2Q26 Crypto Market Review

The second quarter of 2026 extended crypto's downturn. BTC fell 14% to close around $59K, adding to its 22% decline in 1Q26, while aggregate crypto spot and futures volumes fell to their lowest levels since 2023.

Investing in digital assets or tokenized equities involves a substantial degree of risk. Market prices can be highly volatile and unpredictable. Movements in the market can result in significant, rapid, and potentially total loss of your invested capital. Before allocating capital, you should carefully evaluate whether such investments align with your financial situation, experience, and risk tolerance. For further information regarding potential risks, please refer to the disclaimer below.

Summary

2Q26 saw crypto spot volumes decline 42% YoY, while futures volumes fell 31%. Crypto futures open interest drifted from $56B to $53B over the quarter, holding near the deleveraged levels reached in 1Q26. Spot volumes declined to a multi-year low, but the trajectory improved within the quarter (June volumes rose 7% versus April after bottoming in May) suggesting the activity reset may be stabilizing, though the month’s greater volumes may simply reflect other factors, such as volatility around concerns over MSTR’s capital allocation strategy.

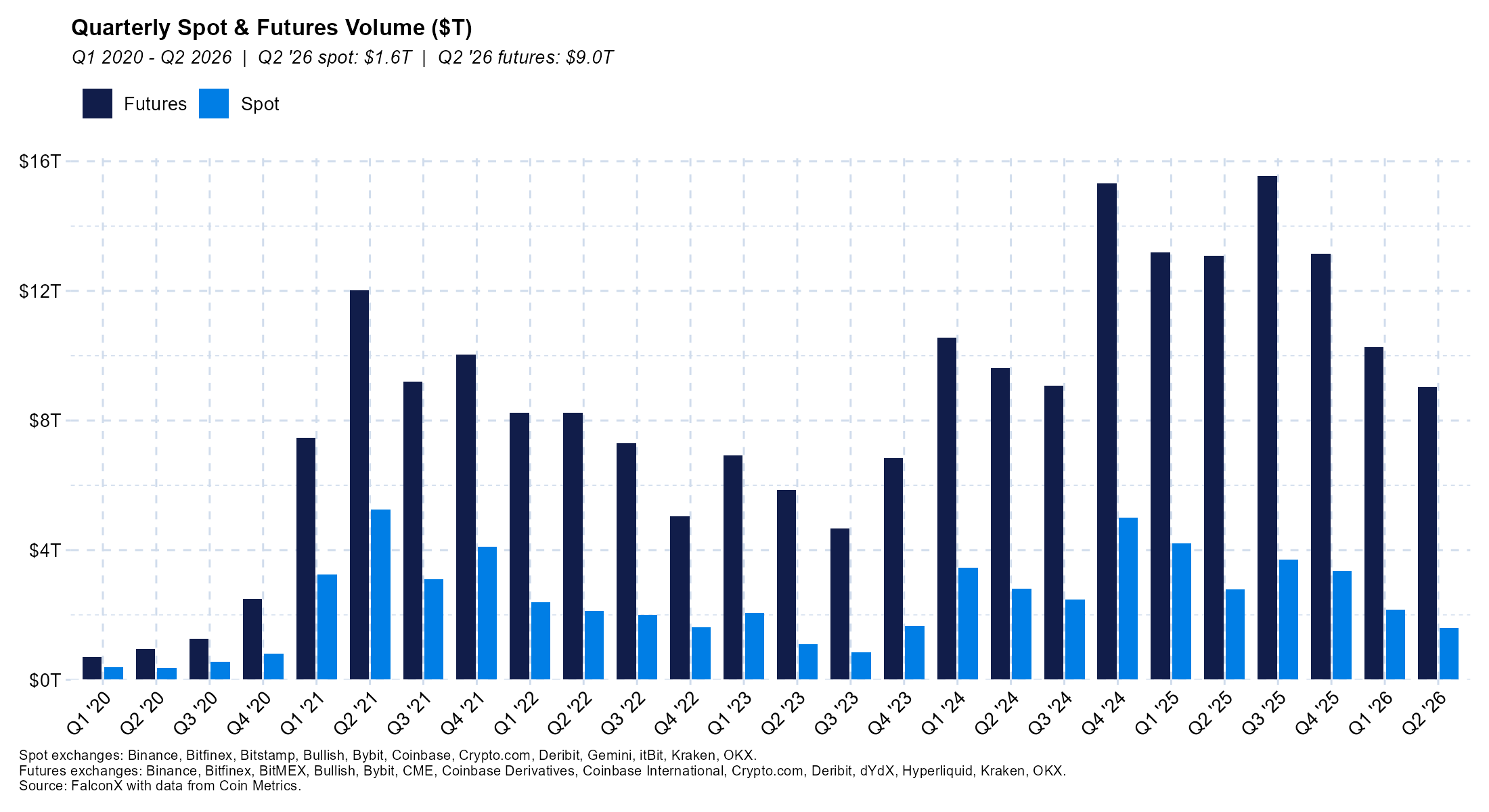

Spot and Futures Volumes at Lowest Since 2023

Spot volume across a set of 12 leading exchanges[1] totaled $1.6T in 2Q26, -25% from the prior quarter and -42% from a year ago, per data from Coin Metrics. The data indicates that this was the weakest quarter since 3Q23 ($0.8T in spot volumes), compared to $1.7T in 4Q23.[2] Within the quarter, volumes hit a low in May ($503B) before recovering: June volumes of $568B rose 13% vs May and 7% vs April ($533B). June spot volumes were down 61% relative to October 2025 ($1.5T), when crypto markets were near their cycle highs.

Futures volume, across a set of 14 venues[3], totaled $9.0T, -12% QoQ and -31% from a year ago. Futures volumes were the softest since 4Q23 ($6.8T), dipping just below 3Q24's $9.1T.

