Answering Mr. Sorkin: Untangling BTC's Behavior Amid the Recent Macro Uncertainty

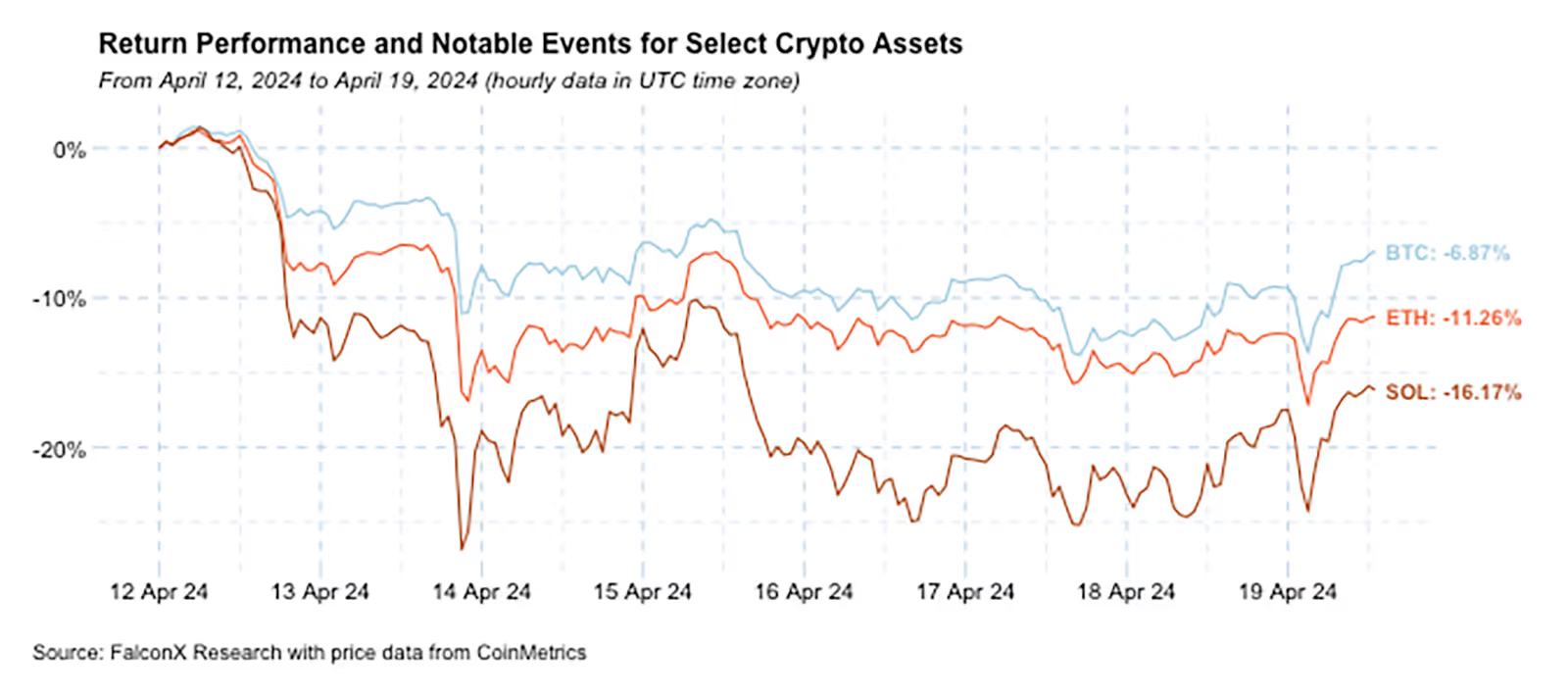

Over the past seven days, crypto assets traded relatively in sync, with none of those boasting a circulating market capitalization above $2 billion registering positive gains. Geopolitical tensions in the Middle East continue to add to a complex macro landscape characterized by persistent inflation and substantial deficits and exert pressure on prices.

