The Transformational Potential of Hyperliquid's HIP-3

Summary

- We project incremental fees from HIP-3 builder-deployed perpetual futures markets to drive 67% upside for HYPE in the next year, led by stock and index markets.

- Staking yield for HYPE may increase as deployers of these markets pass through yield to node operators, stakers and partners (note FalconX runs a validator in partnership with Chorus One).

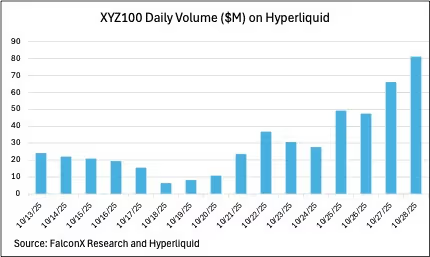

- The first HIP-3 market ‘XYZ100’ is seeing strong traction with over $80M of daily volume and open interest of $70M as of October 28.

Hyperliquid released HIP-3 on mainnet October 13, allowing for permissionless perp markets listings. This brings Hyperliquid further on par with the offerings of its centralized peers, with broader spot and perps listings now available. With perps markets on custom and traditional assets possible with HIP-3, it is one step closer to becoming the everything exchange.

The timing is convenient, with the crypto community recently questioning the steep cost and value of CEX listings, especially for TGEs. Longer term, we should see a proliferation of new on-chain markets, such as stocks and FX, on Hyperliquid, which could drive meaningful incremental revenue.

However, immediate impact will likely be muted as builders carefully construct and launch these markets to minimize potential slashing risk. Moreover, the nuances involved in the launch process may limit how quickly new perps go to market, namely a significant stake requirement and an auction process. Low hanging fruit could be perp markets on TGE token projects, while perps for traditional asset classes, such as indices and stocks, may take longer to adopt on-chain but represent a much larger TAM of trillions of daily volume.

What is HIP-3 and How Does it Work?

Hyperliquid Improvement Proposal (HIP)-3 enables anyone with a stake of at least 500K HYPE (~$25M as of writing) to launch their own perps markets on HyperCore. A deployer meeting the requirements can launch their first 3 markets for free, with any following markets subject to an auction process where deployers bid to secure a slot.

The deployer of the perp market sets parameters such as leverage limits, the oracle, etc, but runs slashing risk of up to all their stake if their actions harm the network, such as via downtime or degradation. There is a further proposal to allow validators to halt a market for reasons such as oracle misconfiguration or reliability. Considering the slashing risk, the high threshold for the amount staked is to incentivize the deployment of only high quality markets. In this case, slashed HYPE is burned; it does not go to validators. The amount required to be staked to launch a market is expected to be reduced over time.

Similar to the process for HIP-1 spot tokens, new HIP-3 perps markets are launched via Dutch auction, priced in HYPE, that run every 31 hours. In a Dutch auction, the price declines over time. The initial price starts at twice the previous successful auction’s price, or 500 HYPE if the prior auction was not successful. The auction has a minimum price of 500 HYPE (~$25,000 equivalent). Considering the first 3 markets are free to launch for a deployer, we have seen the auction process only twice so far for HIP-3 markets, with the deployer paying 500 HYPE each time to launch ‘GOLD’ and ‘HOOD’ markets. As of writing, these markets have not opened for trading yet.

HIP-3 perp markets split fees 50% between the deployer and the protocol, aligning incentives between participants, and importantly still growing the pie for Hyperliquid. Initially, overall fees are twice the fees on validator-operated perp markets, thereby the protocol will continue to receive the same fees regardless of the kind of market. Per the fee schedule here, this translates to initial base fee tiers before discounts of 3/9 bps maker/taker. The protocol aims to allow the deployer to customize their fee portion later on.

Tokenomics Implications

HIP-3 markets stand to drive demand to acquire HYPE, as any deployers will need to source and/or keep their 500K HYPE staked, effectively reducing circulating supply, and possibly driving buying demand.

The staking requirement could also support the creation of robust LST or pooling markets for deployers seeking to source HYPE to be able to launch markets. HYPE staking yield could see a lift as deployers pass back a portion of the fees to their staking bootstrappers and partners, including validators who may further pass on the yield to delegates. Considering the current HYPE staking yield is 2.2%, any significant increase could drive additional demand to stake HYPE.

Furthermore, if these perp markets see large volumes, protocol fees could grow substantially. Given protocol fees will be the same as Hyperliquid’s current markets, growing HIP-3 volumes could funnel considerable fees for buybacks, helping support HYPE’s price.

Framing the Impact

What HIP-3 really unlocks for Hyperliquid is trading traditional asset classes on-chain, such as equities, FX, and commodities. These are massive markets that have historically had little presence or activity on-chain, although that may be changing lately with tokenized stocks seeing adoption and record high gold prices driving interest in trading gold on DEXes. These traditional asset classes already do hundreds of billions to trillions of dollars of volume each day, so capturing any of this volume could be very meaningful for Hyperliquid.