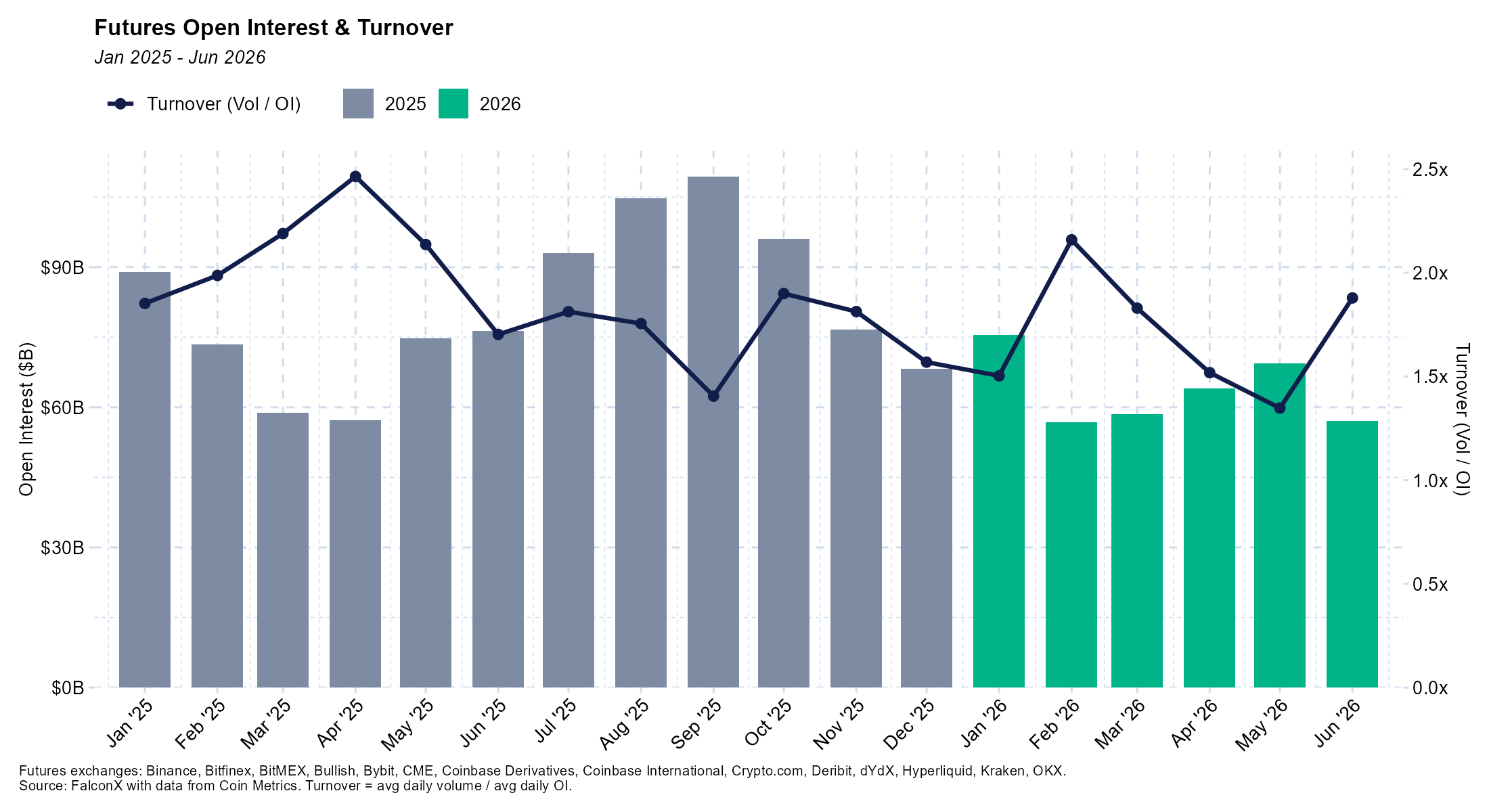

Futures Open Interest Holds Near Q1 Lows

Aggregate futures open interest across the same set of venues (OI) ended June at $53.2B, down 56% from October 2025's $122.2B peak and compared to $56.5B at the end of 1Q26, a decline of 6% QoQ. The turnover ratio (volume / OI) sat at 1.6x in the quarter, down from 1.8x in 1Q26, reflecting a market where more of the OI consists of longer-term positioning rather than short-term speculative activity.

Within the quarter, average daily OI ran ~$64B in April and ~$69B in May before drawing down to ~$57B in June; monthly turnover moved 1.5x / 1.4x / 1.9x across April / May / June (vs. 1.5x / 2.2x / 1.8x in 1Q26's three months).

