Liquidity Trends Suggest 'Uptober' Could Be the Start of a New Crypto Bull Run

Stronger interest from institutional investors and a market with relatively few sellers could mean we’ve entered a new phase of the market.

Originally published on Coindesk.

It was hard not to take notice of the “uptober” crypto rally. Bellwether BTC was up over 35% since October, and assets such as LINK and SOL are up two or three times that much.

Less explored, though, are the liquidity trends underpinning this price action. Observing these can help us gauge where we are in the cycle and thus navigate what the future market might hold.

As we highlighted for CoinDesk earlier in the year, price changes with low trading volumes are less reliable indicators than those with higher volumes. Low volumes suggest limited market participation at a particular price level, potentially leading to greater price volatility and reduced market depth.

Conversely, higher trading volumes signify broader market participation, indicating a stronger consensus and offering a more dependable basis for price movements, thereby bolstering the credibility of the signal.

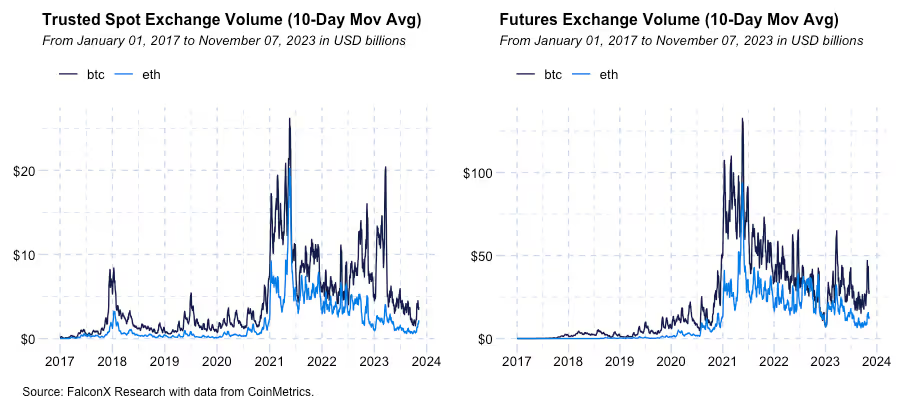

Trade volume recovery in BTC and ETH, the most watched liquidity metric, is eye-catching. Two of the top-15 trading volume days since the market top two years ago were recorded during this recent rally. And most of the other high-volume days happened as dramatic company failures were taking place in 2022, or as several mid-sized U.S. banks got into difficulty in March 2023. BTC Spot volumes, which until September were breaking three-year lows, have steeply recovered and are now approaching six-month highs.

But this is not the whole story. Digging deeper into liquidity trends can provide us further insight.

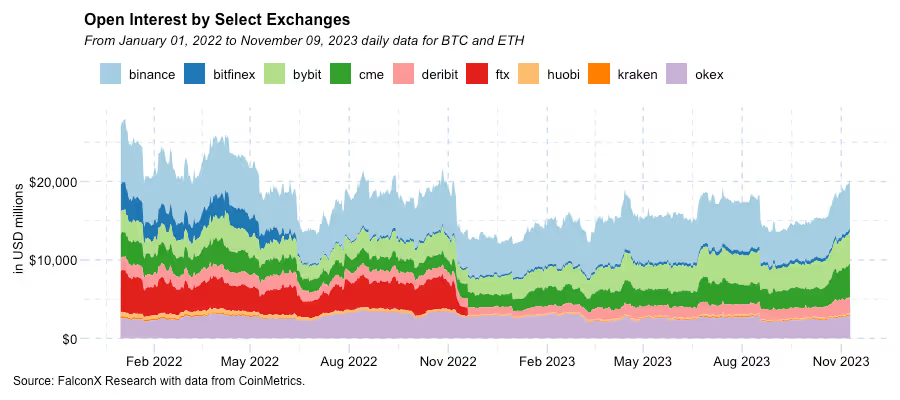

Strong action on the derivatives side, especially in the CME

Futures open interest (OI) in BTC and ETH just crossed the $20 billion mark for the first time since the FTX meltdown in November 2022, led by BTC on the back of excitement around the highly anticipated U.S. spot ETF launch.

