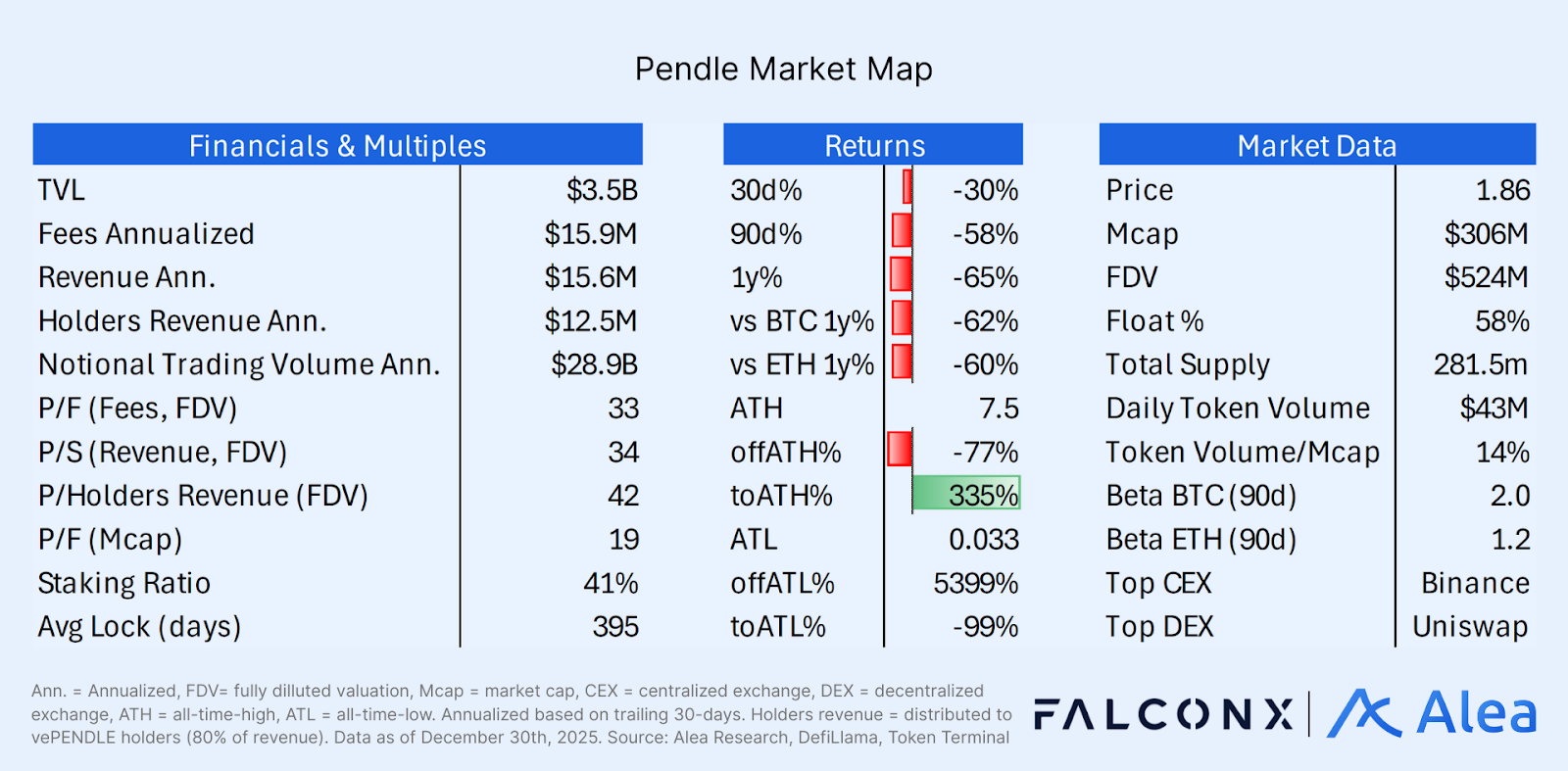

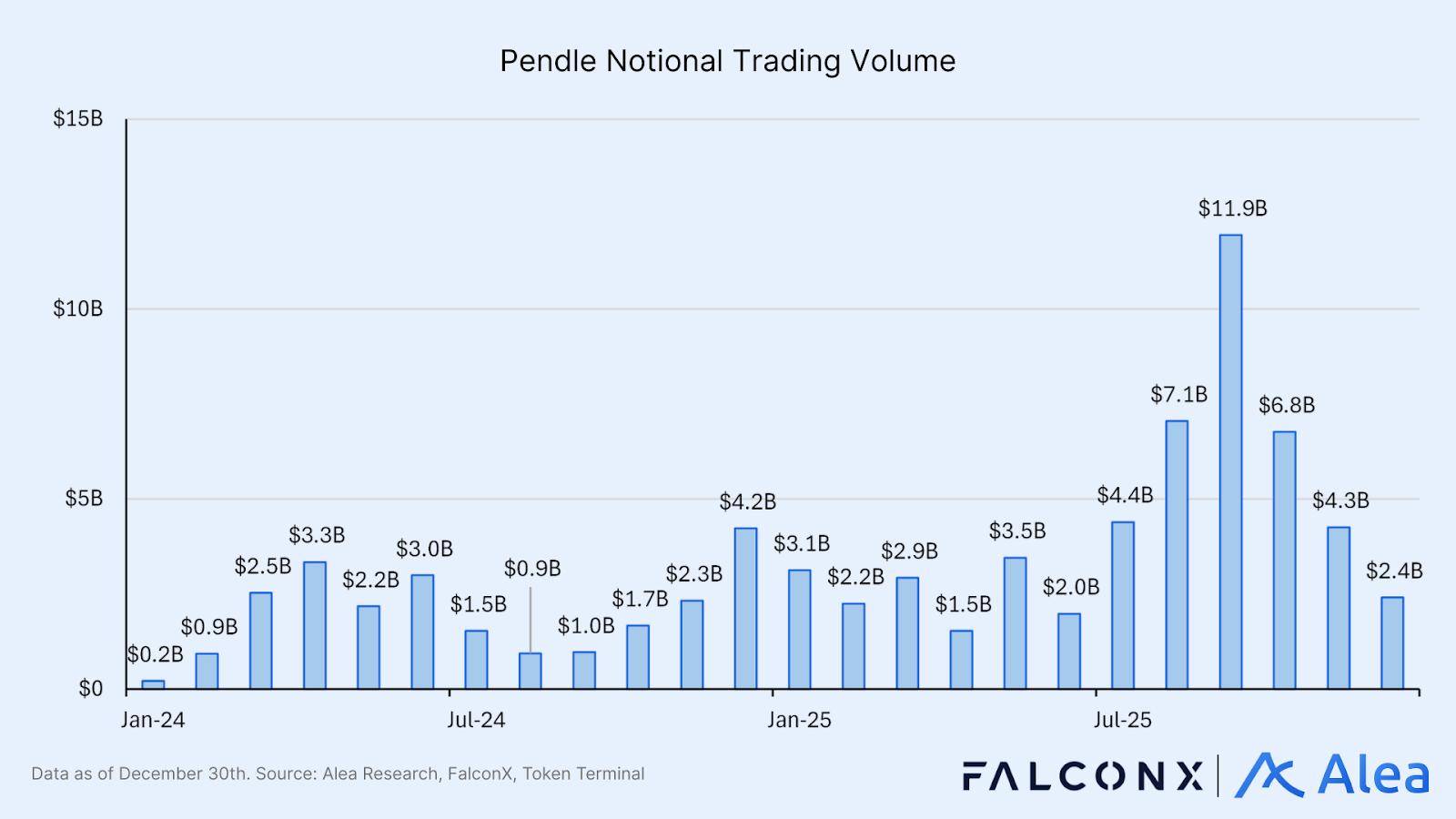

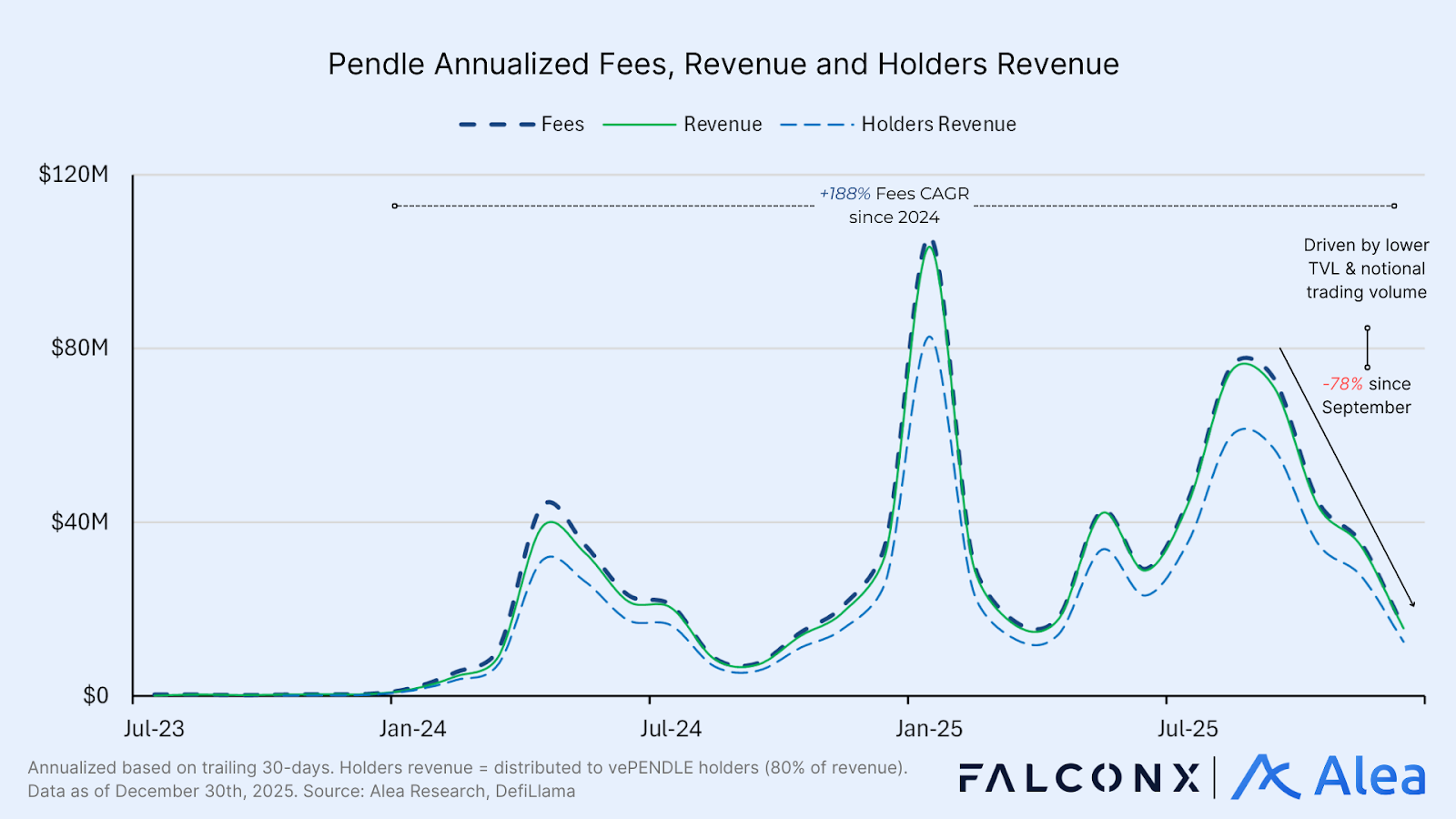

Pendle is the leading on-chain yield-trading protocol (yield stripping and interest rate swaps). TVL averaged ~$5.7B in 2025 (+76% YoY), reaching its peak at ~$13.4B; fees totaled $44.6M (+134% YoY); holders' revenue hit $34.9M (+147% YoY). Monthly notional trading volume reached $54B (trailing 90-days average) in 2025 (+63% YoY), with frequent daily nine-figure prints. Pendle concluded 2025 as a top-20 DeFi protocol by TVL, ranked 13, right after the leading spot DEX, Uniswap.