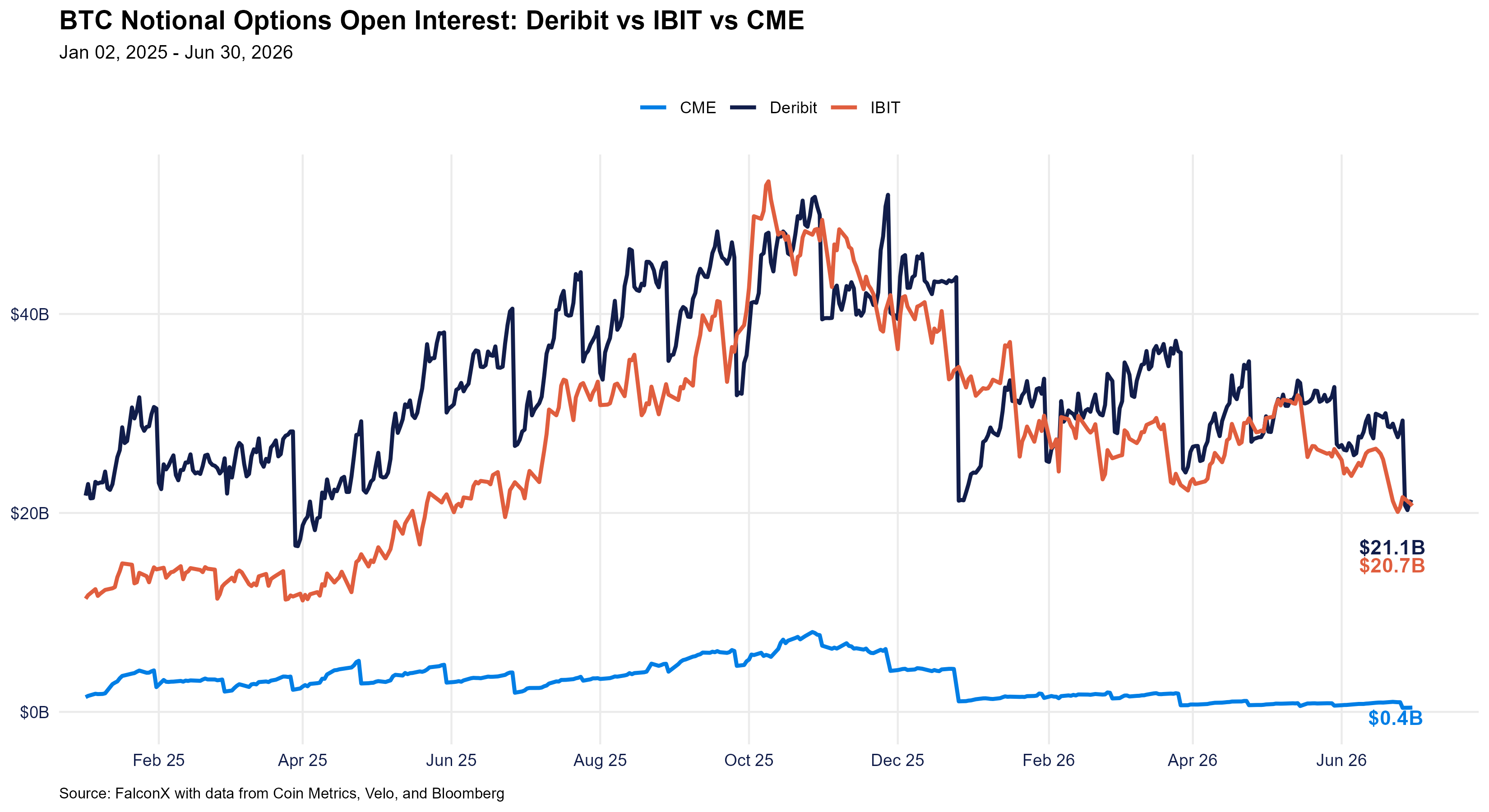

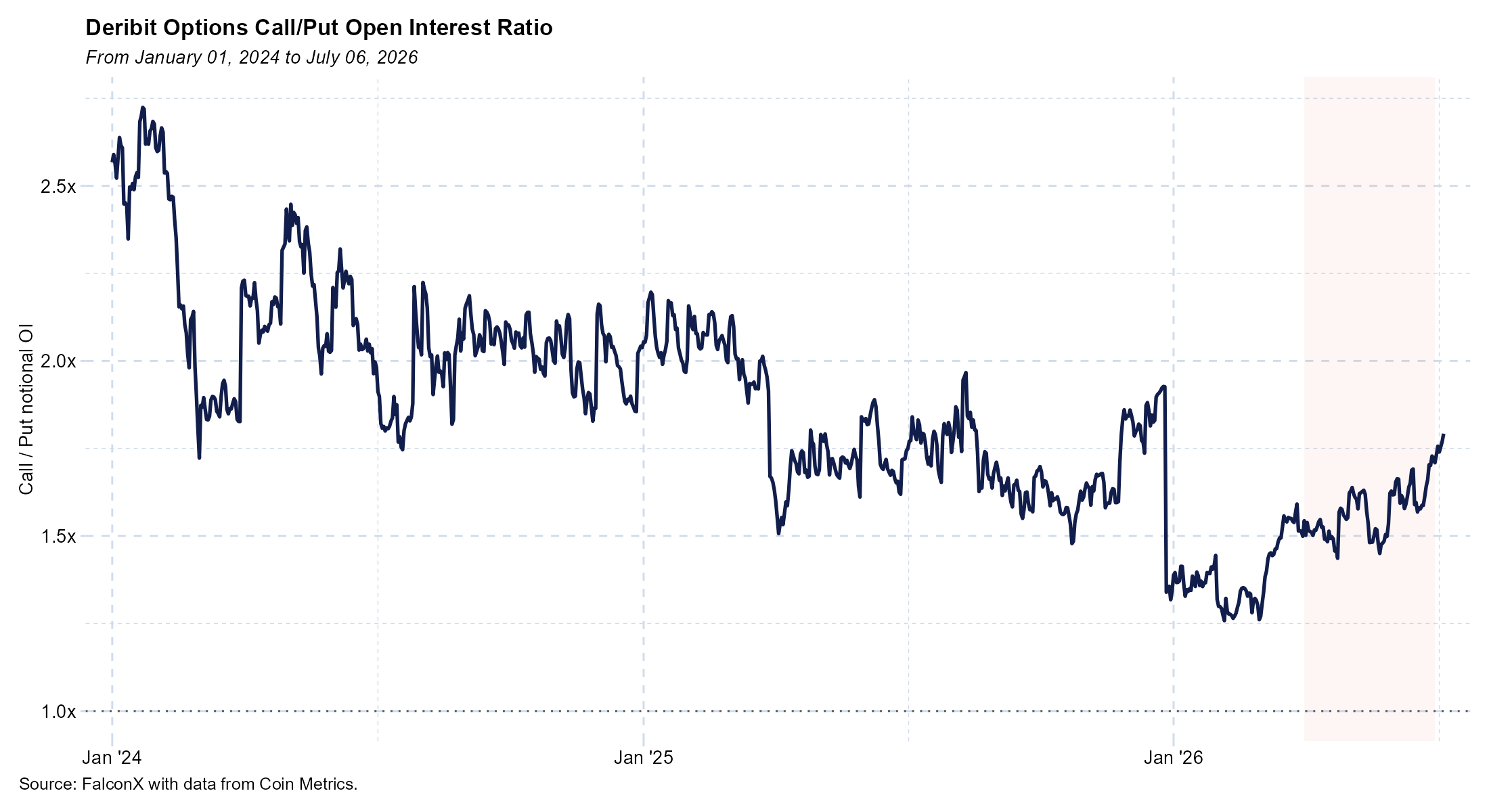

BTC Options OI Extends Its Reset

BTC notional options open interest continued to compress into the late-June quarterly expiry. As of June 30, 2026, Deribit BTC notional OI totaled $21.1B vs IBIT's $20.7B. Deribit remained ahead, but the gap narrowed from 1Q26 (Deribit $26.7B vs IBIT $22.9B). CME BTC options stood at $0.4B. Combined across the three major venues, BTC notional options OI stood at roughly $42B, down from ~$50B at the end of 1Q26 and still less than half the ~$110B at the 4Q25 peak.

