Hyperliquid’s Stablecoin USDH Bidding War: One of the Most Interesting Live Experiments in Crypto

Hyperliquid's decentralized exchange is auctioning its reserved USDH stablecoin ticker, with Paxos, Ethena, and Native Markets competing to challenge USDC's $5 billion dominance on the platform. The bidding war highlights crypto's community-driven governance as validators prepare to vote on September 14, with the winner facing the task of displacing entrenched stablecoin incumbent USDC.

The lemma “not a boring day in crypto” remains undefeated. After an unusually active summer with DATs exploding (driving ETH outperformance) and macro debates centered on monetary policy and central-bank independence, crypto has, yet again, found a new, attention-grabbing storyline.

The theme of the moment is Hyperliquid’s stablecoin auction, USDH. This one is likely to reverberate for a while because it’s interesting on multiple levels.

For those not following, a quick recap: Hyperliquid, the decentralized exchange that has taken the crypto trading world by storm, generating over $120 million in monthly revenue in less than 18 months since launch, is auctioning its reserved USDH stablecoin ticker. USDH is intended to rival USDC, the stablecoin most used on the exchange thanks to its early Arbitrum bridge, the default gateway to the DEX behemoth.

The stakes are high: roughly $5 billion of USDC sits on Hyperliquid, which, on a back-of-the-envelope calculation, implies about 10% of Circle’s business (or about $200 million in annual revenue) comes from this. The Hyperliquid Foundation aims to stir things up by auctioning its reserved USDH ticker to the bidder who can add the most value to the ecosystem rather than letting that yield accrue externally.

The auction format is straightforward: Proposals were due Sept 10, 10:00 UTC, validators state their intended votes by Sept 11, 10:00 UTC, and validators cast final votes on Sept 14, 10:00–11:00 UTC, therefore giving users time to make sure they are staking with a validator that matches their preference.

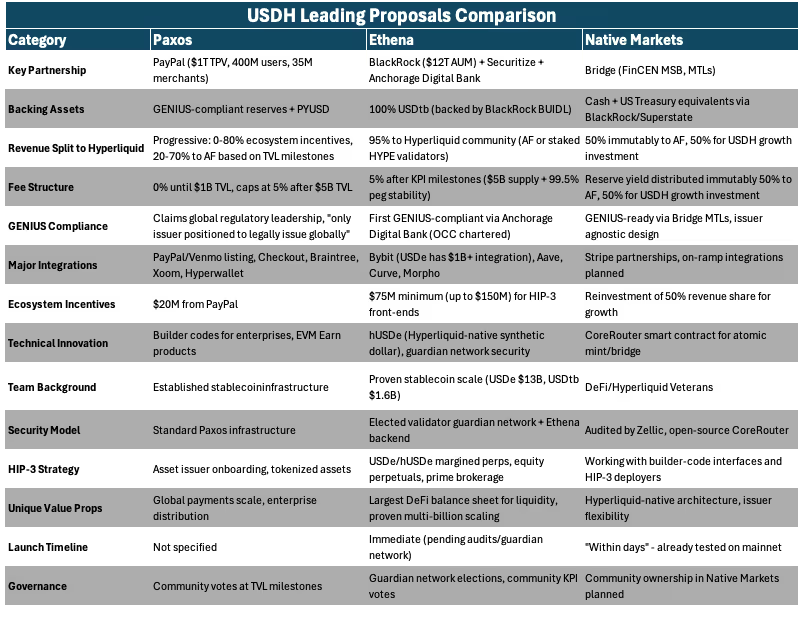

Unsurprisingly, the process has attracted many of the leading stablecoin teams, centralized and decentralized alike. Below, we summarize the proposals from the three leading contenders as measured by engagement in Hyperliquid’s Discord channel.