Despite its dominant position, PENDLE has trended down in 2025 (-62% YoY), underperforming both BTC and ETH by >50%. It closed 2025 under ~$2, significantly lower (~70%) from the ~$6 mid-year highs. Currently, over one‑third of circulating PENDLE sits locked in vePENDLE, with average lock durations above 395 days.

Fixed income is the largest segment of global securities by size and depth. On-chain, it barely exists. The infrastructure to price, trade, and hedge yield across asset types is still forming. Pendle already dominates the segment that does exist: DeFi yield trading. The architecture extends to any yield source with an oracle. That's the foundation for a venue sitting at the center of DeFi, CeFi, and TradFi.

Key Takeaways

Structural Discount: The vePENDLE model pushes some liquid buyers to the sidelines, since they can’t access protocol cash flows without accepting lock-up illiquidity. A move to buybacks or 2026 tokenomics changes could help address these pain points.

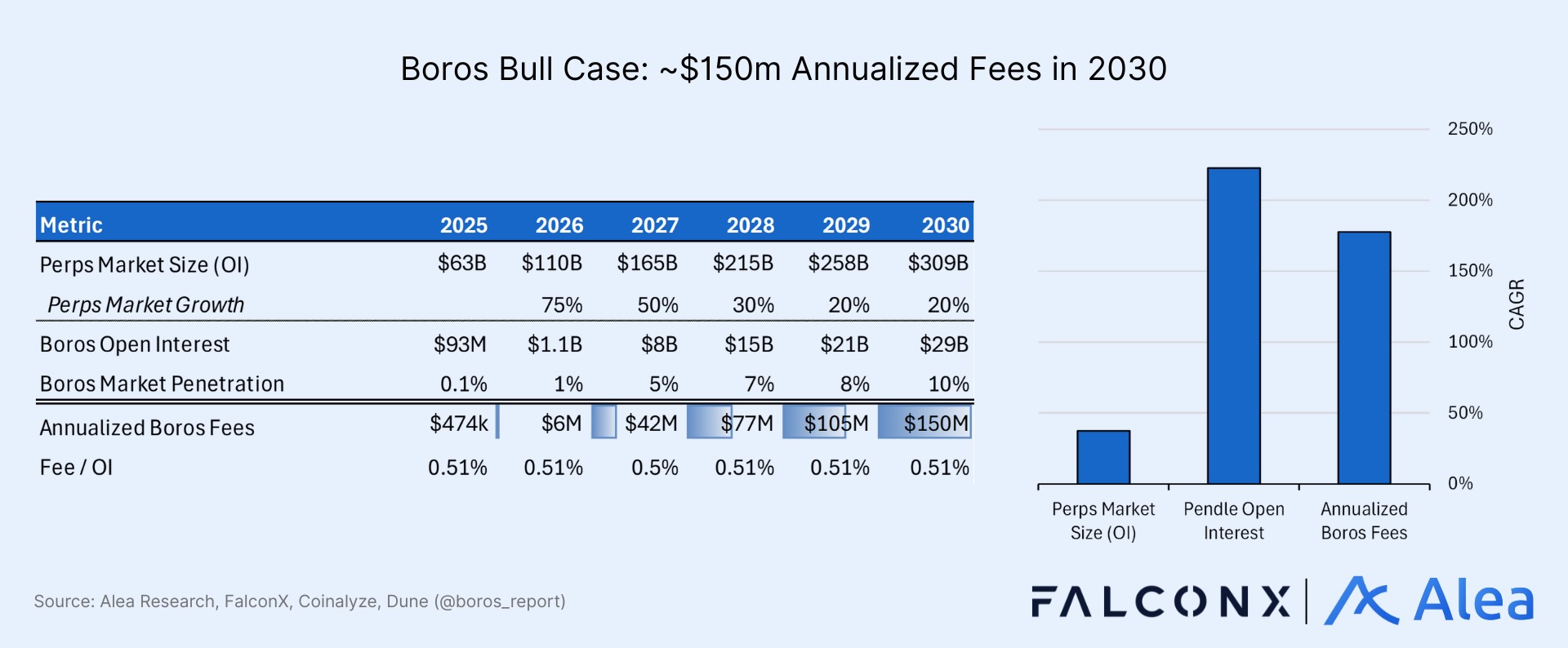

Boros Optionality: Funding-rate derivatives currently are a ~$63B perps OI market where Pendle held just ~$93M (0.1% penetration) in December. A 10x OI expansion would add roughly 15% incremental fees, per our estimates. Such revenue would remove the dependency on TVL and help Pendle manage through DeFi’s yield compression seasons.

Leading Indicators: Boros OI growth relative to the broader perps market; fees mix shift from yield-driven (TVL) to trading-driven (volume); governance proposals around buybacks or lock mechanic changes; vePENDLE staking ratio and lock duration as the clearest conviction gauges.

PENDLE Setup: PENDLE closed 2025 trading below its April lows (Trump tariffs sell-off). The market appears to be discounting earnings quality across Pendle’s two business lines (v2’s yield and swap fees, and Boros), the probability of tokenomics catalysts, and Boros as an independent growth vector.

Before the Thesis

Pendle has an unusual profile among DeFi blue chips. Unlike more obvious DeFi primitives like DEXs, lending, or stablecoins, yield derivatives were a riskier, more speculative bet on a market that didn’t yet exist in crypto. It took years of education alongside product development for the idea to stick.

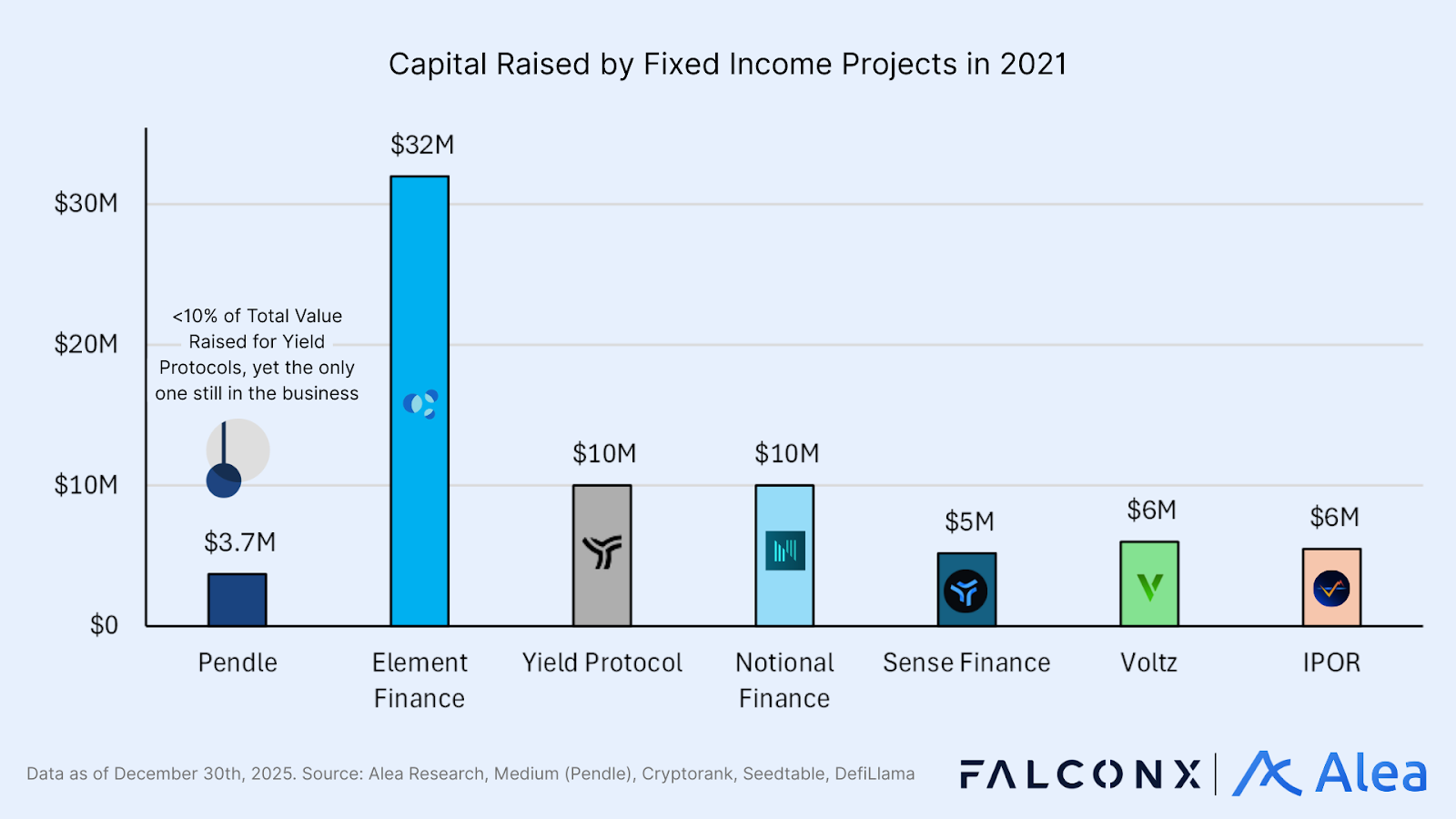

The team started building in mid-2020, and shipped V1 in 2021 on a ~$3.7M seed round. That same year, Element Finance closed $32M backed by Polychain and a16z (and a long list of DeFi founders), Yield Protocol raised $10M led by Paradigm, Notional Finance another $10M. Those weren’t the only players building the rails for fixed income on-chain. It was also Sense Finance, APWine (now Spectra), Timeless Finance, Voltz, IPOR, and more. Notional and IPOR slightly pivoted; Spectra rebranded; all others wound down.

