From Opinions to Odds: Emerging Trends in the Prediction Market Landscape

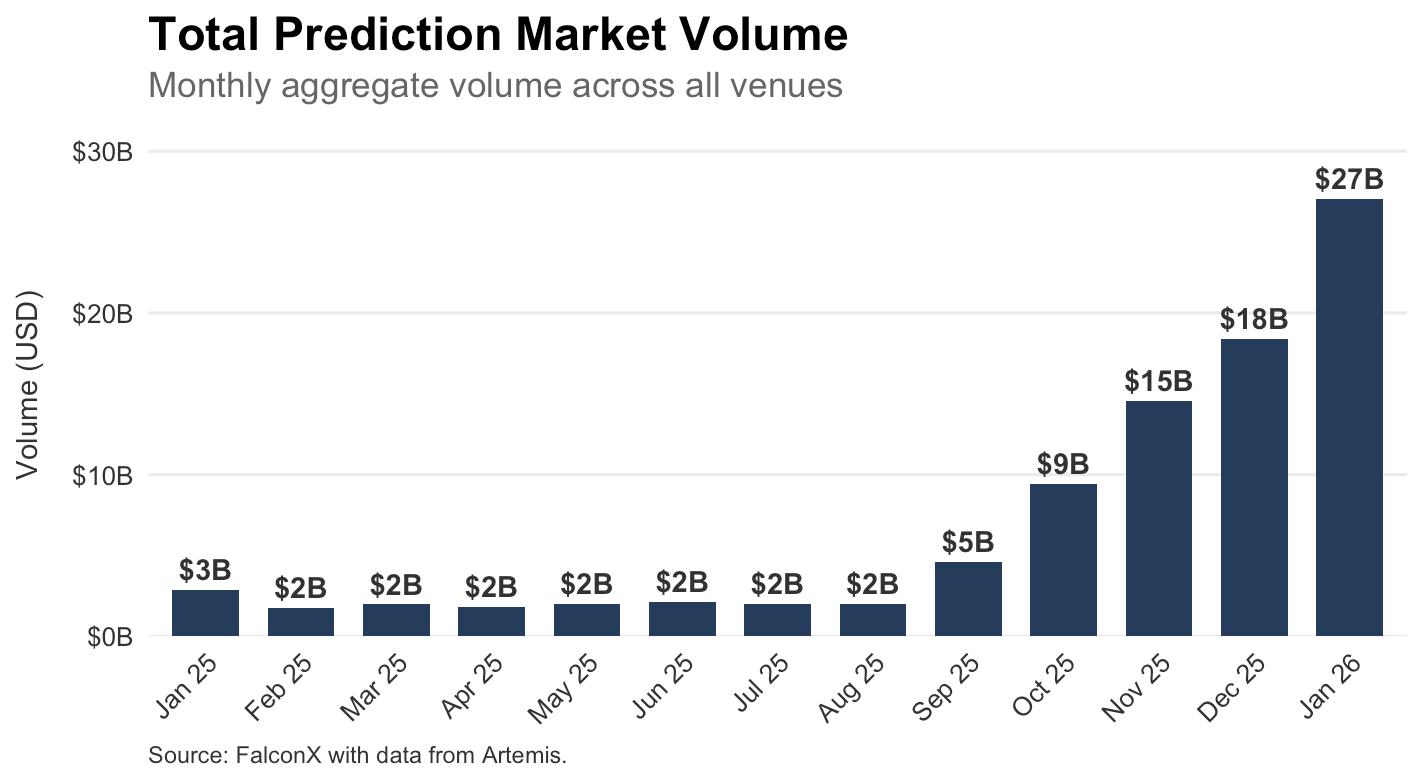

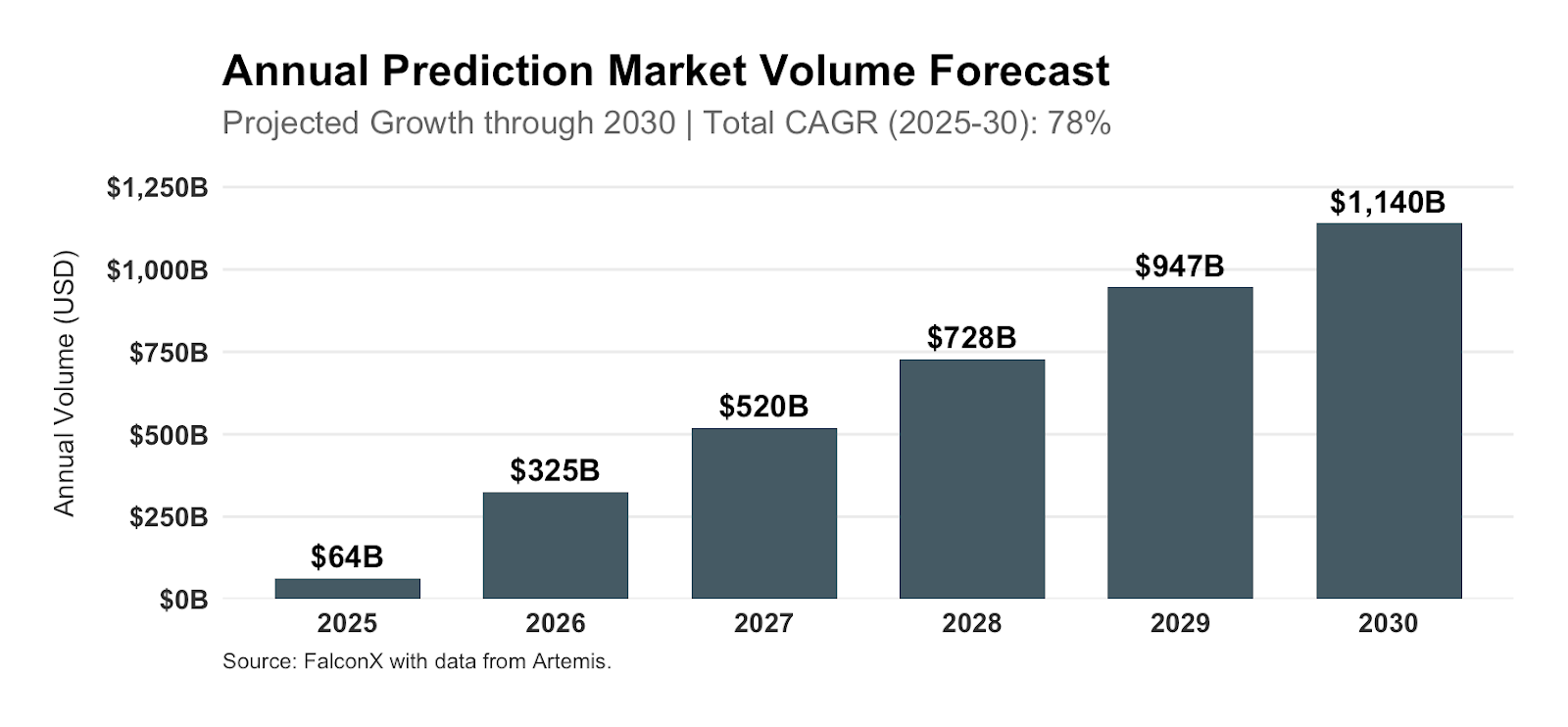

Prediction market volumes grew nearly 4X sequentially to $64B in 2025 and are on pace to exceed $325B in 2026, based on YTD run-rate volumes. Drawing parallels to the early growth of perpetual futures, we estimate volumes could exceed $1.1T by 2030.

Prediction markets enable participants to wager on the outcome of events. They are popular for both their variety and unique structures, and for providing traders the ability to hedge and speculate on real-world events that are not offered as markets elsewhere. Moreover, participants may appreciate the other side of these markets are other traders rather than a house with fixed odds. Popular market categories today range from sports, politics, business, elections, and culture, highlighting the broad depth of these markets.