The two biggest topics of the week are the impending halving and the insights we can glean from BTC's response to geopolitical escalations.

I already wrote extensively about the halving, so here is a short summary if you missed it:

This evening ET, the Bitcoin block reward will be reduced from 6.25 to 3.125 BTC per block. The direct impact on flows should be muted, given that miner revenue as a percentage of BTC traded volume has been shrinking exponentially over the cycles. That said, it’s too early to rule out an impact on prices. In a curious turn of events, the past couple of halving cycles have highlighted Bitcoin’s immutability properties during critical macro periods.

As exciting as the halving is, however, renewed geopolitical tensions dominated crypto price action over the past week.

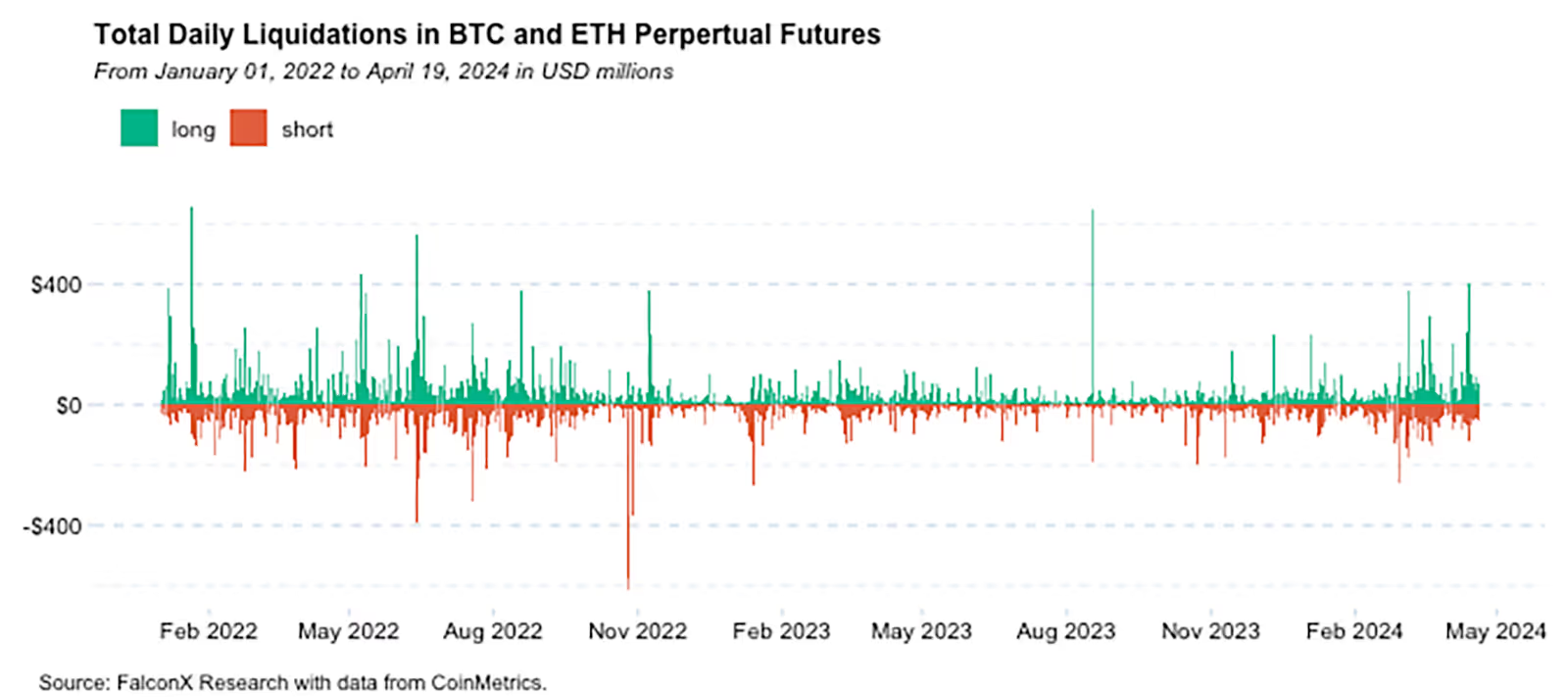

The market uneasiness that started building last Friday increased on Saturday after Iran executed an attack on Israel. The BTC price fell from the $70k range to the $60k level but recovered more than half of the drop by Monday. Perhas even more impressive than the price swing was the leverage wipe out: $645 million in long liquidations on BTC and ETH futures, earsing about $10 billion of open interest.

The second steep correction of the week occurred yesterday (April 18) following reported news of Israel’s retaliatory attacks. BTC briefly traded below the $60k mark but recovered quickly to above the $65k level on perceptions that it was a narrow attack aimed at avoiding escalation.