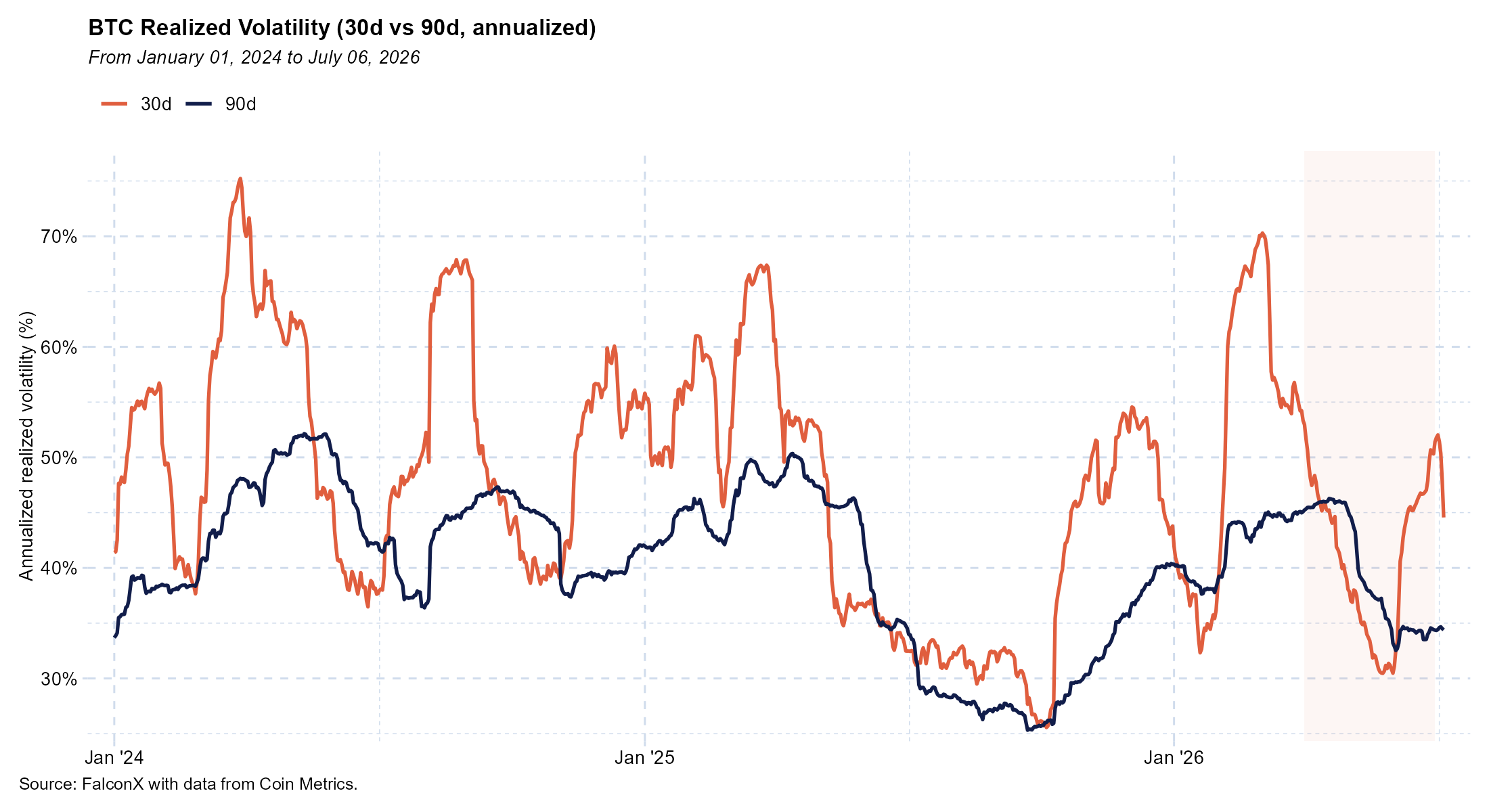

BTC realized volatility compressed in the quarter, ending June with 30D and 90D vols at 51% and 34%, respectively, indicating a calming, deleveraging market. The BTC selloff in mid-June marked a pickup in 30D vol in the period and was driven in part by trading activity around MSTR developments.

Despite the broader deleveraging YTD, the call/put open interest ratio increased over the quarter, suggesting traders may be positioning for a potential bounce in BTC.

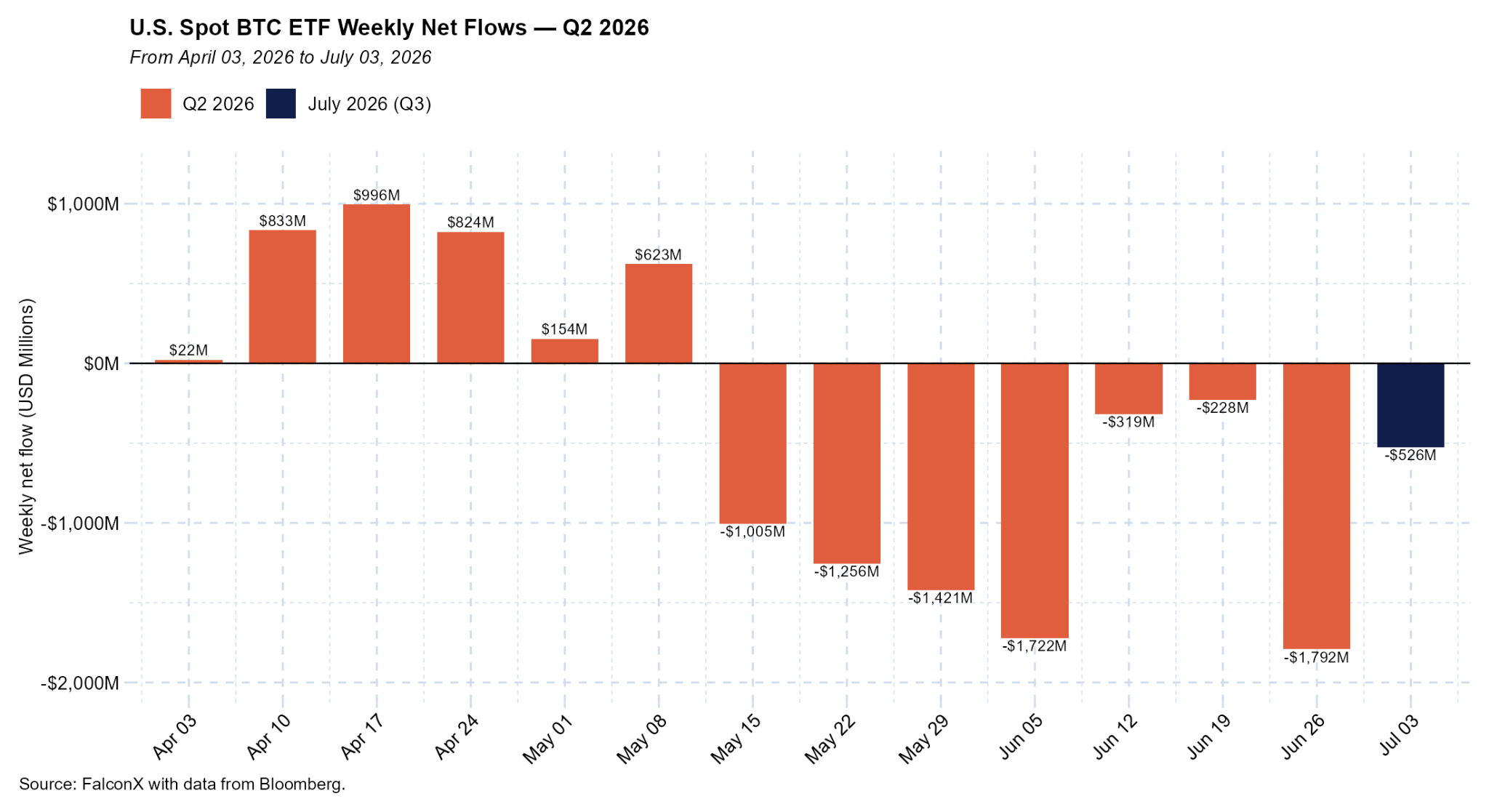

BTC ETFs See Heavy Outflows, HYPE ETFs See Strong Debut

BTC ETF outflows turned sharply negative in the quarter (-$4.9B), potentially reflecting MSTR concerns and a freeing of capital around the SpaceX IPO. This brought YTD ETF flows to -$5.4B. The nuance here is that this was a very recent trend with $8.2B in outflows since May 12.