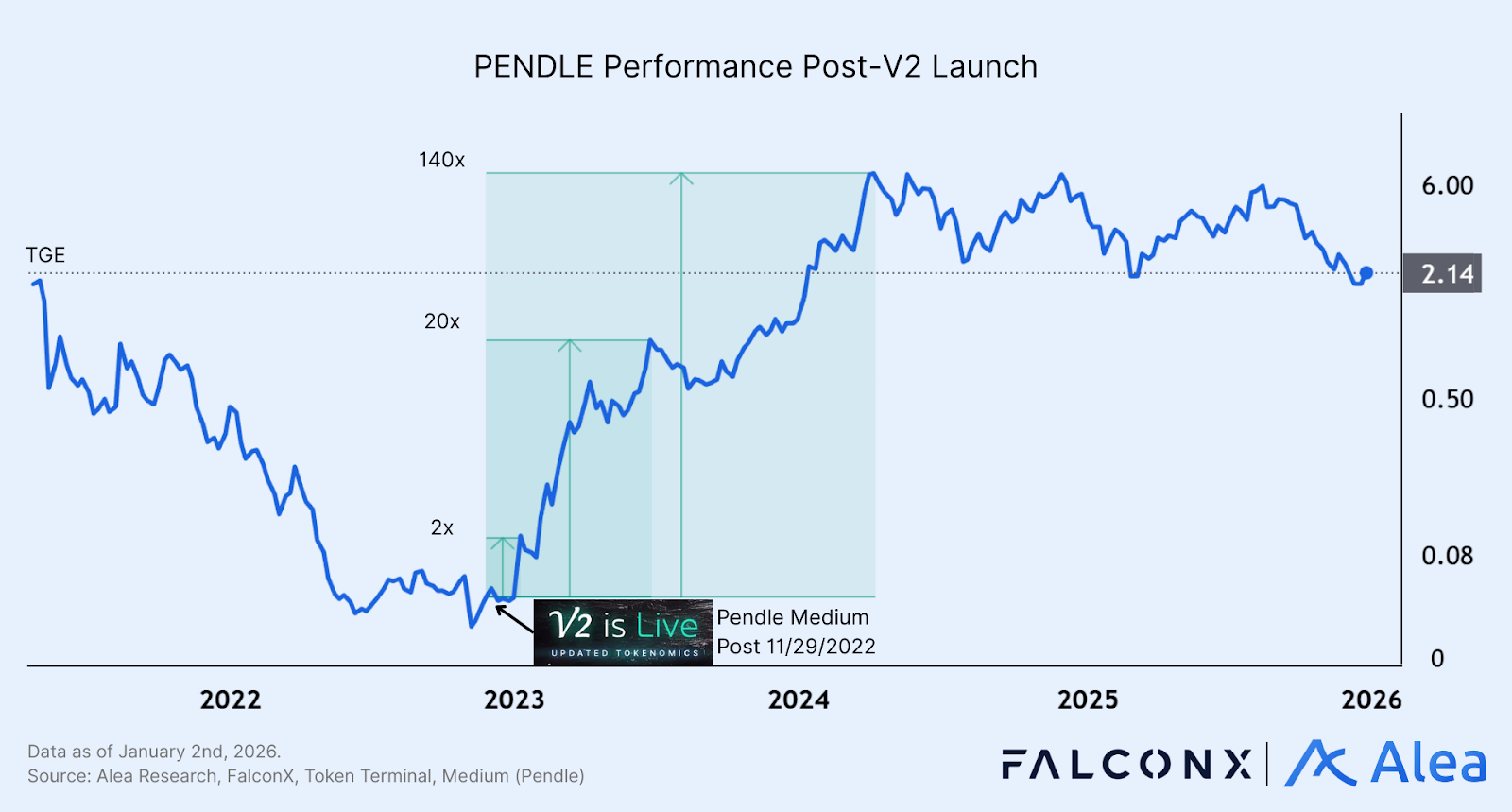

Pendle v2 unified PT/YT trading with StandardizedYield (SY) wrappers, fixing v1’s fragmentation. The upgrade paved the way for product-market-fit, supporting the creation of yield trading markets for any yield-bearing asset. To markets it was overnight; to the team and investors it was years.

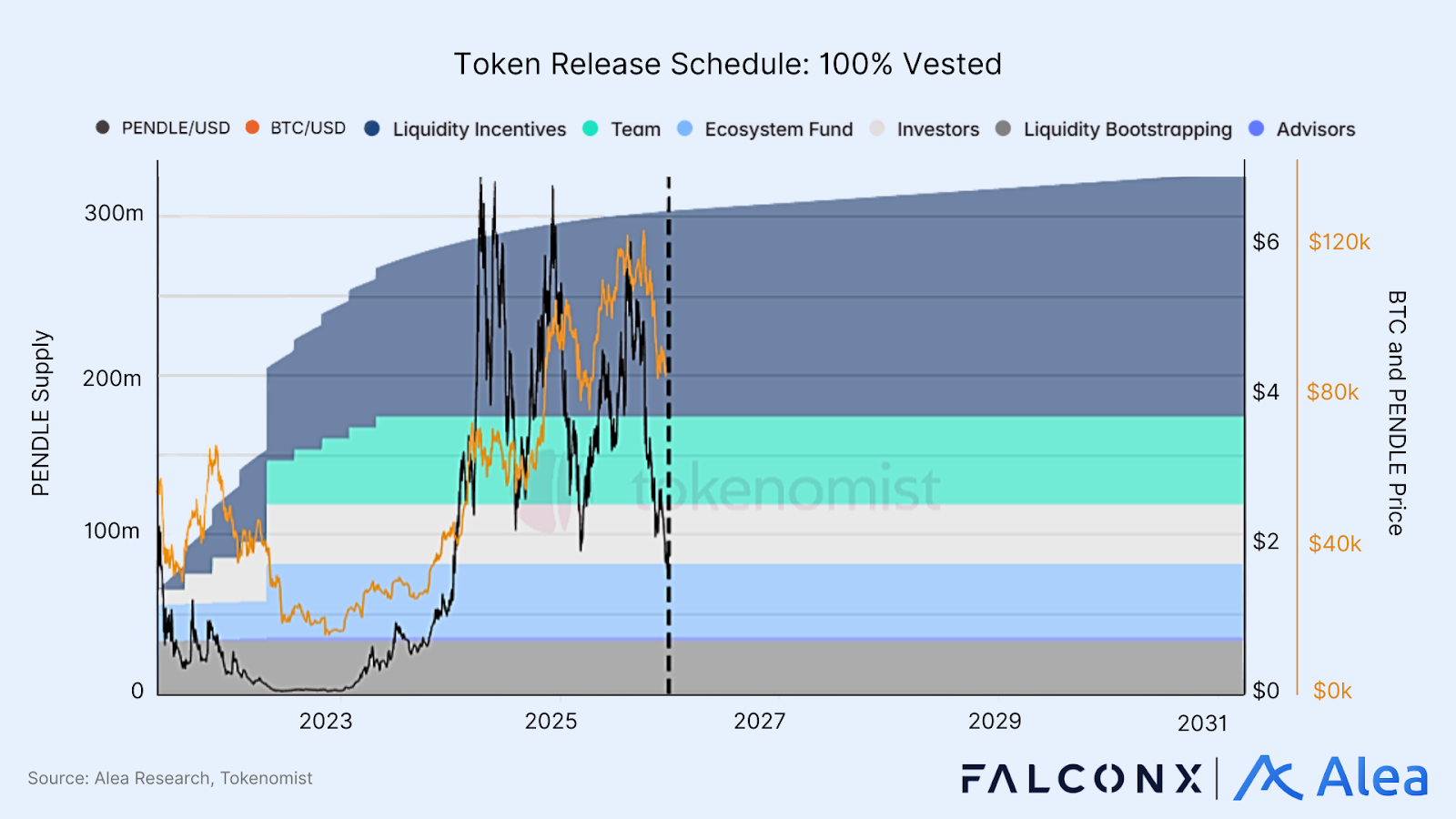

Pendle, operating on a fraction of the funding, became the market leader in 2023. It raised a follow‑on strategic round with Spartan Capital and Binance Labs (now YZi Labs) on the cap table, culminating in a Binance listing. 2025 closed with ~164.86M PENDLE in circulation, ~67.68M locked in vePENDLE (illiquid), and ~49M outside “circulating + ve-locked.” With team and investors vesting schedules complete by September 2024, the remaining corresponds to ongoing incentive emissions.

What is Pendle?

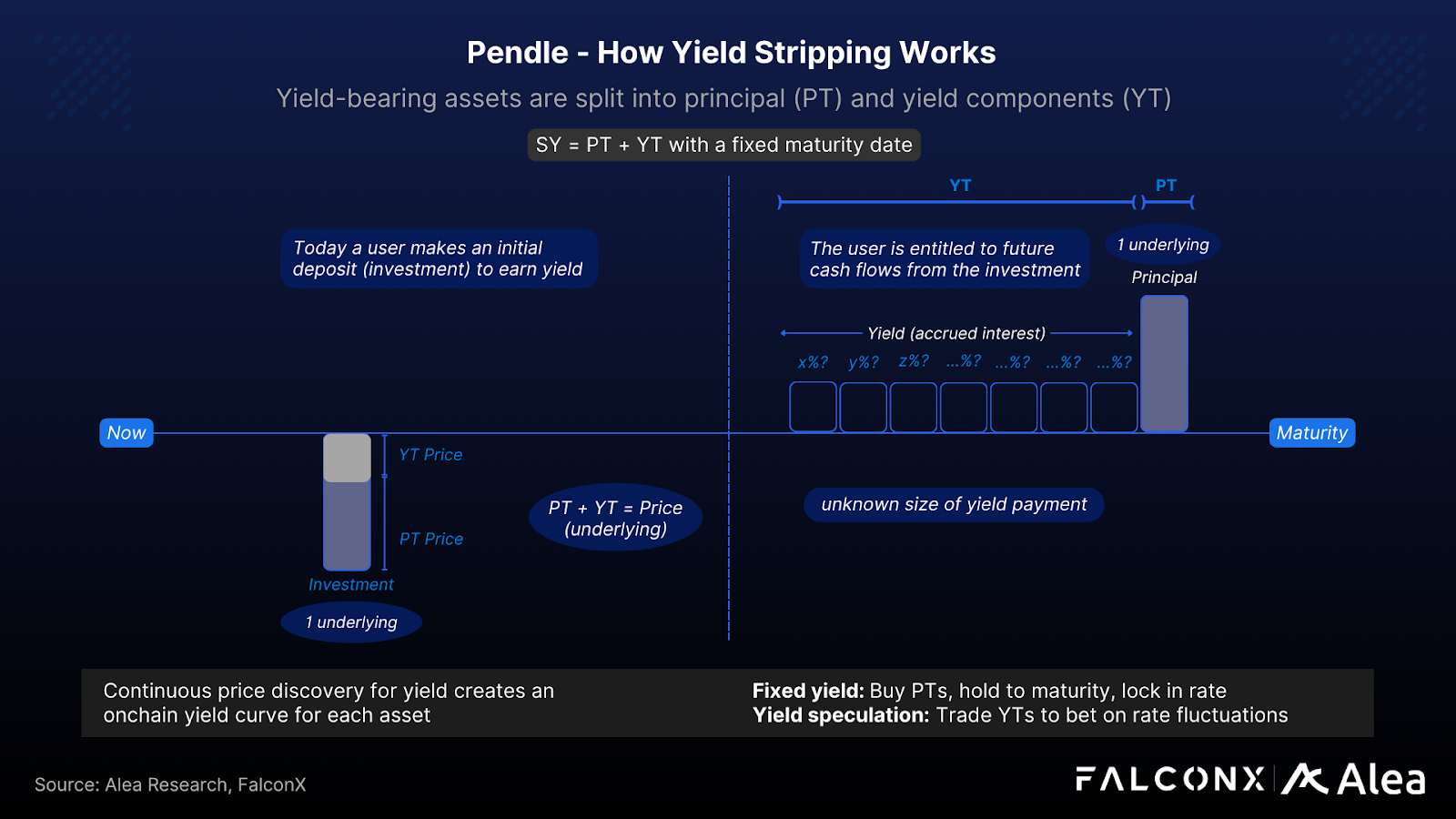

Pendle is the largest and most dominant on-chain venue for yield trading. Closer to bond stripping than to TradFi’s interest rate swaps (IRS), it splits yield-bearing assets into principal (PT) and yield (YT) constituents, then lets markets price and trade implied yields across maturities using a time-aware AMM and limit orderbook. By making DeFi’s variable yield tradable (fixed for floating and vice-versa), it enables hedging, directional rate bets, arbitrage, and yield curve formation.