Importantly, prediction markets have demonstrated the ability to surface more precise event probabilities than polls or experts, suggesting that monetary skin in the game can drive more accurate results in real-time. This has been attributed to the ‘wisdom of the crowd’. Consequently, prediction markets have since found applications in several industries, such as media, finance, and politics.

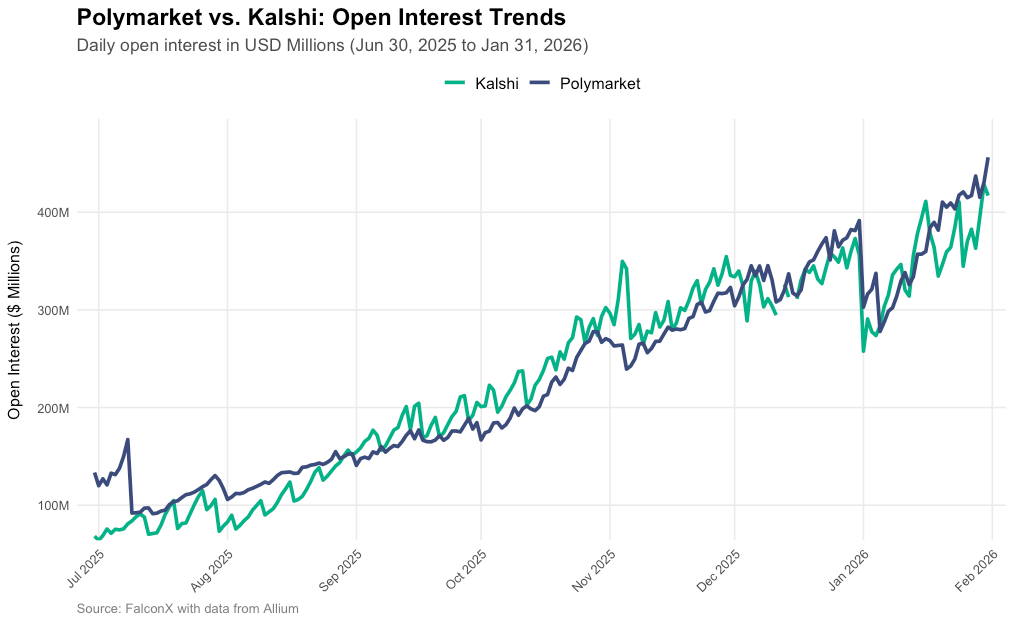

Polymarket and Kalshi are the two leading prediction markets by open interest, both neck and neck at roughly $400M OI as of Jan 31, 2026, according to data from Allium. For the month, Kalshi posted volumes of $9.5B, while Polymarket saw volumes of $3.3B.

Structure

Event contracts on prediction markets may have multiple options, each with a binary outcome. These outcomes can be structured in several ways such as Yes/No, Long/Short, Up/Down, Bull/Bear, Above/Below, Over/Under, In/Out. For example the event “Who will Trump nominate as Fed Chair?” has multiple options, each priced as Yes/No outcomes. Each Yes/No outcome is priced out of $1.00 (such as YES at $0.99 and NO at $0.01), effectively translating into odds, with the correct outcome settling at $1.00. Importantly, these are fully collateralized.

It is also possible to have events that bundle several independent outcomes. Polymarket calls these ‘Parlays’, as commonly referenced in the sports industry, while Kalshi calls these ‘Combos’.

The Two Largest Prediction Market Venues: Kalshi and Polymarket

Kalshi Overview

Kalshi is a CFTC-regulated exchange structured as a central limit order book (CLOB) with off-chain components. It was founded in 2018 and had its public launch in 2021. Founders Tarek Mansour and Luana Lopes Lara are both MIT alums with backgrounds at financial firms including Goldman Sachs, Citadel, and Bridgewater.