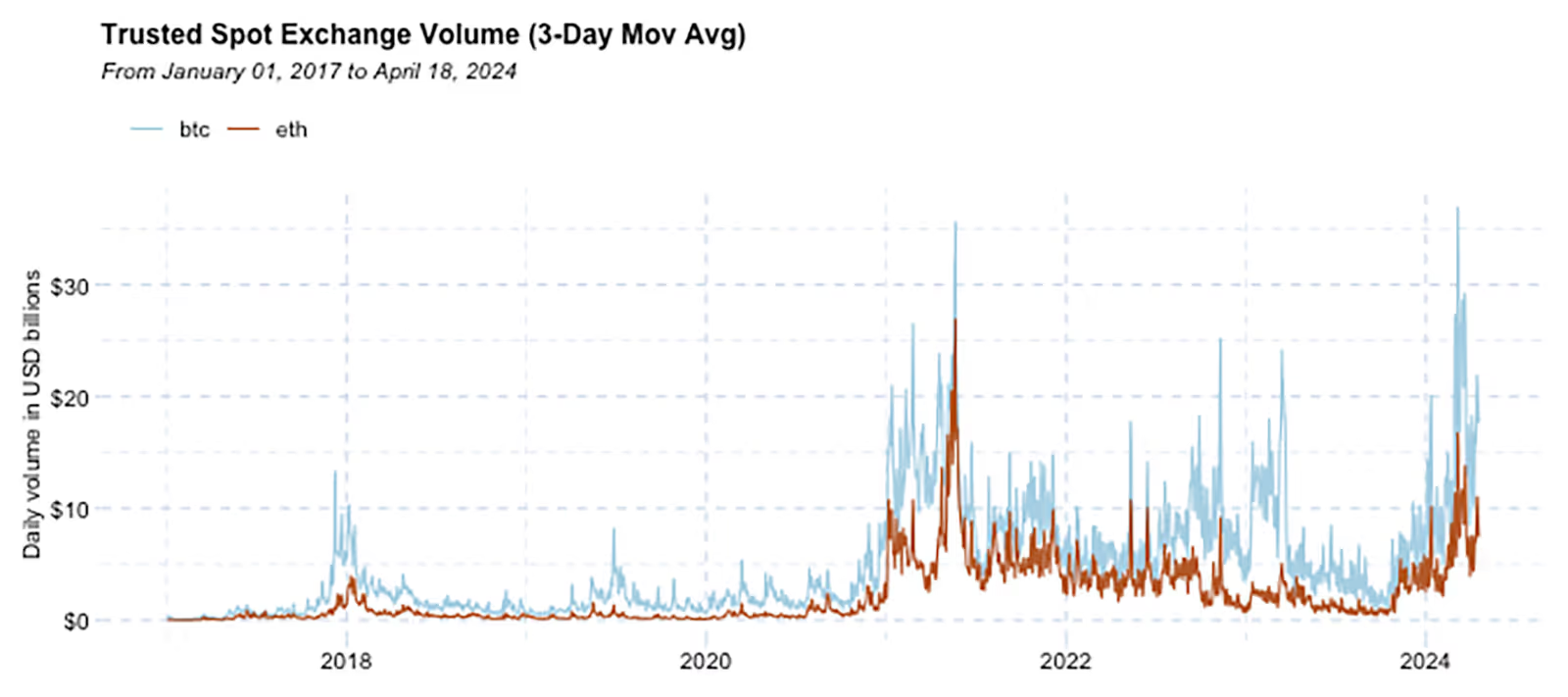

Encouraginly, both price revoveries came on the back of strong spot volumes. This is notable given that volumes, which have been on an uptrend since Q4 ‘23, have been languishing in April.

The price gyrations led market participants to revisit their BTC investment cases. The always excellent Andrew Ross Sorkin posted the following on X/Twitter:

Trying to understand Bitcoin's price movements this weekend...If it is, as Bitcoin bulls believe, a store of value, during a war, wouldn't it be a considered safe haven? And if it is a hedge against inflation, wouldn't buyers rush to it out of fear that countries will spend more on conflict? What explains its fall? I'm genuinely curious to hear various perspectives…

Despite the myriad crosscurrents currently playing out in the market, Bitcoin behaved as it is supposed to.

The important qualifier in Andrew’s description is that Bitcion is an emerging store of value commodity. Emerging commodities should not be expected to behave as established ones, but to move toward that direction over time.

This is important because if Bitcoin behaved as a risk-off asset, which it might one day once it’s broadly acknowledged as a digital and superior form of gold, a good chunk of Bitcoin’s upside will be off the table.

Moreover, Bitcoin is not a hedge against inflation in the same way that assets like Treasury Inflation-Protected Securities (TIPS), widely used commodities with low demand elasticity such as oil, or the stock of companies with pricing power.

Bitcoin is more of a hedge against the mainstream mechanisms we have to keep inflation in check. In other words, Bitcoin is outside money, or non-debt money.

This is a much more compelling value proposal, as besides gold there aren’t many assets that can fullfill this role, as Ray Dalio excellently put this week. Under the current environment of sticky inflation and high deficifts amid several other challenges for the established central banking mechanisms, the value proposition of an emerging non-debt money seems appealing.