Pendle won despite using a funded fixed-income structure (similar to cash securities or bond stripping), where rate exposure requires deploying the principal upfront (unlike TradFi’s vanilla interest rate swaps, which deliver the same exposure via margin and cash-flow exchanges). This explains what kind of market DeFi actually is versus what TradFi rates markets are. Because DeFi’s dominant rate demand was not duration hedging against benchmark curves, but trading incentives and yield dispersion across assets, venues, and maturities, Pendle succeeded by packaging yield itself as a tradable asset.

While others built for a theoretically efficient rates market—where yields converge across protocols and chains—Pendle built for the one that actually existed. Yield Tokens (YTs) became the delivery mechanism for incentives and points, while Principal Tokens (PTs) functioned as zero-coupon collateral inside lending markets.

This allowed Pendle to tap into a broader user base: institutional players gravitated to PTs for fixed income exposure, while retail traders expressed directional yield views through YTs. This allowed Pendle to stay adaptable and remain relevant across cycles, successfully riding diverse narratives ranging from liquid staking, points, RWAs, or yield-bearing stablecoins.

Assets issuers pursue Pendle listings in the same vein as Binance or Coinbase listings for their governance tokens. Pendle gains volume and TVL from each market; issuers gain distribution, additional utility, and more strategy diversity for their assets. Users can exchange preferences in a positive-sum way as well: YT buyers take leveraged exposure to variable yield sources; PT buyers lock in fixed rates.

Yield tokenization exhibits winner-takes-all dynamics. The moat is not code but distribution and integration density: deep liquidity across maturities, and integrations in lending markets (PTs allowed as collateral). With v2 now holding a defensible position (no close competitor within its market sector), Pendle’s next growth leg is Boros.

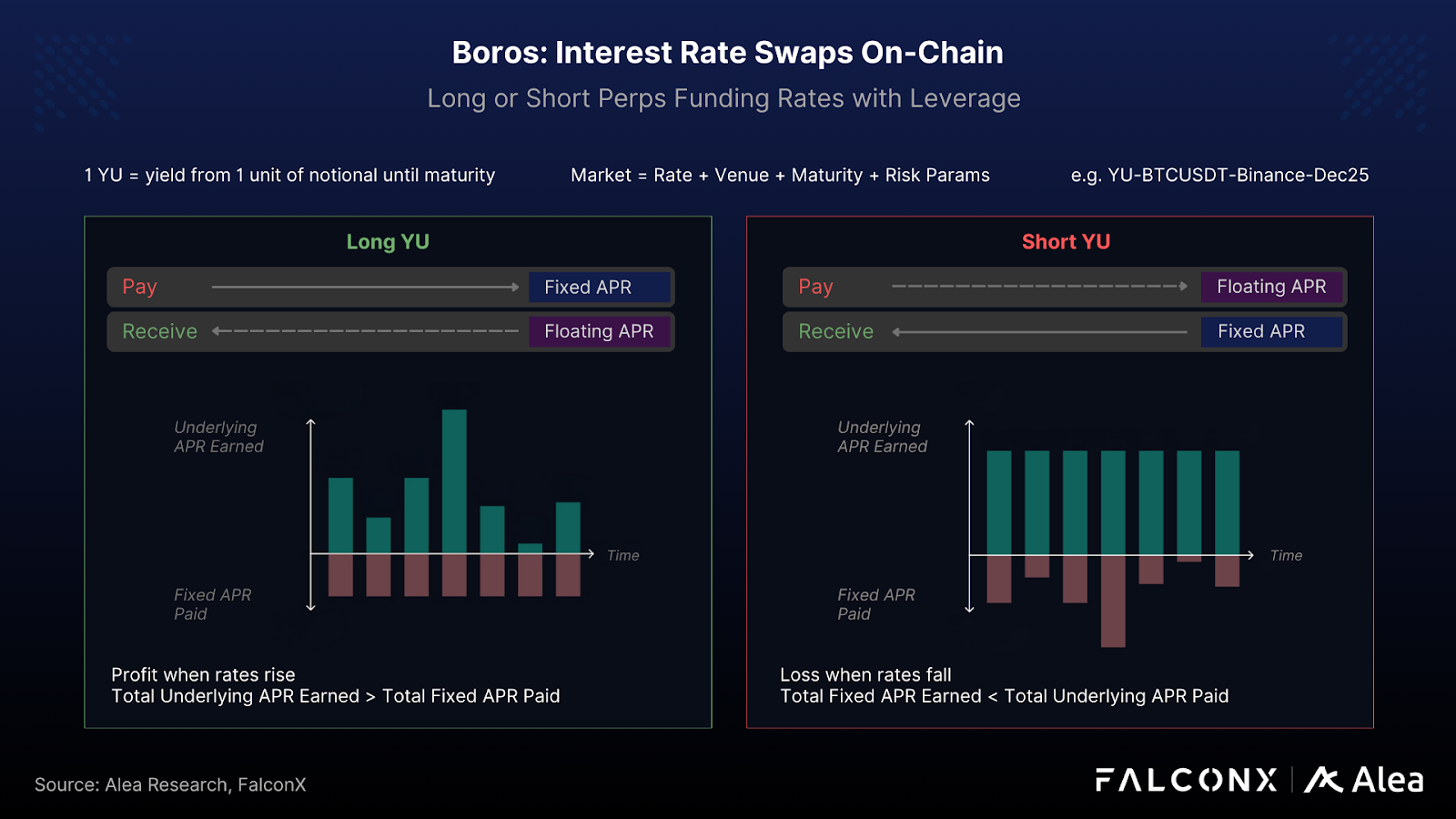

Boros

Launched separately from the core protocol, instead of tokenizing underlying yield, Boros trades funding rates (the variable cost of carrying leverage on perps). Functionally, Boros applies the same logic: make an unhedgeable variable rate tradable.

Perps dominate trading volume in crypto, with on-chain venues increasingly competing with CEXs as custody and KYC frictions fall and perps expand beyond crypto into equities and commodities. At the same time, structured products and synthetic stablecoins have made funding rates one of the largest and most volatile yield flows.