The firm approached the CFTC early on, intent to build in a regulated manner from the start. This culminated in receiving status as a designated contract market (DCM) in 2020, making it the first fully regulated U.S. exchange for event contracts. This designation requires Kalshi to comply with strict rules for considerations such as settlement source and susceptibility to manipulation for its event contracts. It also requires certain controls, market surveillance, and an integration with the clearinghouse to be in place. Because of its federally regulated status, Kalshi can tap into the U.S. banking system, enabling USD deposits, and can receive orders from other Future Commissions Merchants (FCMs), enabling integrations from other brokers. In 2024, Kalshi won a landmark legal case against the CFTC, allowing them to offer contracts on elections.

Since then, Kalshi clinched an $11B valuation with its latest raise of $1B in December 2025. Backers include Paradigm, Andreessen Horowitz, and Sequoia.

Kalshi offers several kinds of markets, such as binary outcomes (Yes/No), multiple-choice, continuous forecasting (numerical targets, ranges), and conditional markets (if/then events). Kalshi uses a predefined official source for market resolutions.

Kalshi has a minimum tick size of $0.01 (1 cent). This effectively means the minimum probability for an event is 1%, which may cause challenges for tail events (ex: an event with a probability of 0.2% is priced at 1%). The platform is addressing this, with documentation showing prices will be transitioning to at least 4 decimal points. Furthermore, Kalshi plans to support fractional trading of contracts in the future. Such changes are similar to prior SEC efforts in equities for more granular tick sizes, on the notion smaller ticks lead to more competitive pricing.

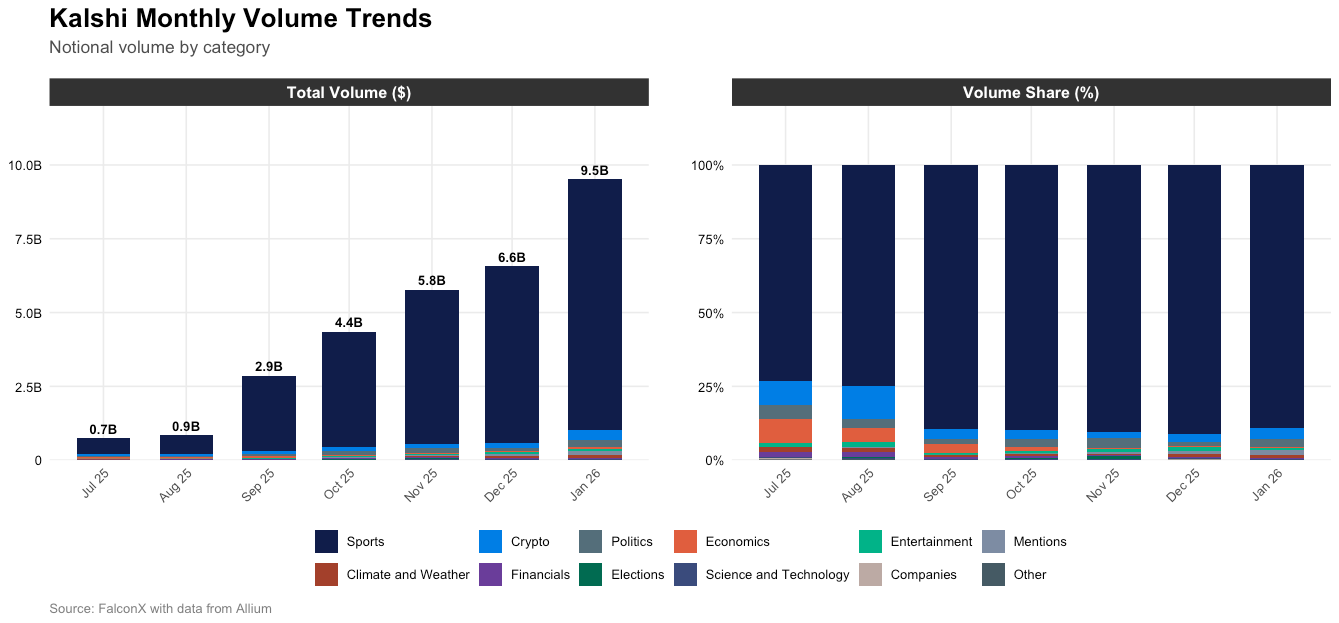

Kalshi volumes are overwhelmingly on sports events, relative to other categories. In recent months, sports-related volumes have totaled approximately 90% of its total notional volumes, followed by crypto, entertainment, and politics. Interestingly, sports only comprised ~80% of its number of trades, suggesting users are trading larger amounts relative to other markets.