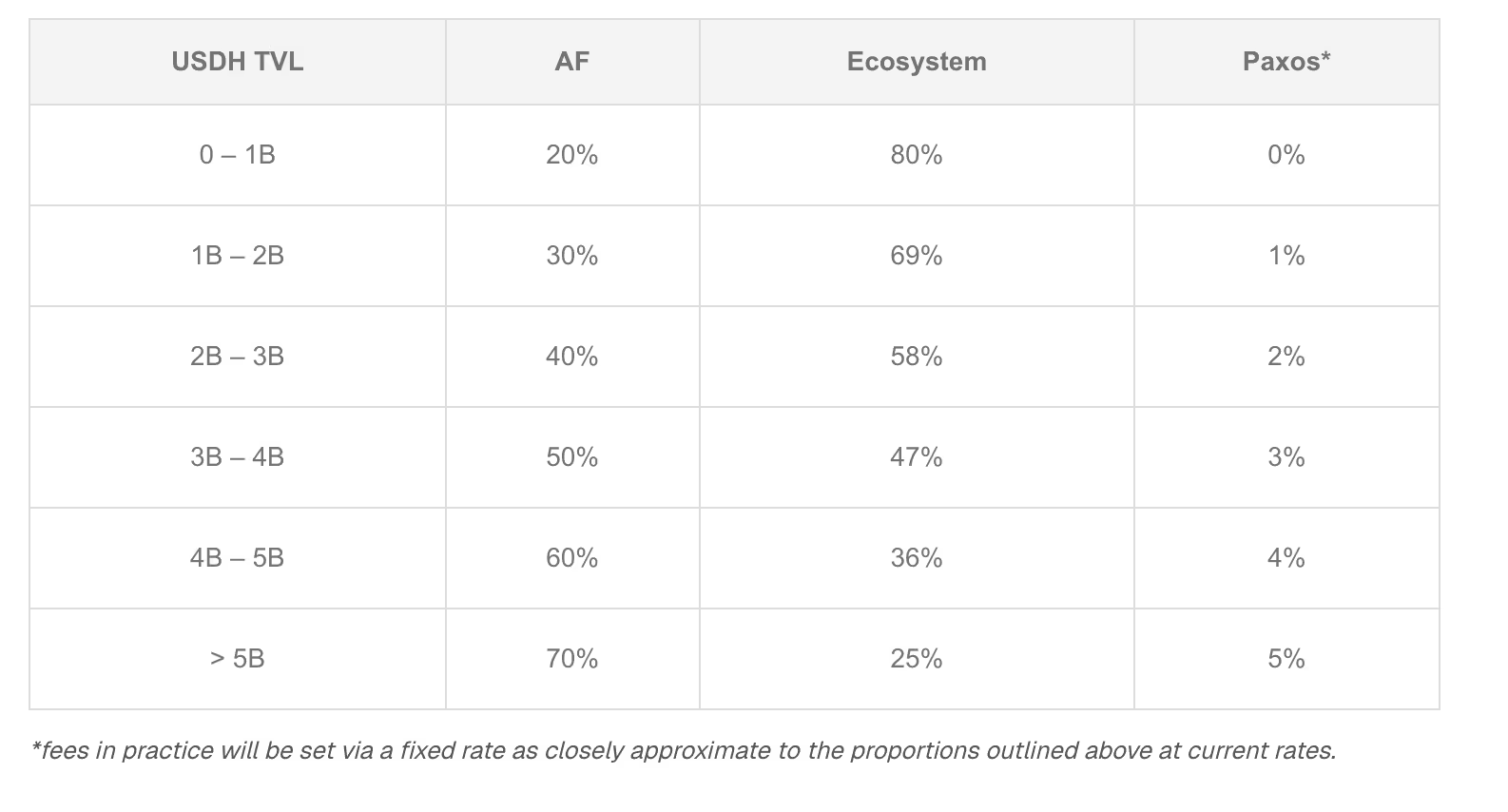

- Paxos: Leveraging a track record of launching and scaling regulated stablecoins (Binance USD to $25B+, PayPal USD to $1B+, and $160B+ in cumulative issuance) Paxos is a top contender. After an initial offer covering both HyperCore and HyperEVM deployments, multi-jurisdictional issuance with GENIUS and MiCA compliance, and a 95% interest-revenue share, Paxos upped the ante last night.

The updated proposal includes: support from the PayPal/Venmo ecosystem (HYPE listing and free USDH on/off-ramps), $20M in ecosystem incentives, global payments integrations across multiple networks, and a revenue-sharing schedule that starts at 100% to Hyperliquid and steps down linearly with TVL, capped at a 5% issuer share once TVL reaches $5B.

- Ethena: A strong bid from one of crypto’s fastest-growing and most impressive ecosystems. USDe now has a market cap of over $13B, and Ethena reports $23B in cumulative mints/redemptions of tokenized USD assets with zero security incidents or downtime.