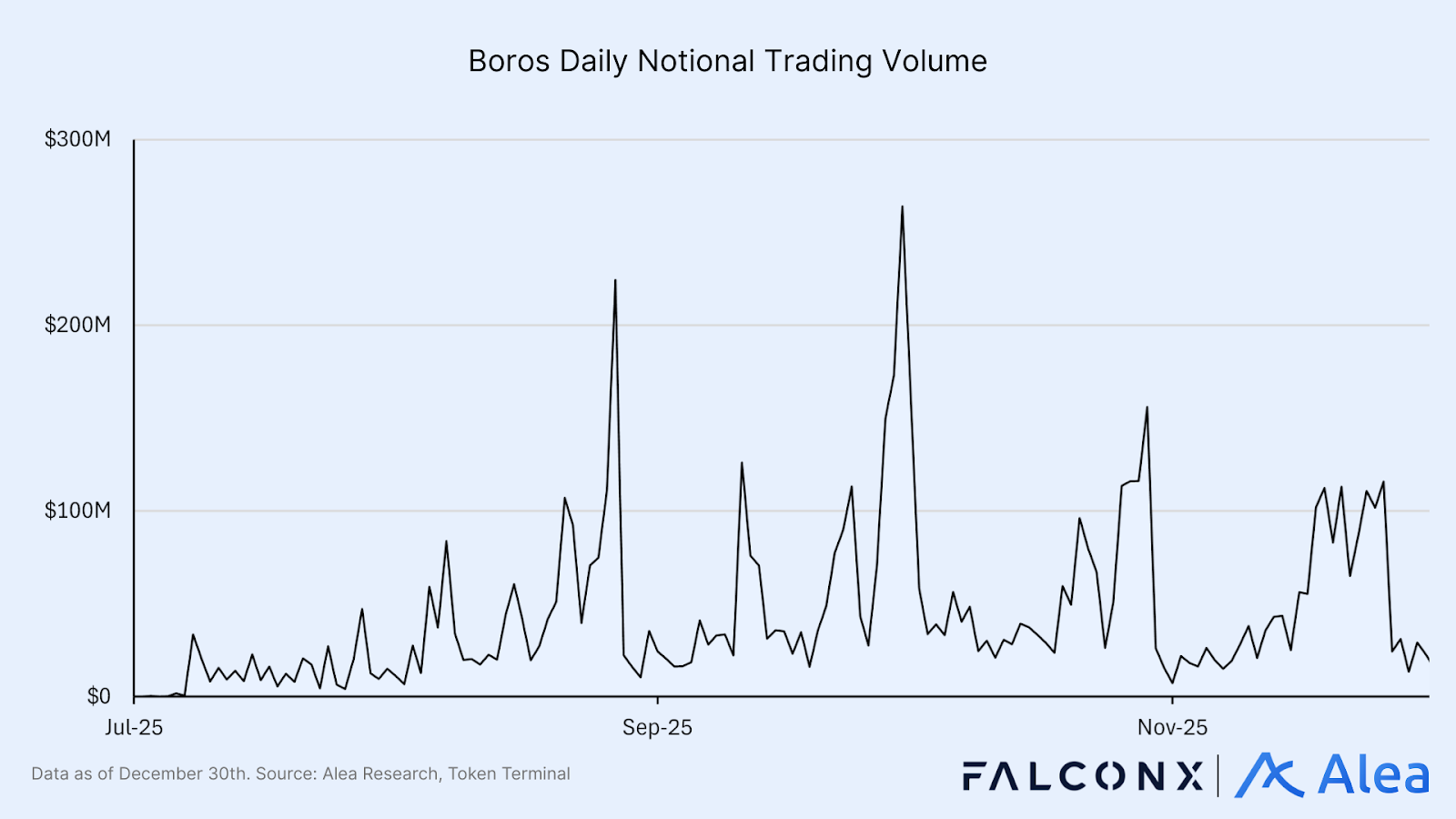

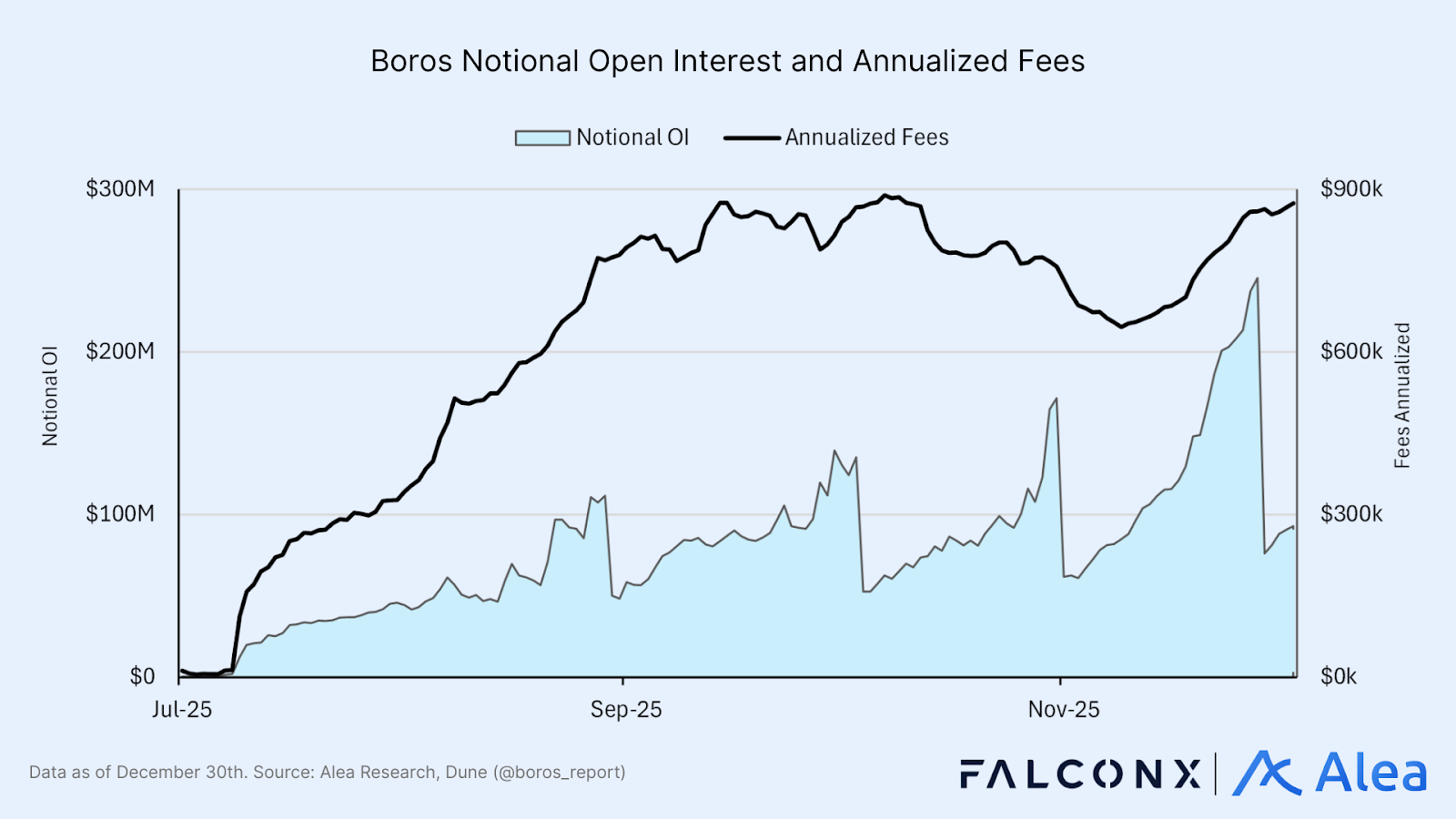

Boros is the first protocol to bring an instrument for hedging or betting on funding rates on-chain. Despite launching in a relatively quiet market, Boros has generated $301K in all-time fees across $6.9B notional volume since August 2025. Open interest sits at ~$91M with $6.8M in deposits as of December 30, 2025.

Perps evolved from a speculative instrument into core infrastructure; rate derivatives are similar but target a vastly larger market. Fixed-income markets already dwarf equities, FX, and crypto, and even a small on-chain migration would eclipse today’s spot markets. Apart from perps funding rates, Boros’ architecture supports any fixed-to-floating exchange rate with an oracle. From on-chain lending and staking rates to mortgages or TradFi benchmarks, the ambition is to support any rate, any maturity, and any venue.