This may be explained by its history that leaned toward sports contracts as a more conservative option for vetting with the CFTC, given arguably clearer parameters and event resolutions. It can also be argued that sports-related events are already a large, vetted market with massive public companies such as FanDuel and DraftKing involved, making sense to focus there given its significant size. FanDuel’s parent company, Flutter, has previously estimated that iGaming could be a $70B market in North America alone by 2030. Potentially greater growth could come from new categories that are still nascent today, such as politics, financial events, and social/cultural events.

Kalshi saw a clear acceleration in demand for sports markets relative to other categories from September 2025 onward, driven in part by a lower relative share of crypto and entertainment market activity. Around this time, daily questions traded for sports nearly doubled from prior months, although sports as a share of notional volume only trended from ~75% to 90%, suggesting smaller bets were driving the activity.

Kalshi charges taker and maker fees on its markets, although these can vary by market. It uses a dynamic formula that charges higher fees when odds are uncertain (ex: Yes/No at 50 cents) and less when the outcome is clear (ex: 99c for Yes).

Top Markets on Kalshi

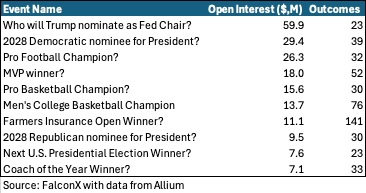

As of Jan 31, the top 10 event markets by OI included ‘Who will Trump nominate as Fed Chair?’, followed by ‘Democratic nominee for President in 2028?’ and ‘Pro Football Champion?’. Sports events dominate the top markets, highlighting the popularity of these.

We find that the activity is concentrated in a set of markets, with the top 3 markets comprising nearly 30% of total Kalshi OI and the top 10 comprising nearly 50%. These markets tend to have many different outcomes available, although a smaller set of outcomes tend to see meaningful volumes.