Other Top Trends We're Watching

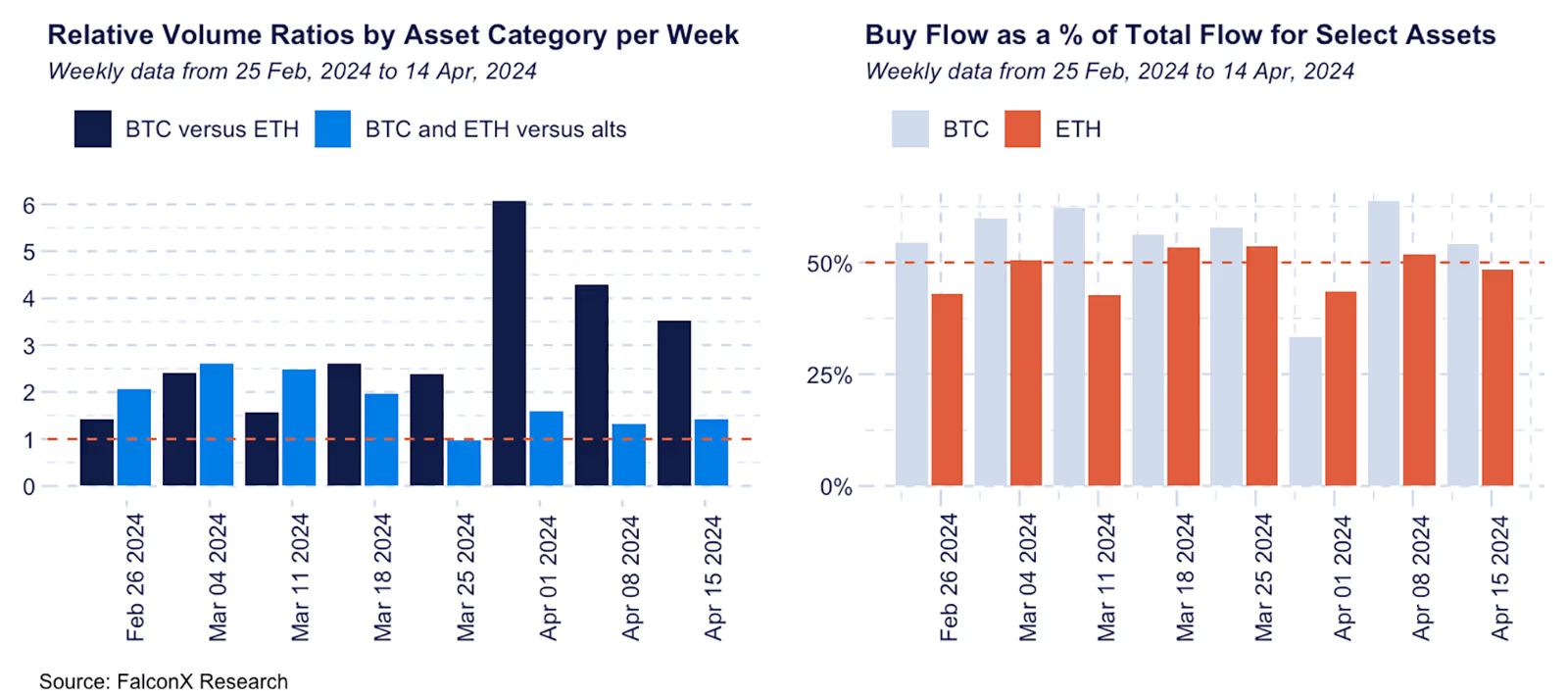

FalconX Trading Desk Color: Desk flows came from both directions over the past week, with prop trading desks on the buy side, retail aggregators slightly on the sell side, and hedge funds and VCs more heavily on the sell side. BTC remains the dominant asset, trading more than 3.5 times than ETH, but its dominance has been diminishing over the past three weeks. Pessimism around ETH continues to reflect in our desk flows, with buy/sell ratios still significantly lower than BTC’s for almost all client personas. Majors traded 1.4x more than alts, with alts activity still concentrated in relatively few names, such as SOL, NEAR, ARB, DOGE, FTM, and LDO.