The highlights include: USDH backing by USDtb, the first GENIUS-compliant payment stablecoin (itself backed by BlackRock’s BUIDL tokenized money-market fund); commitment to deploy ≥95% of net revenue via HYPE purchases and Assistance Fund contributions; coverage of USDC to USDH migration costs if existing USDC pairs are re-denominated to USDH; launch of Securitize (tokenization platform) on HyperEVM, plus many more relevant features (full list here).

Notably, these commitments are not contingent on winning the USDH bid. Ethena says it will build on Hyperliquid regardless.

- Native Markets. While the brand may be newer to some, the team includes respected operators and investors such as Max Fiege (Hyperliquid ecosystem), Anish Agnihotri (research/engineering; ex-Paradigm, Polychain), and MC Lader (former President/COO of Uniswap Labs; ex-BlackRock, Goldman Sachs).

The proposal features a partnership with Bridge (Stripe’s stablecoin issuer), HyperEVM launch with seamless interoperability to HyperCore, fully backed reserves comprised of cash and U.S. Treasury equivalents, with off-chain reserves managed by BlackRock and on-chain reserves by Superstate via Bridge, reserve yield (not just net revenue) notably split equally between an autonomous, immutable stream to the Assistance Fund (ie, HYPE buybacks) but also in investment in USDH ecosystem growth.

The table below compares the three main proposals across select key factors.

Over the next few days, all eyes will be on who is going to take this bidding war.

Even if the validators are supposed to disclose their intended votes by tomorrow, the focus should be on whether stakers will move across validators that are more aligned with their votes until the final vote on September 14. Polymarket is now attributing strong odds to Native Markets, which is seen as the embedded ecosystem members (more on that later), followed by Paxos and then Ethena.

Whatever the outcome, the primary beneficiary of this bidding war is the Hyperliquid ecosystem. Note that this is simply the auction of a reserved ticker. Any stablecoin issuer can still build on Hyperliquid via the standard ticker-bidding process, as some have said they’ll do regardless.

First, market structure and liquidity. For anyone focused on market structure, liquidity, and collateral, the coming months will be busy. How will USDH compete with USDC, especially given Circle has said it’s doubling down on Hyperliquid by deploying native USDC with seamless interoperability via its cross-chain messaging protocol? And USDT0 (Tether’s omnichain stablecoin) has also stated its intention to keep building on Hyperliquid despite not bidding for USDH.

Some will recall when Binance incentivized other stables (BUSD, and notably FDUSD) over USDT a few years back. That push didn’t last, thanks in part to the bear market, but it showed how hard it is to dislodge an incumbent stablecoin. The context is different on Hyperliquid, but it will be fascinating to see how this whole dynamic plays out, and it should be anything but easy for the USDH bidder winner.

Second, community-driven governance in the open. This community-led, live RFP spotlights one of crypto’s most interesting, yet sometimes underrated, features: a community’s ability to move its shared ecosystem forward.

This process is of course not always tidy. Some argue the process is favoring Native Markets, noting the team’s proposal appeared just hours after the auction announcement. Others point out that it has been known for some time that the reserved USDH ticker would eventually be auctioned, and that someone as deeply embedded in the ecosystem as Max Fiege could reasonably have anticipated it and prepared over weeks or even months. Still others note that governance is functioning as intended, not least because stakers have time to delegate to validators aligned with their preferences.

Finally, an orthogonal, but related and noteworthy development: Polymarket spun up a prediction market on the auction with remarkable speed. After I asked on social media why no market for this existed yet, the team launched one in under two hours, and within 48 hours, about $1.5 million was at stake. If anything showcases how prediction markets are the future and how crypto-enabled applications can interact with one another to drive positive outcomes or produce useful signals, this does.

Hyperliquid.

"In the spirit of transparency and disclosure, FalconX, along with our partner Chorus One, runs one of the most recently added validators on the Hyperliquid network. We will be submitting a vote determined by our staking clients to best represent their interest."

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd. nor Banzai Pipeline Limited service retail counterparties, and the information in this material is NOT intended for retail investors. This material is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this material is not and should not be regarded as investment advice, investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over the counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a Swap Dealer with the U.S. Commodities Futures Trading Commission and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is licensed by the MFSA as a Class 2 Crypto-Asset Service Provider (Regulation (EU) 2023/1114). It is also licensed as a Financial Institution (Cap. 376) exclusively for EMT payment services.

"FalconX" is a marketing name for the FalconX Group and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.