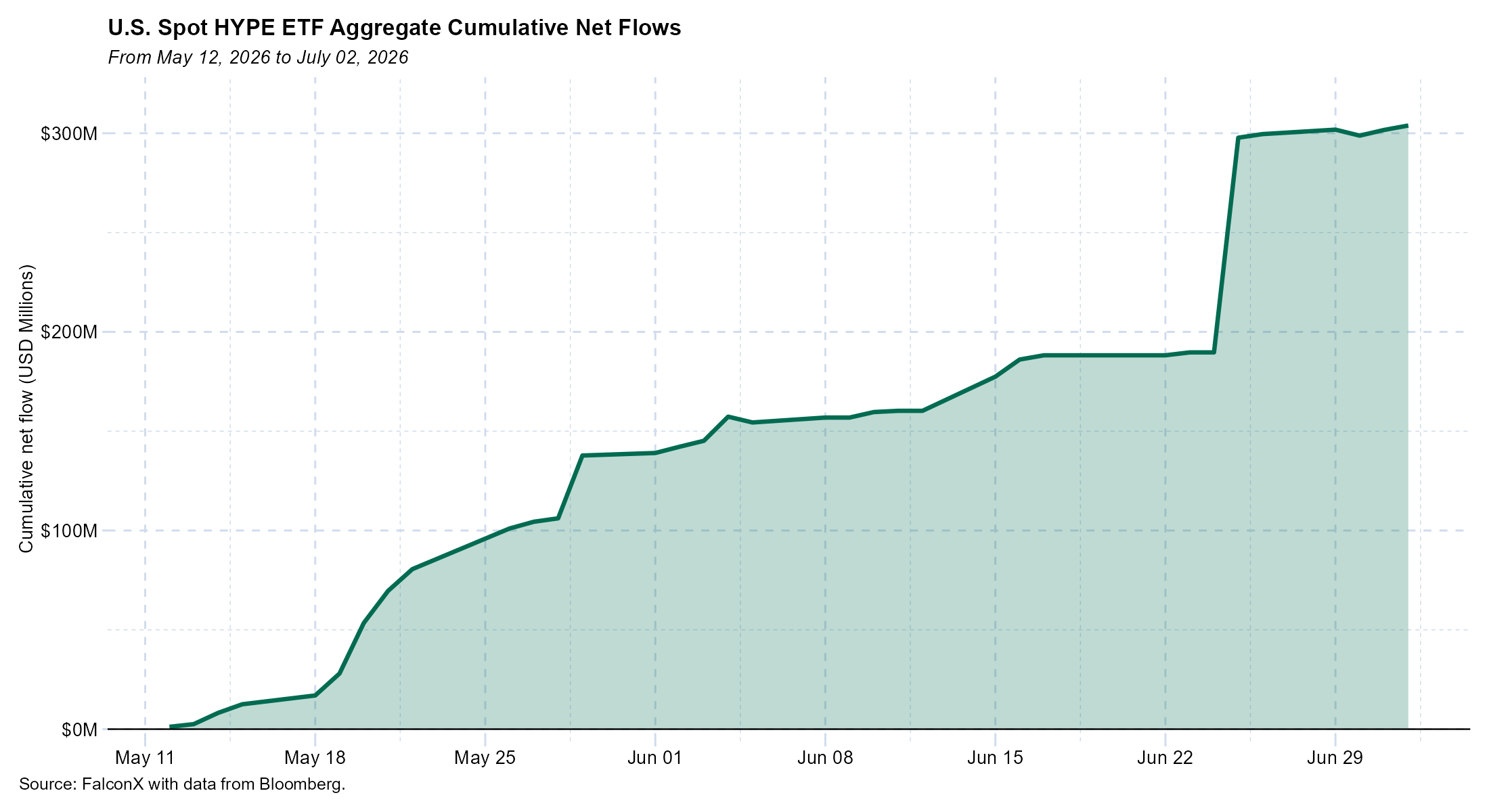

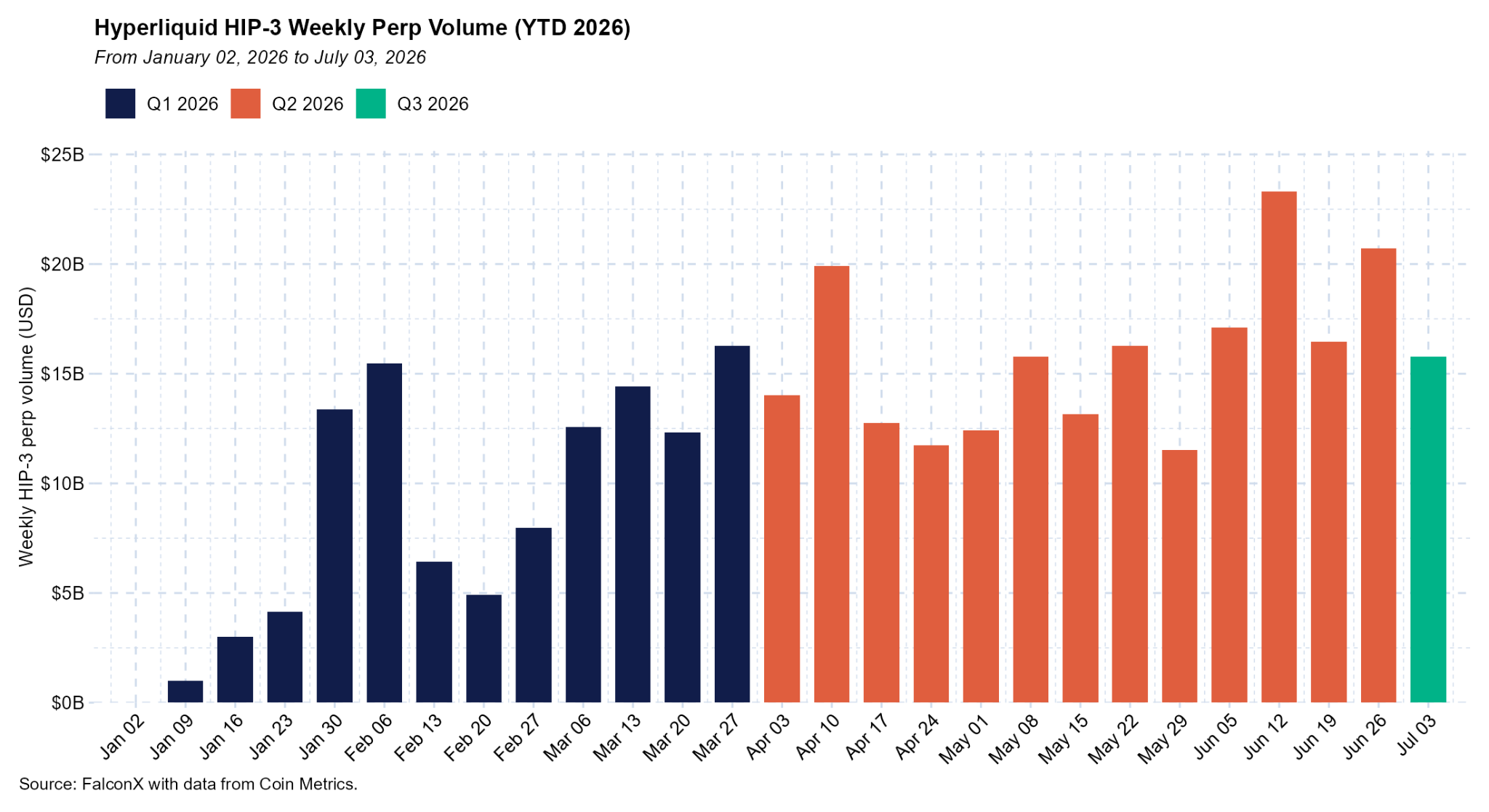

Hyperliquid (HYPE) stood out in the quarter given its positive ETF flows ($300M), especially relative to its market cap ($15B). The apparent implication that new crypto ETF launches could see strong interest despite a broader crypto bear market seems noteworthy.