Unit’s XYZ100 perp market was the first and only market to begin trading after HIP-3 was implemented on mainnet on October 13. While described as an index of 100 non-financial companies listed on a US exchange, community members suspect it tracks the Nasdaq 100. So far, traction has been strong with daily volume and open interest climbing to approximately $80M and $70M, respectively, as of Oct 28. It appears the deployer has earned over $100K in fees in less than 2 weeks, highlighting how lucrative these markets can be. The traction will likely encourage more deployers to come in quickly, but given the hurdle of sourcing stake, could lead to a smaller number of markets that are expected to generate the most volume. While the XYZ100 market is still relatively small, it is generating significant excitement from the community as an example of the kinds of markets HIP-3 unlocks.

We could also see demand for these kinds of perp listings most immediately from pre-TGE projects. Projects launching their token can benefit from a perps market as their key participants such as the team, foundation, investors, and yield farmers can use it to hedge price risk once the token is live. Moreover, these projects may not want to wait for a major exchange to list their perps markets – something that could take months or years depending on the popularity of the project. Longer tail assets could also want their own perp markets as they may be unlikely to drive enough volume for a major CEX to launch perps for them, although the staking cost here may be prohibitive.

Immediate Adoption May Prove Difficult to Achieve, But Hyperliquid Has Distribution

History suggests attracting interest in a new category of markets may prove a challenge. For example, peer dYdX rolled out permissionless perp markets in 2024, but volumes for traditional markets on its platform remains low with 24H volumes for Tesla xStock, PAX Gold, and the Turkish Lira $4K, $10K, and $0, respectively, as of Oct 29. One factor here could be that it may be difficult to line up market makers for newer markets without incentives or expectations of strong demand. Regardless, it seems that on-chain instruments for traditional markets have already been around, but may have suffered from lack of distribution.

However, Hyperliquid has already demonstrated it can attract significant interest to new kinds of markets, such as its spot markets, despite little success in applying the CLOB format to spot assets from DeFi projects in the past. With daily spot volumes of $200M+ as of Oct 27, it regularly trades more in spot than many CEXes. Doing so was no easy feat, in part because it had to get traders comfortable with Unit assets, a form of wrapped assets.

Moreover, Hyperliquid has an advantage from its distribution. As the largest perp DEX by open interest and with 44,000 DAUs as of Oct. 28, per Artemis, simply listing these new markets on its front end is likely to attract traders.

Considering this, we believe Hyperliquid can attract interest in these new offerings from its broad reach, activity, and potential incentives, such as further airdrops. In an era when experimentation with tokenization is proliferating, there is still considerable friction in trading all assets in one place and Hyperliquid stands to be the one-stop DEX that offers this.

Valuation Analysis

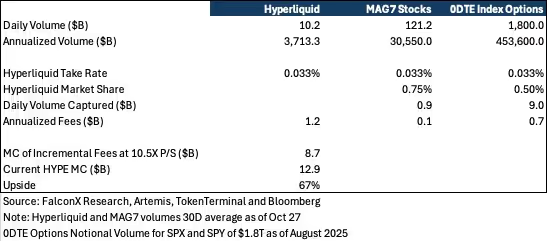

We anticipate that adding new perps markets could meaningfully contribute to Hyperliquid’s fee generation, and see perps on popular stocks and indices as the most likely to see strong demand. MAG7 stocks, popular amongst traders and making up considerable portions of leading indices, have traded $121B daily recently, which compares to daily volume of approximately $10B on Hyperliquid. We see this volume as a conservative proxy for day traders, as options trading on single-name stocks could be more meaningful.

Moreover, we believe 0DTE options for indices are another potential market Hyperliquid can tap into by offering leverage on index perps. Per Bloomberg Intelligence, notional volumes of SPX and SPY (S&P 500) 0DTE options alone totaled over $1.5T/day in March 2025 and an average of $1.8T in August 2025. Options on QQQ (Nasdaq 100) also see considerable activity, further growing the TAM for leveraged trading on Hyperliquid.

We apply conservative estimates to the market share Hyperliquid could take from each segment. Just capturing 0.75% of MAG7 volumes would represent daily volumes of $0.9B, something that does not seem out of reach considering volumes on the rest of its markets. On the index side, we believe Hyperliquid could take up to 0.50% of flow going to 0DTE options for indices, resulting in daily volumes of approximately $9.0B. Given Hyperliquid’s only live HIP-3 perp is already seeing $80M+ of daily volume just 2 weeks after launching, we believe such volumes could be attainable over the next year given the launch of more markets.

Hyperliquid currently has a take rate of 3.3 bps (Fees/Volume), and nearly all fees go to the bottom line, going towards HYPE buybacks. Consequently, we project HIP-3 markets could conservatively drive an incremental $0.8B of annualized fees within a year, representing upside of 67% from current levels using Hyperliquid’s latest P/S of 10.5X, equating to a HYPE price of $80. We note the opportunity could even be larger if perps on forex, commodities, and other custom instruments become popular.

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd. nor Banzai Pipeline Limited service retail counterparties, and the information in this material is NOT intended for retail investors. This material is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this material is not and should not be regarded as investment advice, investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over the counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a Swap Dealer with the U.S. Commodities Futures Trading Commission and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is licensed by the MFSA as a Class 2 Crypto-Asset Service Provider (Regulation (EU) 2023/1114). It is also licensed as a Financial Institution (Cap. 376) exclusively for EMT payment services.

"FalconX" is a marketing name for the FalconX Group and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.