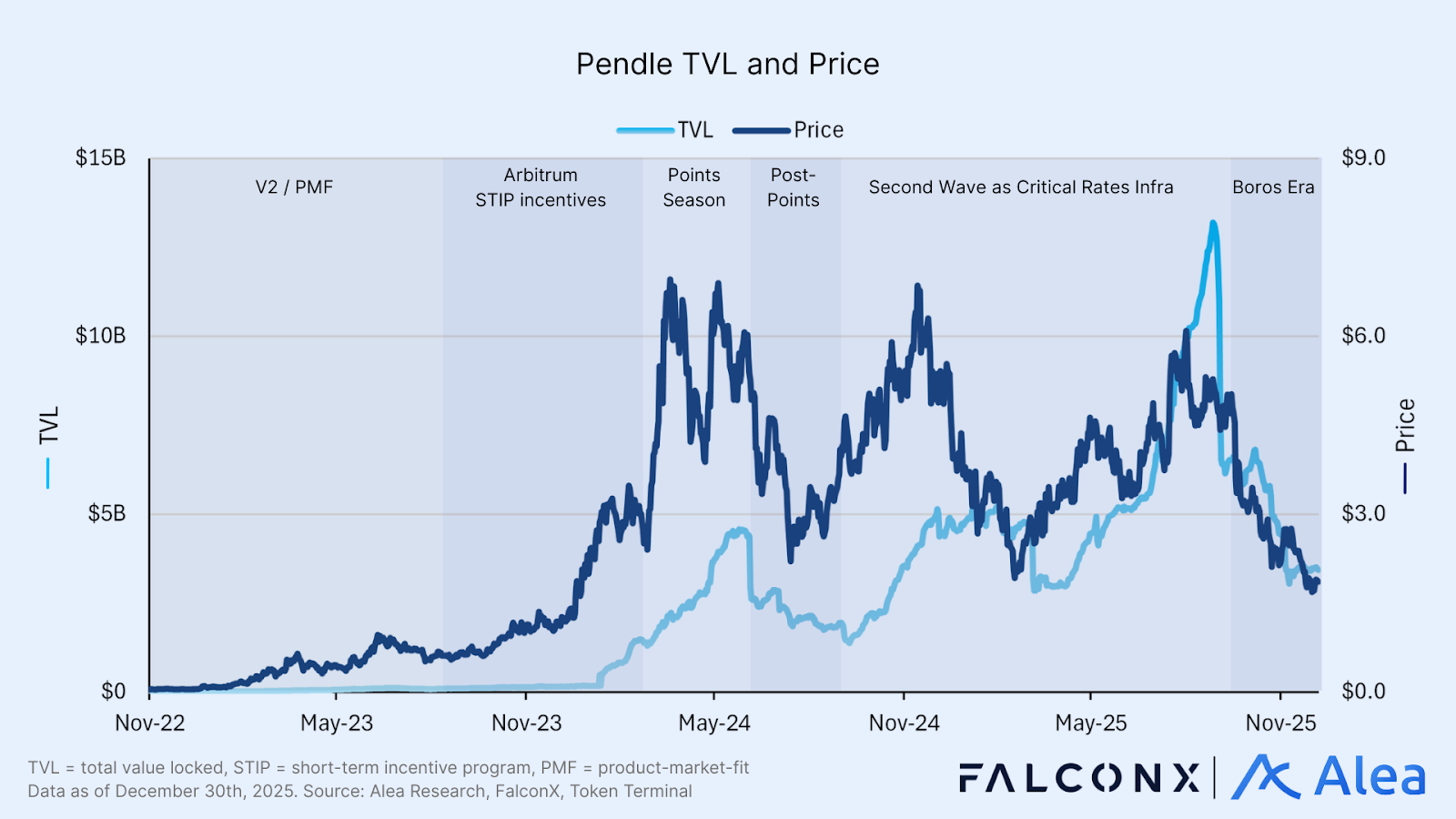

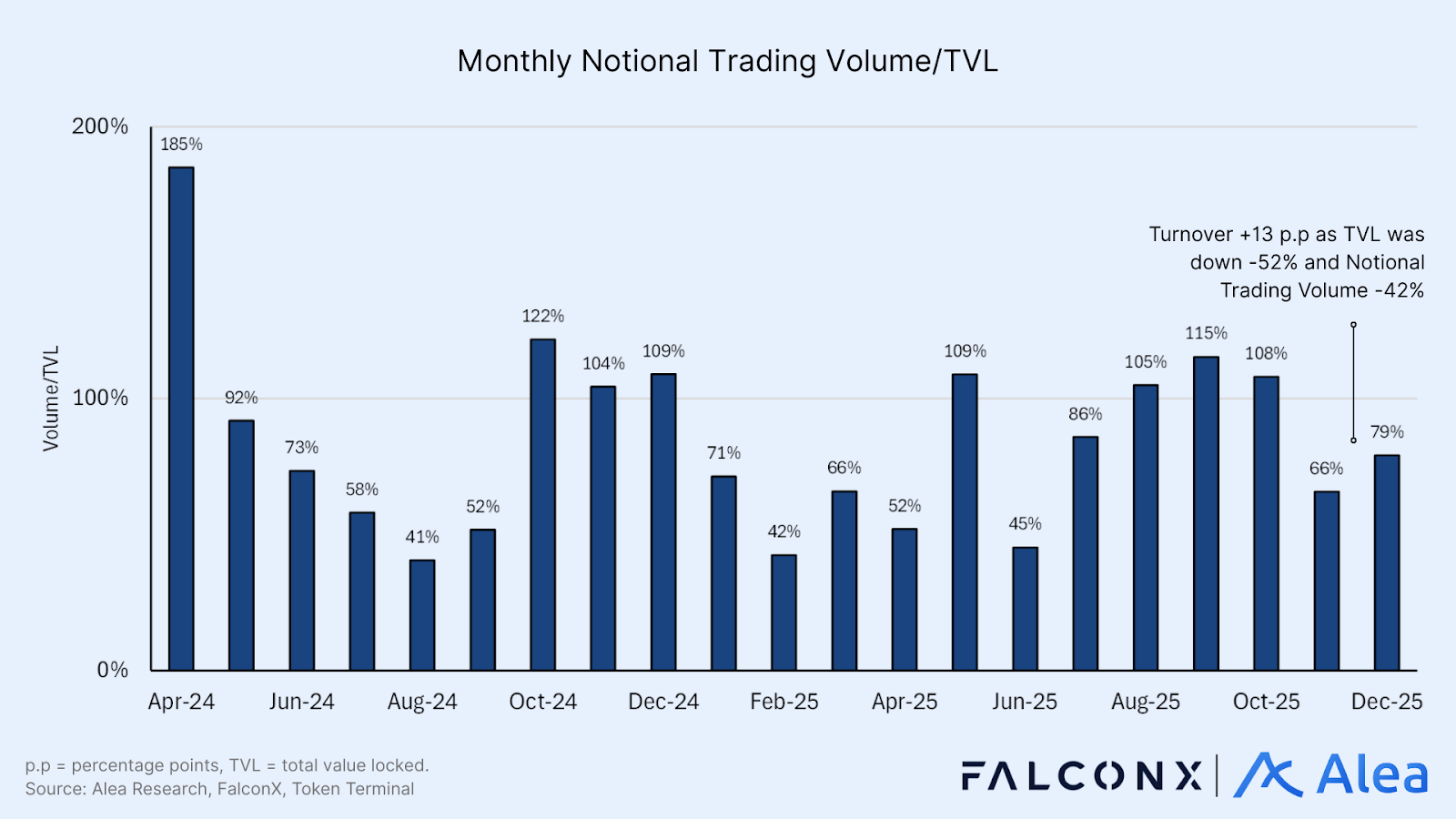

Pendle’s 2025 Recap

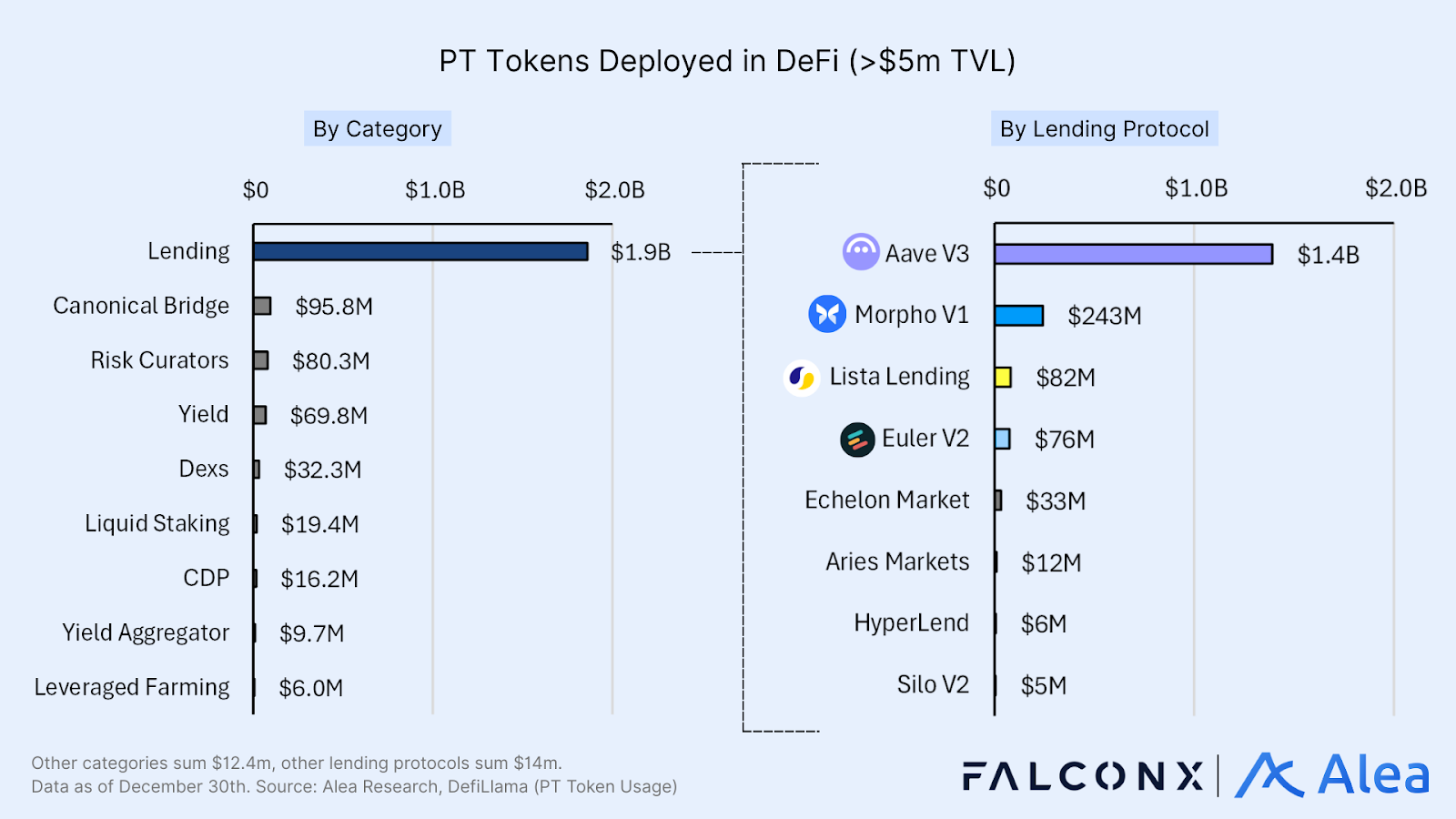

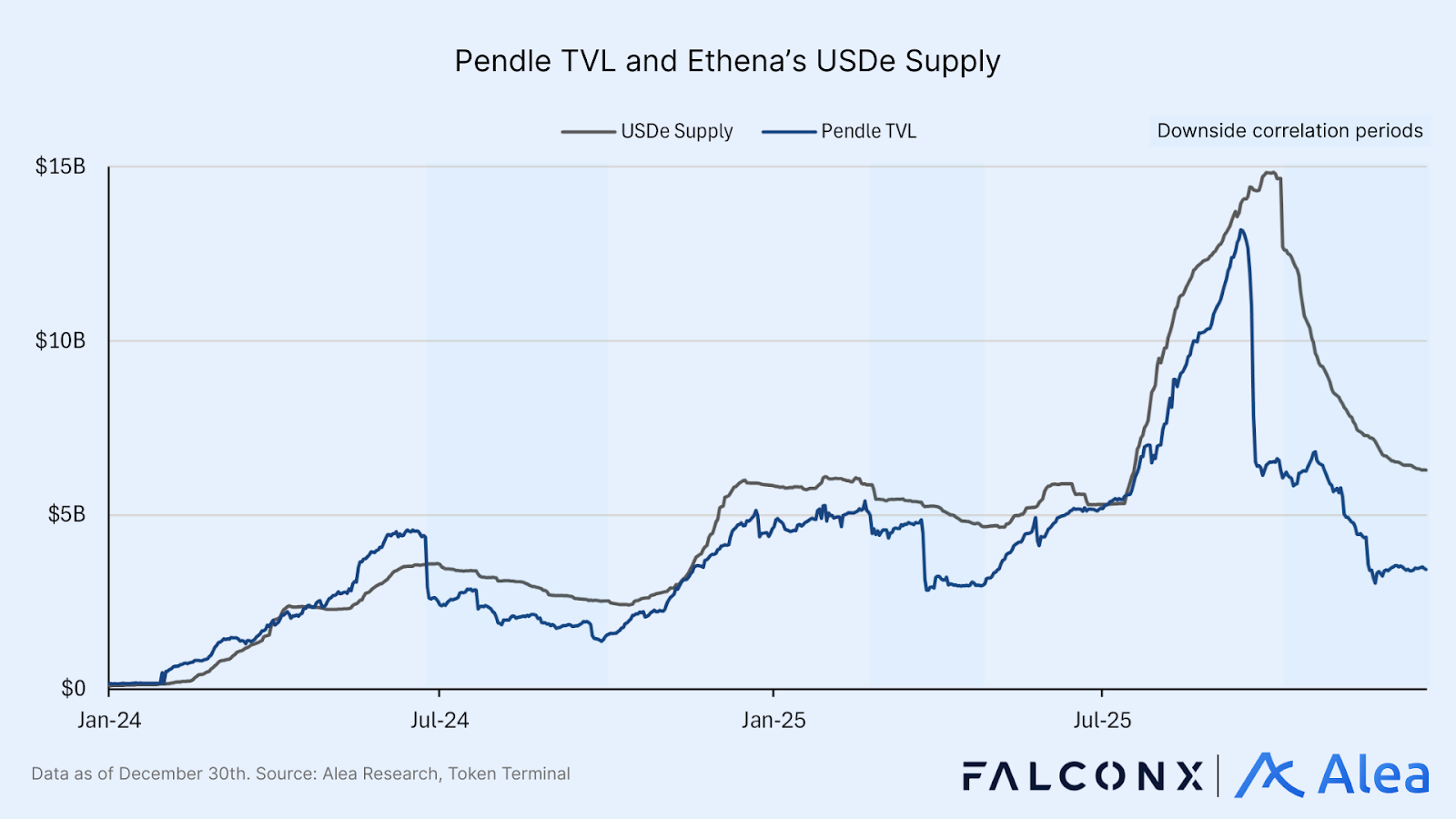

Pendle saw record activity in 2025, largely driven by Ethena and other yield-bearing stablecoin markets. This was further bolstered by leveraged looping strategies enabled by lending markets such as Aave, Morpho, and Euler, with Aave being a key catalyst.

Aave initially contemplated listing PT tokens as collateral in December 2024, and the first PTs on Ethena markets went live as collateral in April 2025. Due to strong demand, caps were raised and more Ethena PTs were listed over time. Pendle’s TVL went up in lockstep with USDe TVL as users participated in leveraged looping.

Ethena Season 4 incentives and cap raises in Aave PT markets snowballed and peaked heading into the September 25, 2025 PT maturity. This coincided with the conclusion of Ethena’s Season 4 rewards on September 24 as well as the expiration of 33 Pendle pools. Pendle’s TVL has remained subdued since then, as crypto prices and activity largely declined in Q4, reducing potential yields.

Pendle is also suffering lasting effects from the October 10th crypto market crash. Liquidations erased leverage users and cooled risk appetite; with yields halved relative to earlier in the year, v2 demand fell as leveraged loopers were forced to unwind.