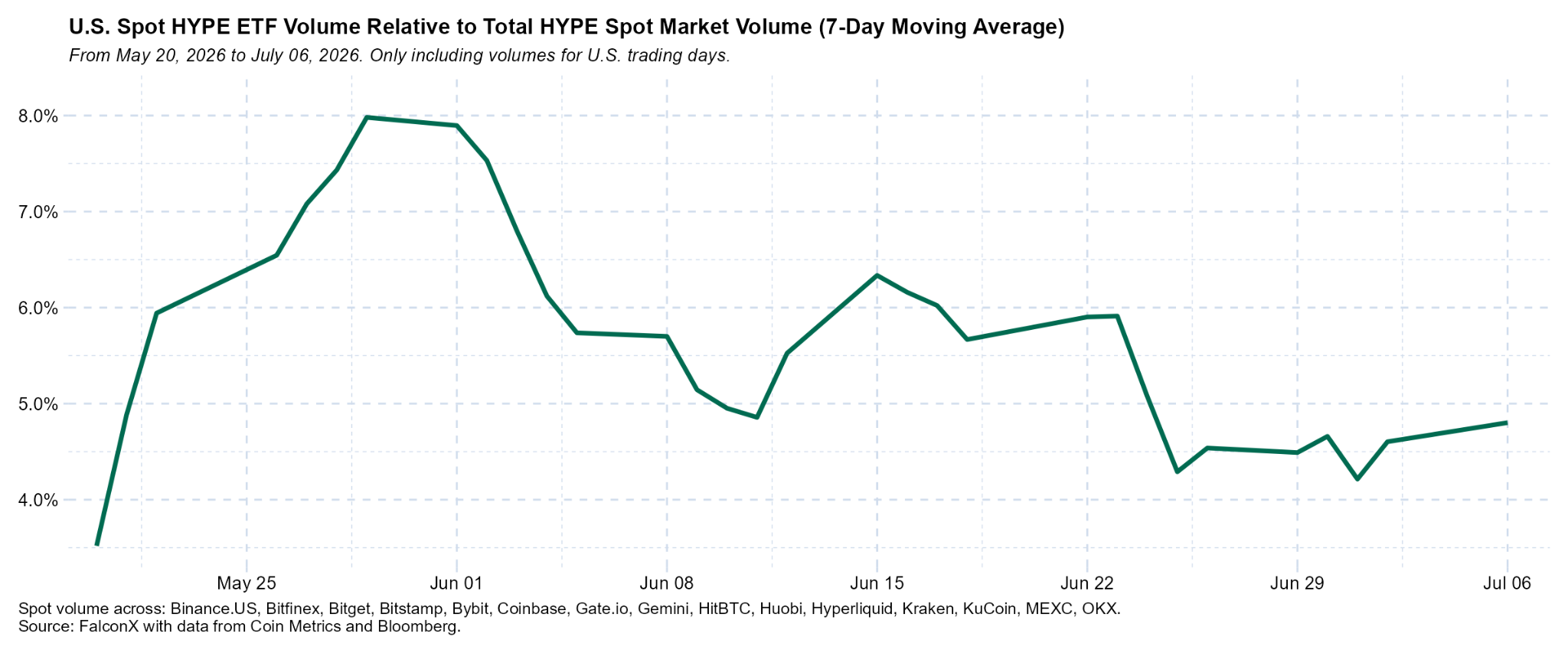

HYPE ETF volumes relative to HYPE spot volumes surged to as much as 8% in the weeks after launch, but trended down to around 5% by quarter end. For context, this compares to BTC ETF volumes rivaling 30-40% of BTC spot volumes. For HYPE, it strongly suggests crypto-native venues still dominate price discovery.

HYPE ETF inflows may have been supported by record-high HIP-3 volume in the month, driven by activity around the SpaceX IPO. Hyperliquid is an apparent key player in the ‘convergence’ narrative, with perpetuals on traditional asset classes consistently making up over 30% of total Hyperliquid platform volumes.

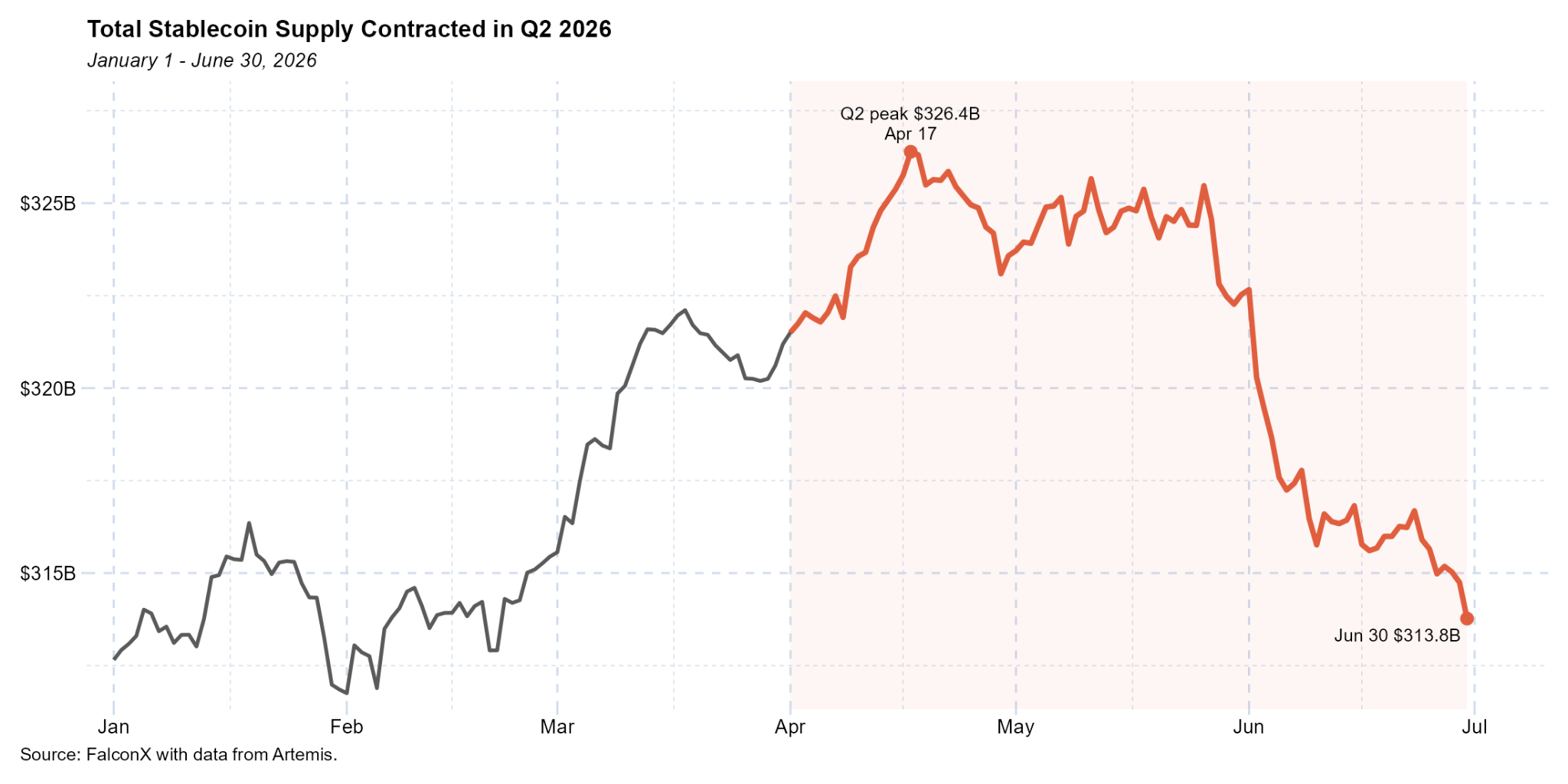

Stablecoin Supply Contracts in Q2

Total stablecoin supply experienced a prolonged contraction for the first time in several quarters, according to data from Artemis, slipping from $321.2B on March 31 to $313.8B on June 30, a decline of $7.4B, or -2.3%. Supply peaked at $326.39B on April 17 before drifting lower through the rest of the quarter.