Notably, but perhaps not surprisingly, this increase is led by institutional capital. The CME, a favorite venue for large traditional finance companies to get crypto exposure, gained the most market share across all venues and is close to overtaking Binance as the leading BTC futures exchange by OI.

A similar trend can also be seen on options.

Open interest in BTC options just crossed $16 billion, and volumes are now at all-time highs. Much of this action is translated to spot prices because a relevant part of these flows is likely hedged into spot. There’s a flipside: a more pronounced derivatives market means there’s more inherent leverage in the system. So the risk of forced liquidations exacerbating price movements will likely increase from here.

Spot Orderbooks Tightened and Revealed a Relative Lack of Sellers

Order book depth – an alternative liquidity metric that gauges how much capital would be required to change the asset price by a certain percentage given the limit orders in place at any time – has tightened over the past few months, despite the strong price increases.

The chart below shows the 1% depth of book for BTC and ETH (top and bottom, respectively) in U.S. dollars and native units (left and right, respectively) over 2023. There is a decrease over the past 3-5 months, whichever chart you look at. And the sell side of the orderbook is trending toward shrinking by more than the buy side, suggesting a lack of sellers relative to buyers.

Busy Derivatives Dynamics Meet a Tight Spot Market With a Lack of Sellers

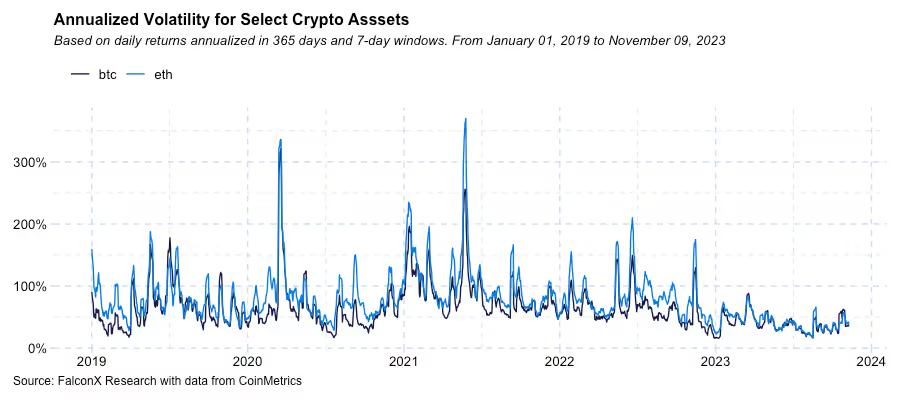

The chart below shows annualized realized volatility for BTC and ETH using a seven-day lookback period to capture the recent price surge. Although volatility picked up recently, it remains relatively low for both BTC and ETH, as it did not break above 63% on an annualized basis, which is below the median value during the previous bull market in 2020 and 2021.

This matters to liquidity because volatility usually drives higher trading activity. BTC’s current spot volumes adjusted by volatility are already in the top quartile of the 2020/2021 bull market cycle.

This Rally Feels Different

Stronger interest from more traditional institutional investors and a market with relatively few sellers amid increasing but still relatively low volatility point to the market shifting gears to a new phase.

Looking forward, even if the possibility of interim corrections grows from there and the macro environment remains cloudy, this rally might be the start of the next bull market.

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd. nor Banzai Pipeline Limited service retail counterparties, and the information in this material is NOT intended for retail investors. This material is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this material is not and should not be regarded as investment advice, investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over the counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a Swap Dealer with the U.S. Commodities Futures Trading Commission and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is licensed by the MFSA as a Class 2 Crypto-Asset Service Provider (Regulation (EU) 2023/1114). It is also licensed as a Financial Institution (Cap. 376) exclusively for EMT payment services.

"FalconX" is a marketing name for the FalconX Group and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.