PENDLE Valuation Framework

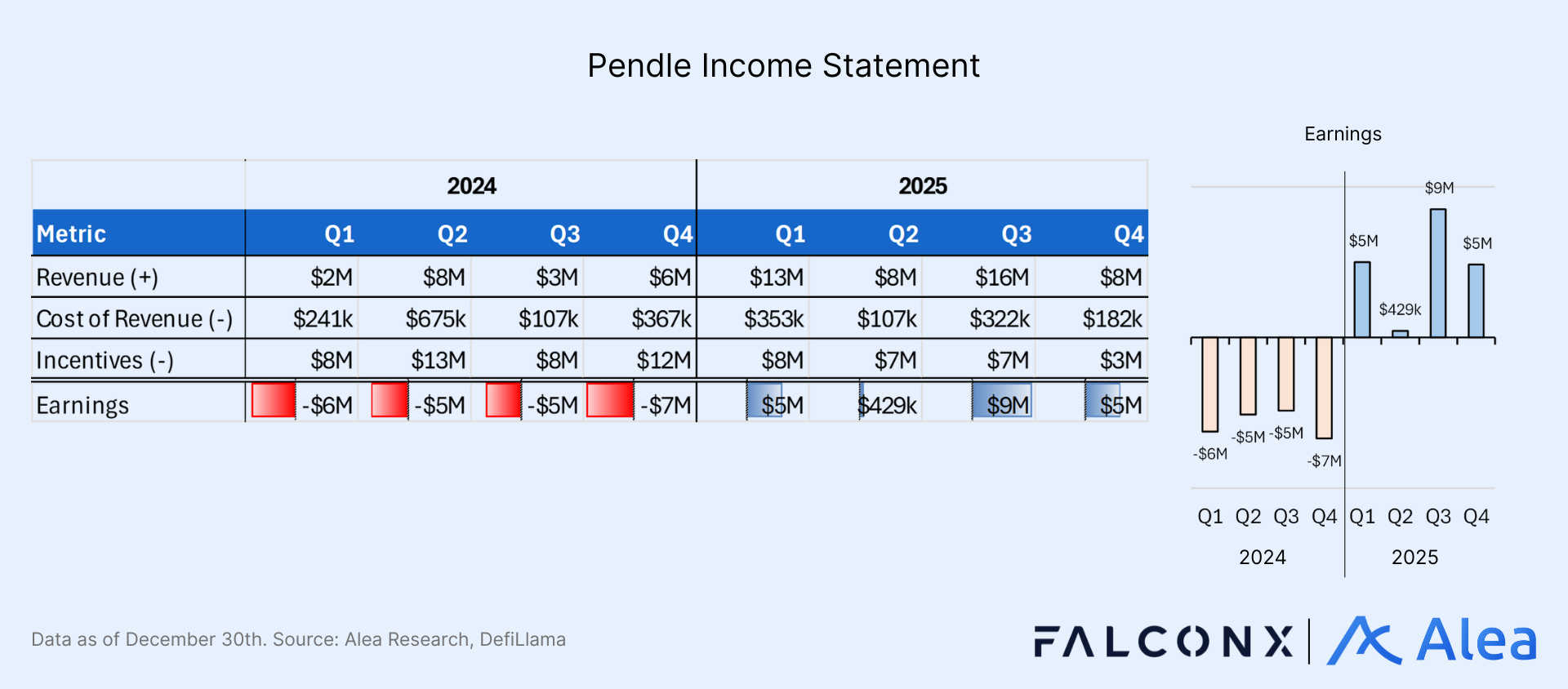

Pendle charges fees on yield and trading volume. It collects a 5% fee on yield accrued by YTs and 80% of trading fees (with the remaining 20% to LPs), with 80% of revenue distributed to vePENDLE as holders’ revenue (with the remaining 20% split 10% each between the Protocol Treasury and Protocol Operations wallets).

The business model ensures that fees scale with both TVL and rate volatility. Yield fees dominate when TVL and underlying yields are high, while trading fees rise as users hedge or speculate on rates. Historically, reliance on yield fees has tied revenue closely to TVL, amplifying the impact of sharp post-maturity drawdowns. Going forward, Boros is expected to address this by expanding the trading-driven fee base, helping stabilize revenue through TVL cycles.

Pendle’s vePENDLE dynamics are central to understanding supply/demand flows. PENDLE holders can lock their tokens for up to 2 years to access the protocol's cash flows and vote on what pools receive emissions. Over ~40% of the circulating supply is currently locked with an average lock duration of 395 days. New supply comes only from controlled emissions, which will stabilize at a ~2% annual inflation rate in 2026 (decaying 1.1% weekly until April 2026, then switching to 2% terminal rate for ongoing incentives).

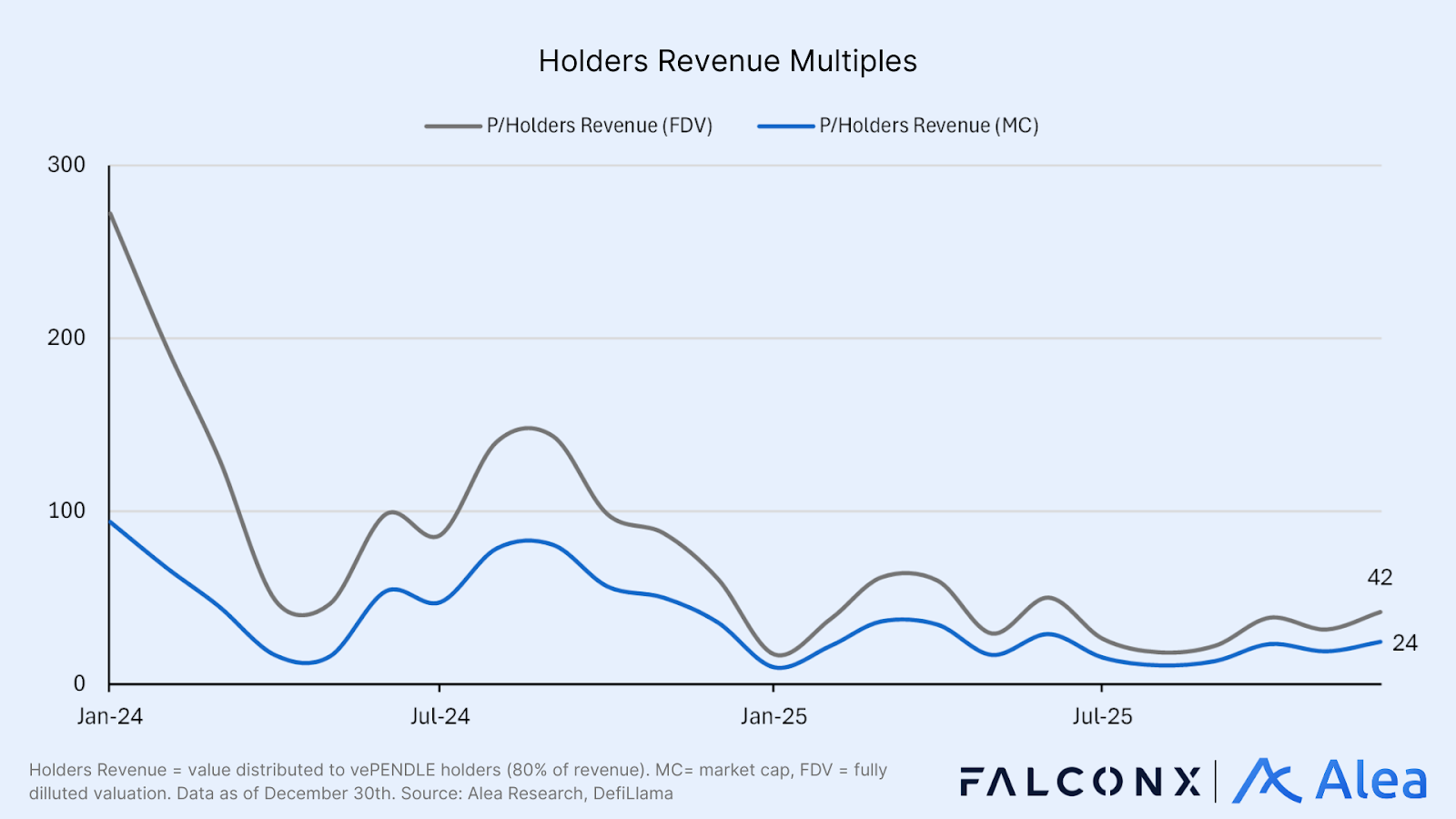

Pendle buyers can be classified into three main segments: vePENDLE lockers seeking cash flows and emission voting rights, LPs/protocols chasing boosted emissions for their pools, and liquid flow traders. The lockup structure, however, disadvantages liquid buyers as many funds may not wish to stay illiquid for prolonged periods of time. They may ultimately label PENDLE as a token without direct value accrual, since they cannot directly capture or access the protocol cash flows.

The marginal buyer, therefore, is presumed to be predominantly DeFi-centric participants willing to lock and vote. This dynamic, however, creates a paradox: the asset is valued by those who understand it best (and don’t mind locking), yet possibly undervalued in aggregate because larger capital pools face structural barriers to entry. Despite strong fundamentals, if the buyer set is limited, price cannot fully reflect true value. The valuation disconnect, therefore, is structural.

Staking penetration (~40% of circulating supply) offers the cleanest gauge of long-term demand. If the ratio rises while fees hold steady, the float tightens and the cashflow-buyer base strengthens; if it falls alongside declining fees, conviction is fading. Heading into 2026, however, Pendle’s tokenomics may be swimming against the current. Vote-locking (Pendle’s model) and buybacks (which is becoming the default for revenue-generating protocols) both return value to holders, but they select for different buyers.

Even though 2023 saw protocols building treasuries around vePENDLE, that era has passed. Since Hyperliquid’s success, the buyback model is becoming standard in DeFi. The reason is that it solves a structural exclusion problem: funds that cannot lock still benefit from protocol cash flows.

Buybacks are becoming the norm precisely because they open the door to liquid investors. They create buying pressure that otherwise may not exist. Whether Pendle follows and adopts this model is speculation, but the option may be on the table if one of the goals for 2026 is broadening the buyer base.