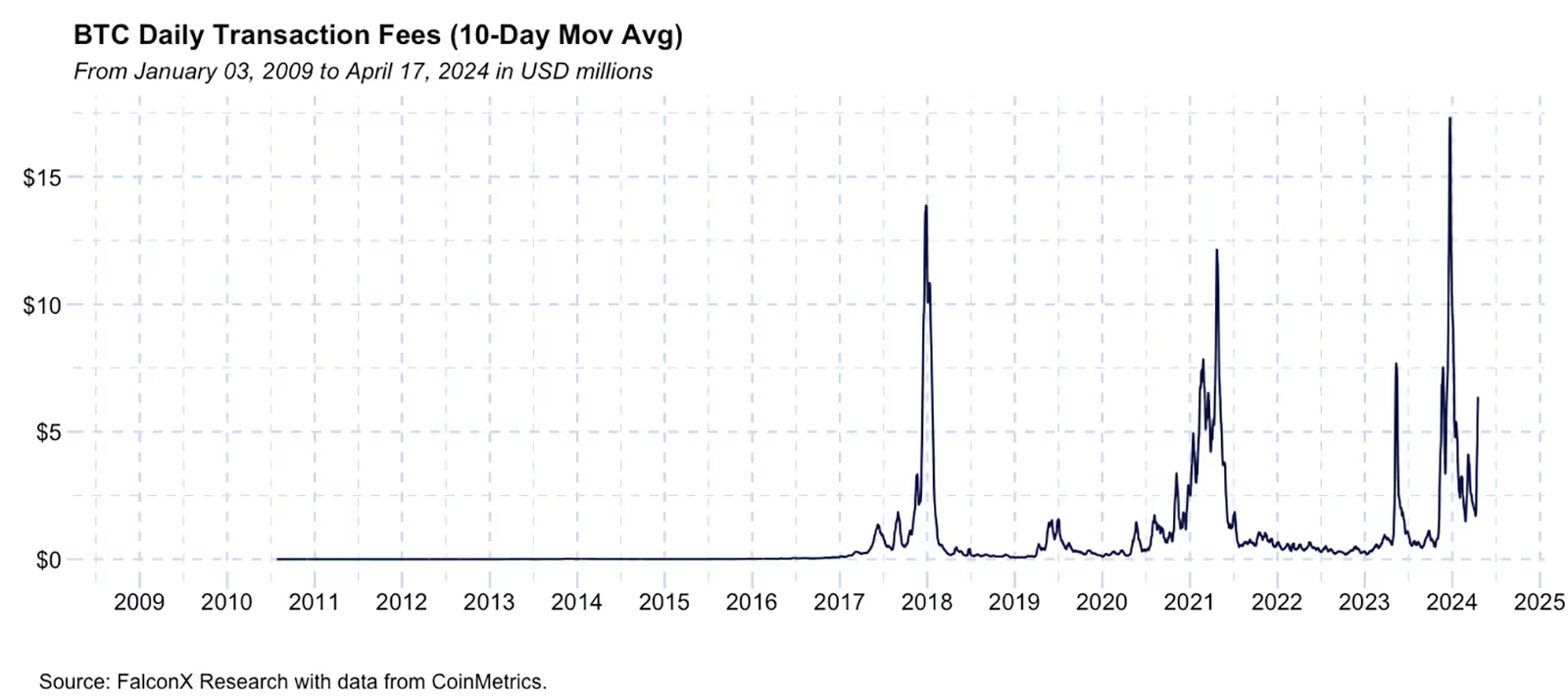

Bitcoin Transaction Fees on the Rise: Signaling a Memecoin Resurgence? Recently, Bitcoin transaction fees have consistently exceeded the $5 million mark daily. For context, such levels have been observed less than 3.5% of the time, predominantly during the peak of bull markets in 2017 and 2021 and during the ordinals/memecoin frenzies of 2023.

This new trend is likely related to Runes, the new protocol by Ordinals creator Casey Rodarmor that will launch at the Bitcoin halving. Runes are interesting because they allow for creating and transferring fungible tokens on top of BTC much more efficiently than BRC-20 tokens, which took the network by storm in 2023.

However, Runes is not alone in the race to bring fungible assets to the Bitcoin ecosystem. Taproot Assets, developed by Lightning Labs, is already operational and even just got its first non-custodial wallet and SDK. Runes, however, could still quickly build a lead given its perceived simplicity and perception of riding on the coattails of the Ordinals’ success.

Given the market's current mood, the most likely short-term use case for fungible tokens on BTC is memecoins. However, other applications, such as stablecoins, could also develop at some point.

From a longer-term perspective, the path of least resistance for Bitcoin transaction fees is likely upward. This is a positive signal of new use cases of the Bitcoin blockchain gaining steam, which is a boon to support the network security in the long term as the subsidy gets cut with each halving.

Have a great weekend!

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd. nor Banzai Pipeline Limited service retail counterparties, and the information in this material is NOT intended for retail investors. This material is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this material is not and should not be regarded as investment advice, investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over the counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a Swap Dealer with the U.S. Commodities Futures Trading Commission and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is licensed by the MFSA as a Class 2 Crypto-Asset Service Provider (Regulation (EU) 2023/1114). It is also licensed as a Financial Institution (Cap. 376) exclusively for EMT payment services.

"FalconX" is a marketing name for the FalconX Group and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.