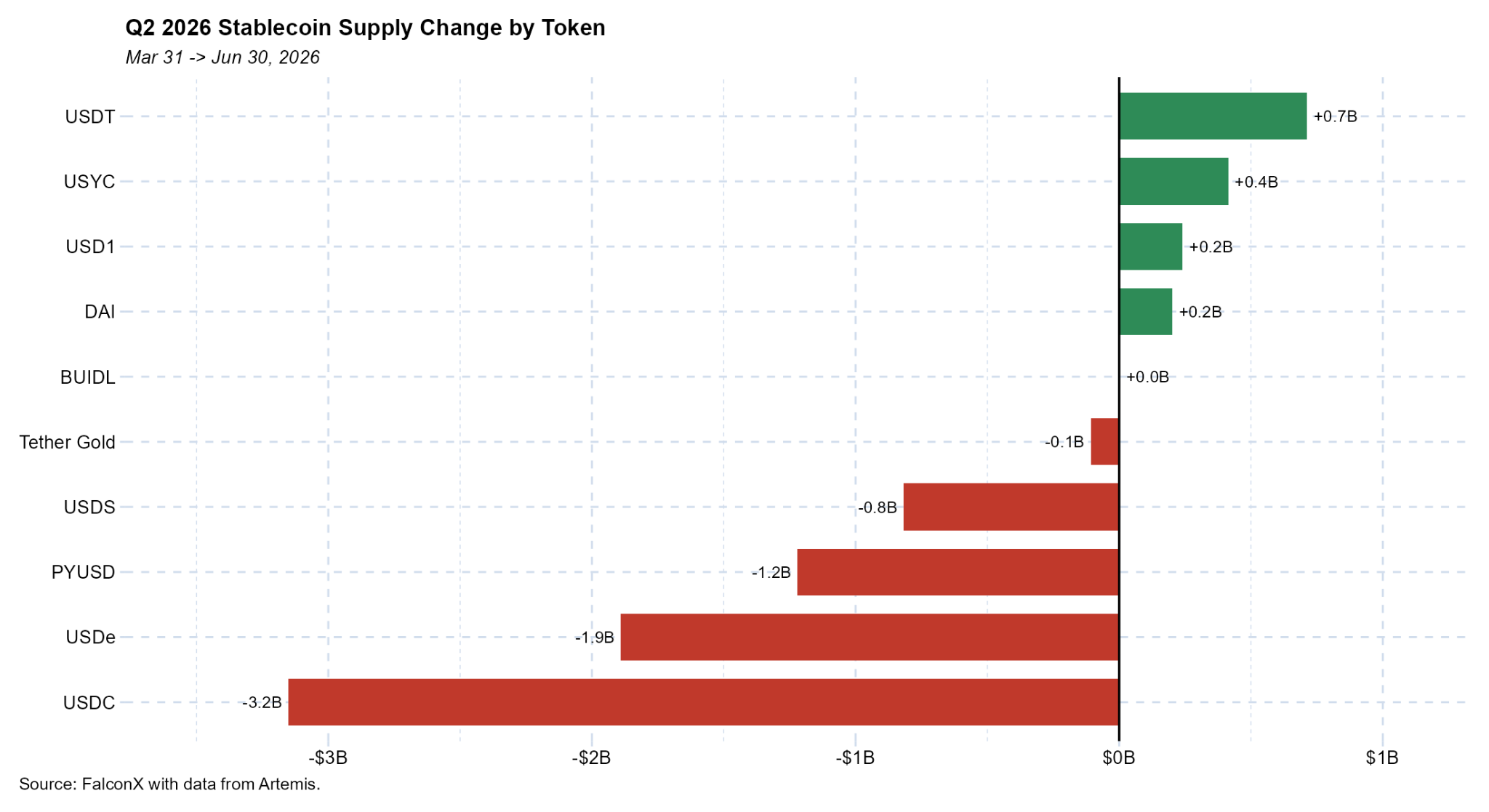

By stablecoin, USDT (+$0.7B), USYC (+$0.4B), USD1 (+$0.2B) and DAI (+$0.2B) grew, while USDC (−$3.2B), USDe (−$1.9B), PYUSD (−$1.2B) and USDS (−$0.8B) drove the net decline.