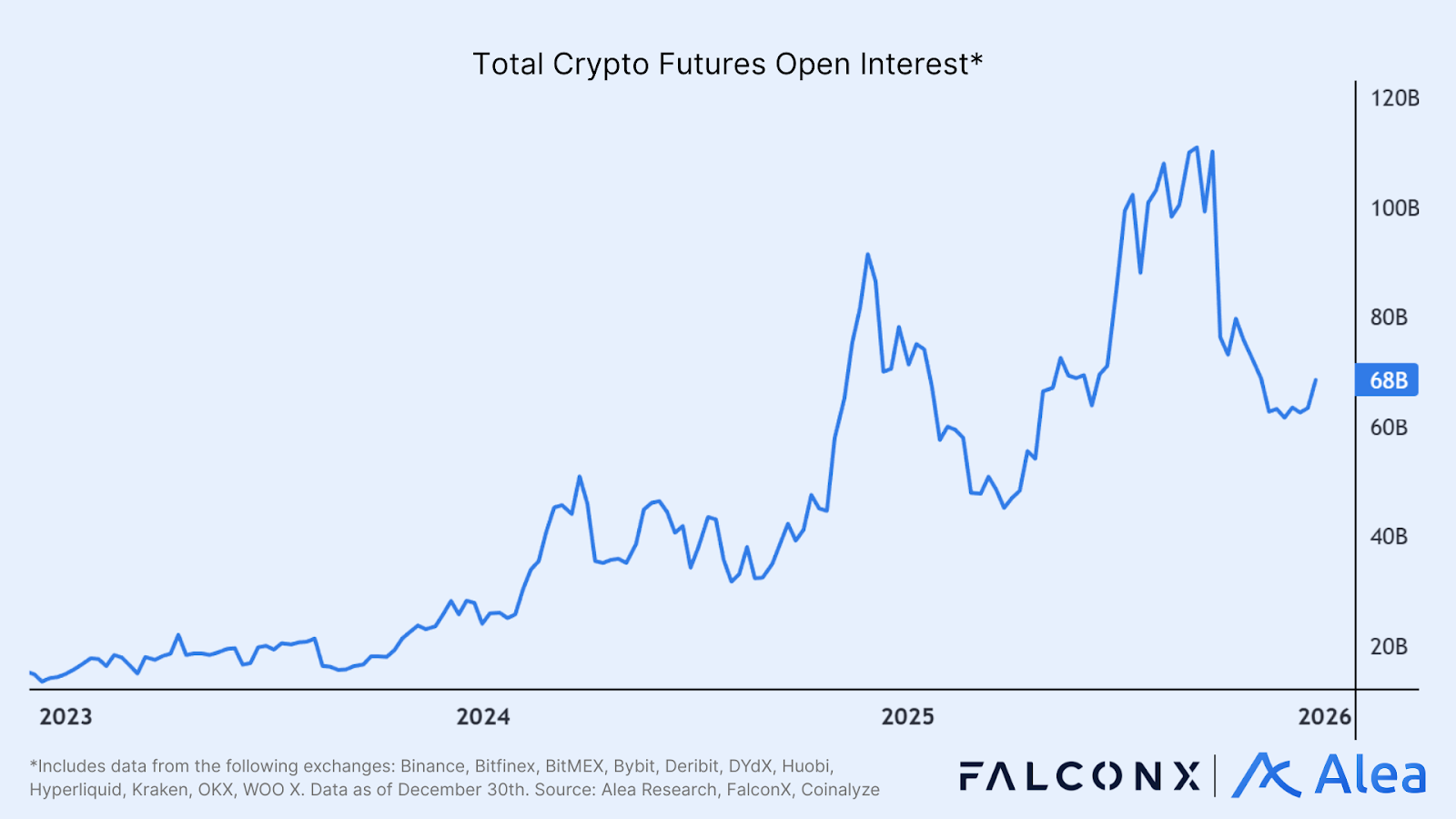

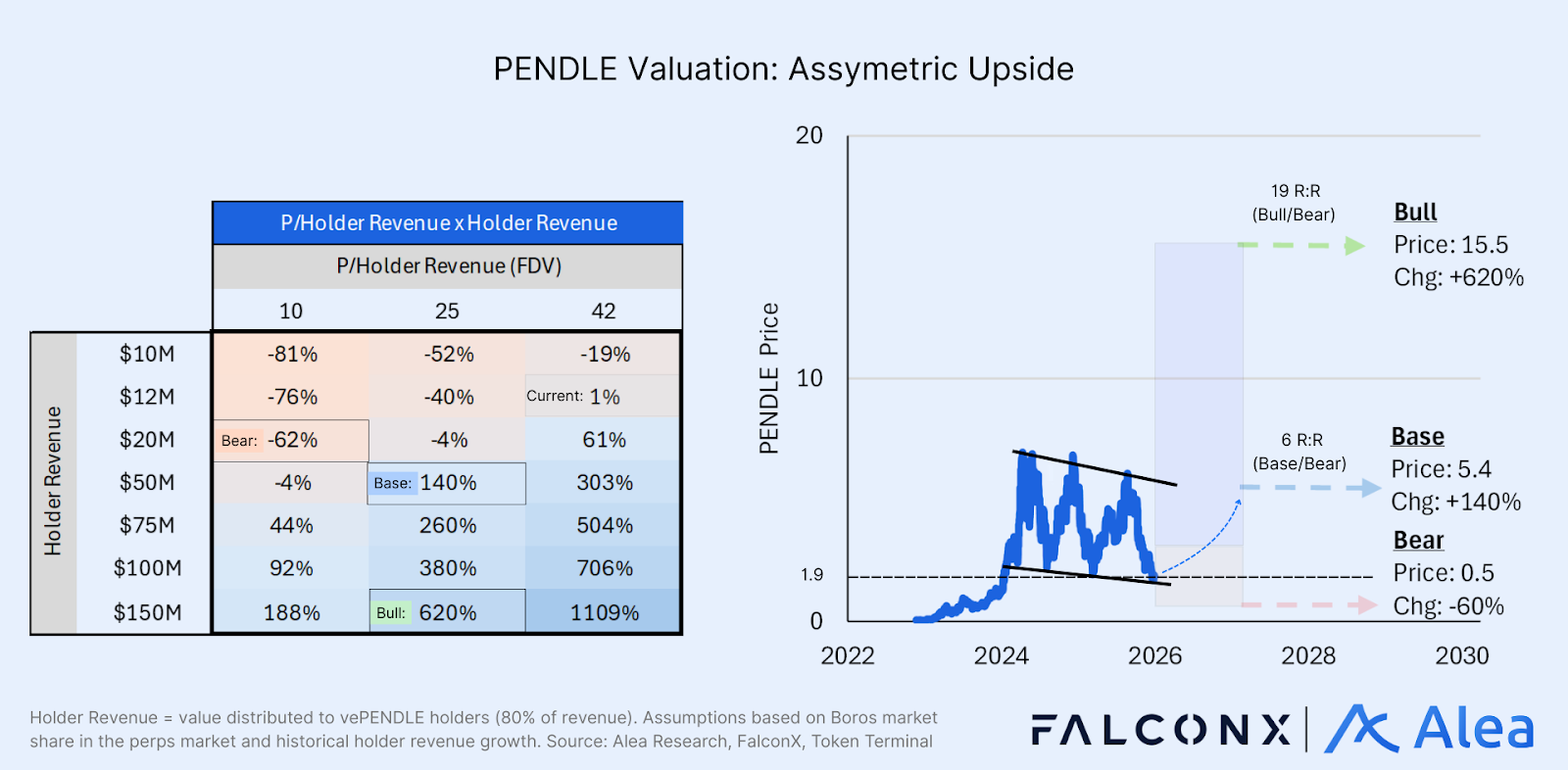

Interest rate derivatives are a massive market, with over $600T+ notional outstanding as of June 2025, per data from BIS. Nonetheless, Boros’ shorter-term opportunity sits within perps, which carries ~$70B of open interest to close 2025. For comparison, Boros had open interest of $245M right before its December 26, 2025 expiries. This translates into $1.2M run rate fees, resulting in a Fee/OI of nearly 0.5%.

Capturing 10% of perpetuals open interest appears achievable, given that many traders leave funding rates unhedged and considering Pendle previously reached roughly 10% of DeFi TVL at its peak. Under a more conservative path of capturing 2% of the perps market by 2026, implying roughly 10x growth in Boros open interest, Boros could drive up to ~15% incremental fee growth for Pendle, with substantially larger revenue potential if adoption compounds toward higher market share over time.

For those optimistic on Boros finding product-market-fit and funding rate derivatives being winner-takes-all (like yield stripping was), the current price implies the market is overlooking three things: quality of earnings (diversified fee sources across two distinct business lines), durability of growth (two independent growth vectors with different drivers), and unexpected tokenomics changes that could close valuation gap.

Risks & Invalidations

Pendle’s primary risk is compositional rather than competitive. Protocol activity has historically been concentrated in cyclical yield opportunities, such as Ethena. TVL leaving when maturities expire leaves fee generation in a vulnerable spot when yields compress. With funding-rate volatility more muted and episodic in recent periods, sustained demand for Boros is not guaranteed either.

Ultimately, the bull case rests on multiple correlated (not independent) tailwinds—more stablecoins, more RWAs, more institutional adoption, more yield sources, more yield-bearing stables hedging carry with Boros, broader Boros adoption across exchanges and pairs, and more structured products building on top. The bull case assumes this flywheel accelerates; the bear case is that these assumptions are not correlated.

Before Pendle, fixed yield in DeFi wasn’t reliably accessible. That helped to gain traction in crypto-native DeFi. Scaling to TradFi, however, means building infrastructure that doesn’t exist: regulatory compliance, KYC rails, legal structuring, institutional custody, etc. These aren't engineering problems; they're distribution and licensing problems that take years and partners to solve. If Pendle can't package its products for capital that won't touch raw DeFi, it can still be a category winner, but the category’s addressable market would be orders of magnitude smaller than the thesis implies.

Conclusion

Entering 2026, Pendle holds the dominant position in on-chain yield trading. This is a market segment on its way to become critical crypto infrastructure as fixed income matures on-chain. If there is a rate, Pendle can make a market. Boros is now kickstarting the next wave of growth. From on-chain lending benchmarks, staking curves, mortgages, or TradFi reference rates, Pendle has the long-term potential to define the on-chain map of a much broader fixed‑income stack.

The short-term thesis ultimately hinges on two questions: whether Boros achieves product-market fit and diversifies fees beyond TVL dependence, and whether tokenomics evolve through buybacks or governance changes to broaden the buyer base. The moat is built; the open question is whether the token structure allows the market to price it.

Evaluating Pendle over the next few quarters requires looking beyond TVL and headline fees. Leading indicators include market launch velocity, cross-chain traction, asset issuance pace, and shifts in fee mix from TVL-driven yield toward volume-based trading. These signals are expected to determine whether Pendle re-rates as rate infrastructure or remains a dominant protocol with a discounted token.

References

Pendle Boros Metrics Dashboard

vePENDLE Overview (Pendle App)

Medium, SeedTable, Cryptorank, Coindesk

Authors

This piece is co-authored by FalconX and Alea Research.

This memo is for informational purposes only and does not constitute investment, legal, tax, or financial advice, nor a recommendation to buy, sell, or hold any digital asset. Forward-looking statements reflect current expectations and involve substantial uncertainty; actual results may differ materially. Data sourced from third-party providers is believed reliable but has not been independently verified. Authors, Alea Research, FalconX, and their respective affiliated parties may hold positions in assets discussed, which may change without notice. Digital assets involve substantial risks including smart contract vulnerabilities, regulatory uncertainty, liquidity constraints, and total loss of principal. Recipients are responsible for their own due diligence and compliance with applicable laws. Alea Research and FalconX are not affiliated with, endorsed by, or sponsored by, each other.

This material is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd. nor Banzai Pipeline Limited (separately and collectively “FalconX”) service retail counterparties, and the information in this material is NOT intended for retail investors. This material is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this material is not and should not be regarded as investment advice, investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over the counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered with the U.S. Commodities Futures Trading Commission (CFTC) as a swap dealer and a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSAA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is a registered Class 3 VFA service provider with the Malta Financial Services Authority under the Virtual Financial Assets Act of 2018. FalconX Limited is licensed to provide the following services to Experienced Investors, Execution of orders on behalf of other persons, Custodian or Nominee Services, and Dealing on own account.

"FalconX" is a marketing name for FalconX Limited and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.