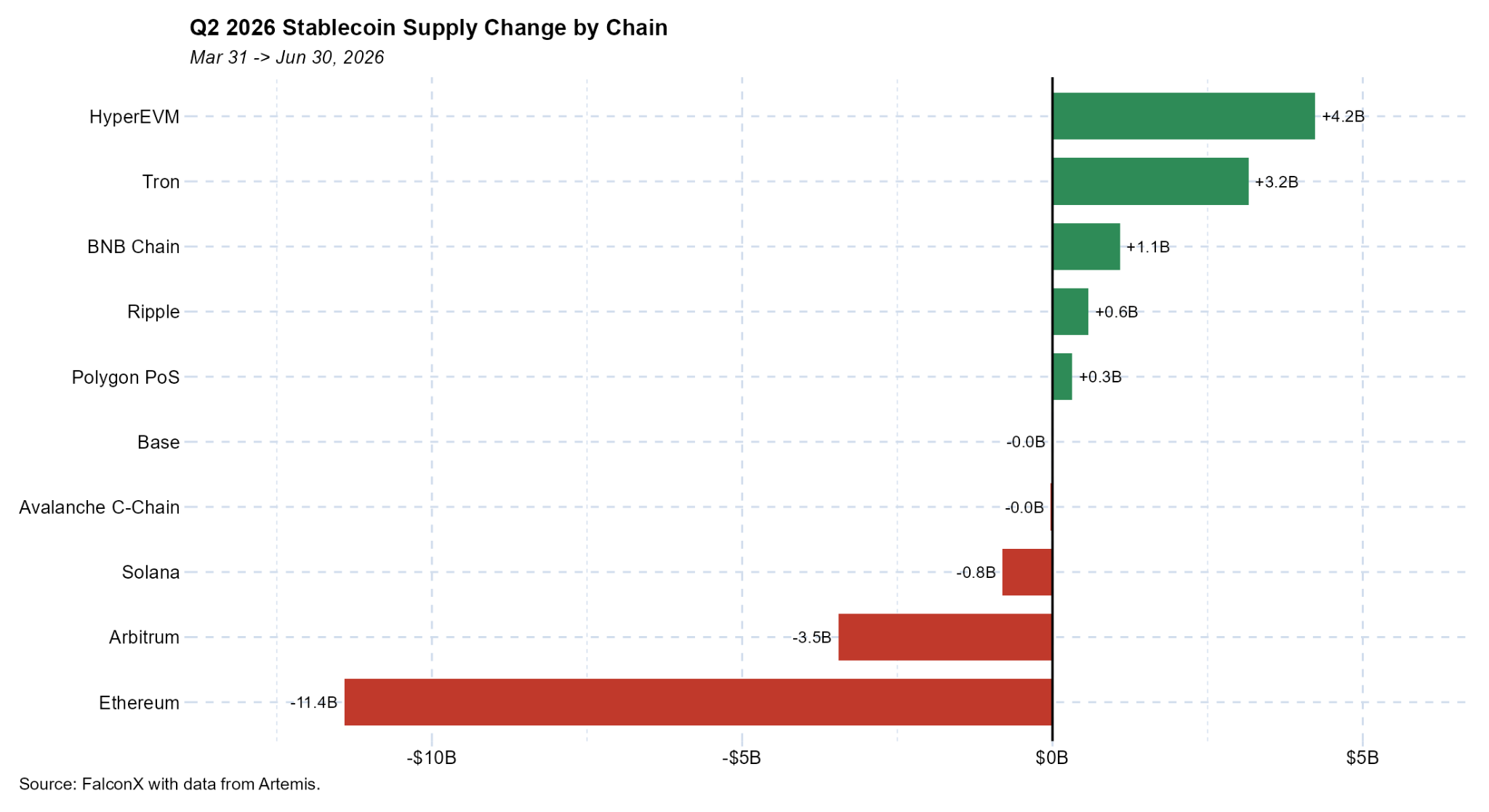

By chain, HyperEVM (+$4.2B), Tron (+$3.2B) and BNB Chain (+$1.1B) gained supply, more than offset by outflows on Ethereum (−$11.4B), Arbitrum (−$3.5B) and Solana (−$0.8B).

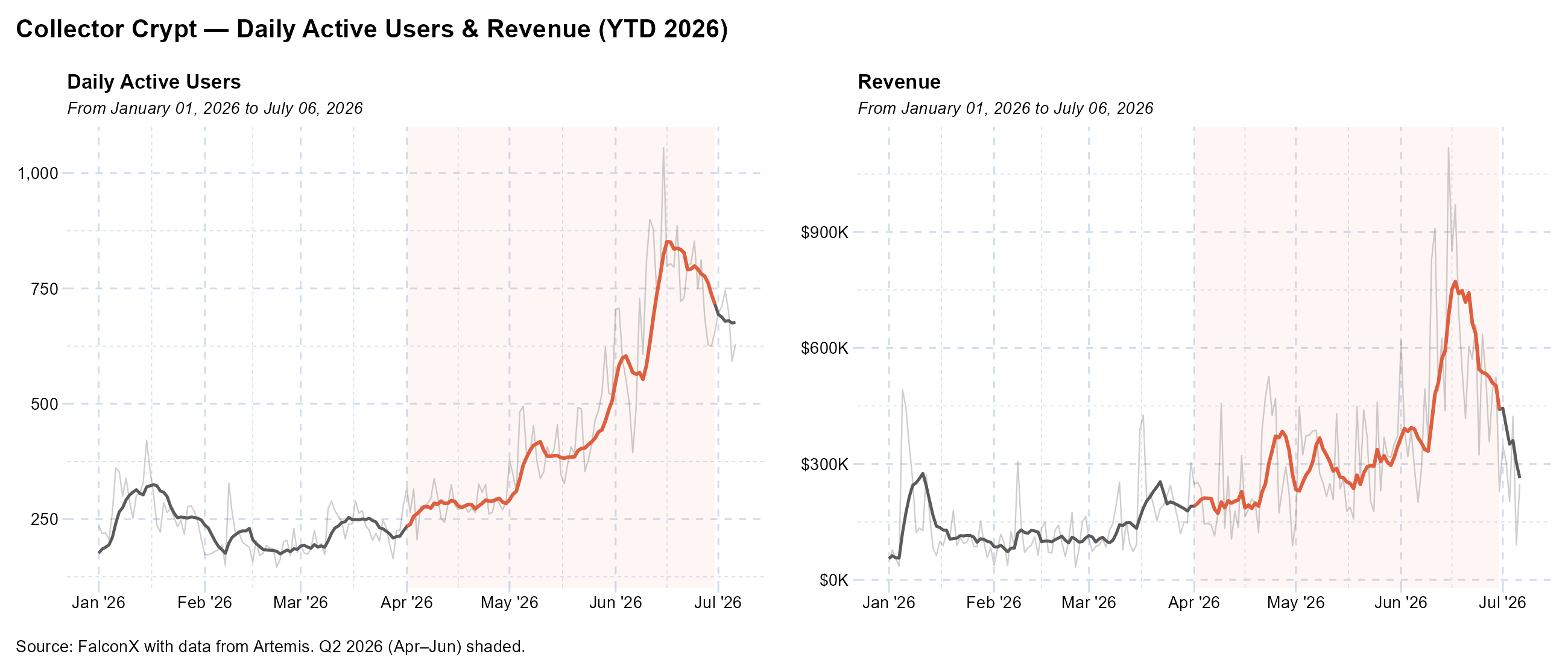

CARDS Becomes a Top 10 Crypto Protocol by Revenue

Tokenized trading card collectibles platform Collector Crypt (CARDS) was a notable performer in the quarter, with its price rising 420%, potentially reflecting growing activity on the platform. DAUs climbed to YTD highs, while daily revenue jumped to as much as $1M per data from Artemis. The activity may reflect growing demand for collectibles as well as broader accessibility unlocked by integrations. The increased activity appears to make Collector Crypt a top 10 crypto project by 30D revenue, according to DeFi Llama, suggesting that it is one to watch.

The Q3 Setup

The positioning data suggests a market that has substantially deleveraged and, in Q2, largely stopped bleeding: open interest held near its reset lows, turnover stayed subdued, and spot volumes turned up within the quarter after bottoming in May. Given MSTR’s actions to recapitalize, the fears that rippled through the crypto markets towards the tail end of the quarter now seem to be subsiding. While the summer period historically tends to be quieter in crypto, the next few weeks could deliver major catalysts, such as a Senate vote on the CLARITY act, and any improvement in ETF flows could bridge the market to a more seasonally supportive Q4. The tight Senate calendar ahead of the August recess continues to pressure odds of the act passing this year: Polymarket traders are pricing in a 47% chance as of July 7, while Kalshi traders have it at 40%, setting the stage for a key quarter.

[1] Spot exchange set: Binance, Bitfinex, Bitstamp, Bullish, Bybit, Coinbase, Crypto.com, Deribit, Gemini, itBit, Kraken, OKX

[2] Per Coin Metrics

[3] Futures set: Binance, Bitfinex, BitMEX, Bullish, Bybit, CME, Coinbase Derivatives, Coinbase International, Crypto.com, Deribit, dYdX, Hyperliquid, Kraken, OKX

[4] Same as spot exchange set

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd. nor Banzai Pipeline Limited service retail counterparties, and the information in this material is NOT intended for retail investors. This material is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this material is not and should not be regarded as investment advice, investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

No discussion of a particular company or product shall be considered an endorsement of such company or product. Past performance is not indicative of future results. FalconX, and its affiliated parties, including 21shares, may hold positions in, act as a market maker for, or otherwise have a financial interest in, assets discussed herein, and may benefit from any price movements or transactions involving the subject company. This may change without notice. Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory, and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over-the-counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a Swap Dealer with the U.S. Commodities Futures Trading Commission and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is licensed by the MFSA as a Class 2 Crypto-Asset Service Provider (Regulation (EU) 2023/1114). It is also licensed as a Financial Institution (Cap. 376) exclusively for EMT payment services.

"FalconX" is a marketing name for the FalconX Group and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.