Kalshi Event and Spread Analysis

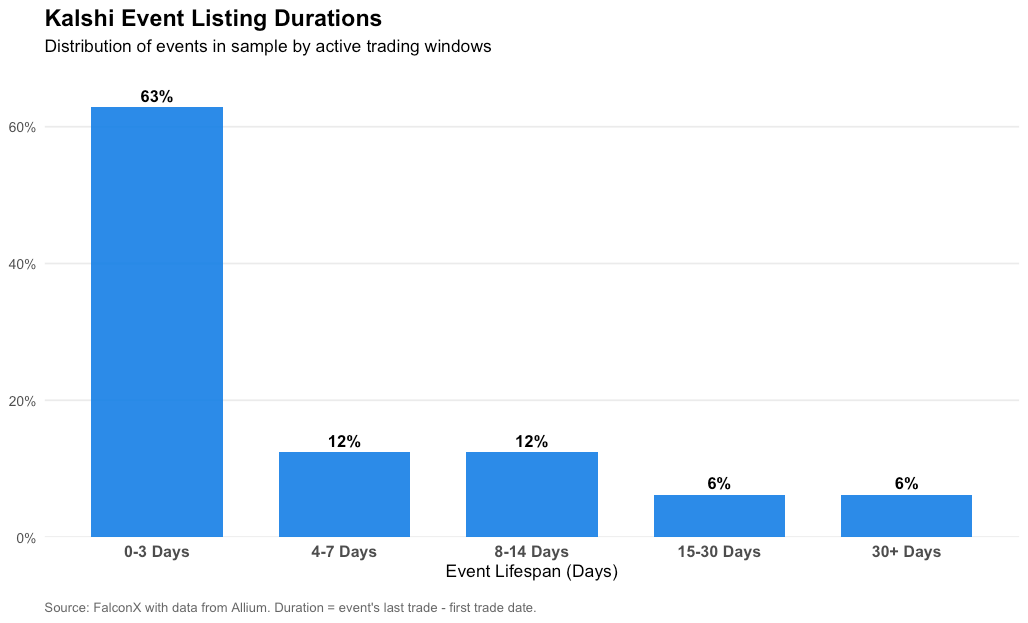

Using data from Allium, we pulled the top 100 Kalshi events by volume that concluded in January 2026, excluding ‘Combos’, and analyzed activity and spread trends. The sample set indicated close to 60% of these contracts were listed within 3 days ahead of the event resolution date, while over 80% were listed within 2 weeks of the event date. This might reflect the cadence of sports matches, where the lineup may not be known far in advance, and interest in trading these would likely occur closer to the event date.

Across the sample, we see a consistent pattern of spreads declining over time, approaching the 1 cent tick limit on Kalshi. Markets tended to have higher spreads shortly after launching, with spreads generally declining as liquidity built up. The chart below shows median spreads for markets in the sample set 7D and 3D ahead of resolution, filtering for markets that had trading history for at least that period. That data suggests that more mature markets (around for 7D+) tend to have spreads closer to the $0.01 level, while the greater number of markets launching in the 0-3D period drive up median spreads for the cohort, although these eventually converge closer to $0.01 as well.

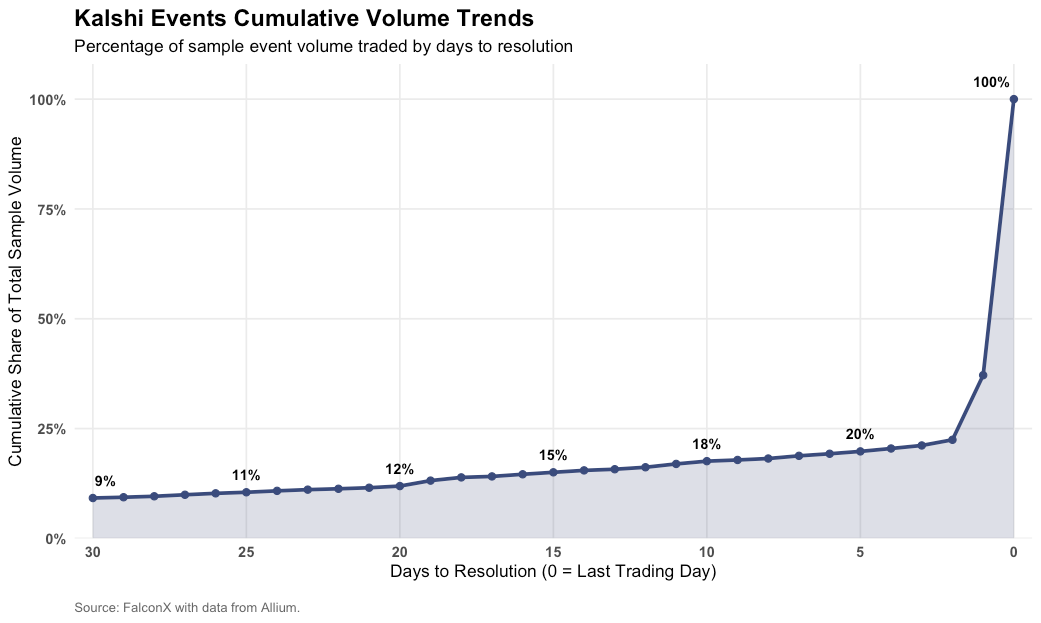

Volume wise, across the sample, we find that around 60% of volume for these markets occurs on the final day of trading (likely around or before the sports event taking place). Worth noting are longer tail markets seeing some volumes well ahead of time, with the set seeing 9% of volumes by day 30D.

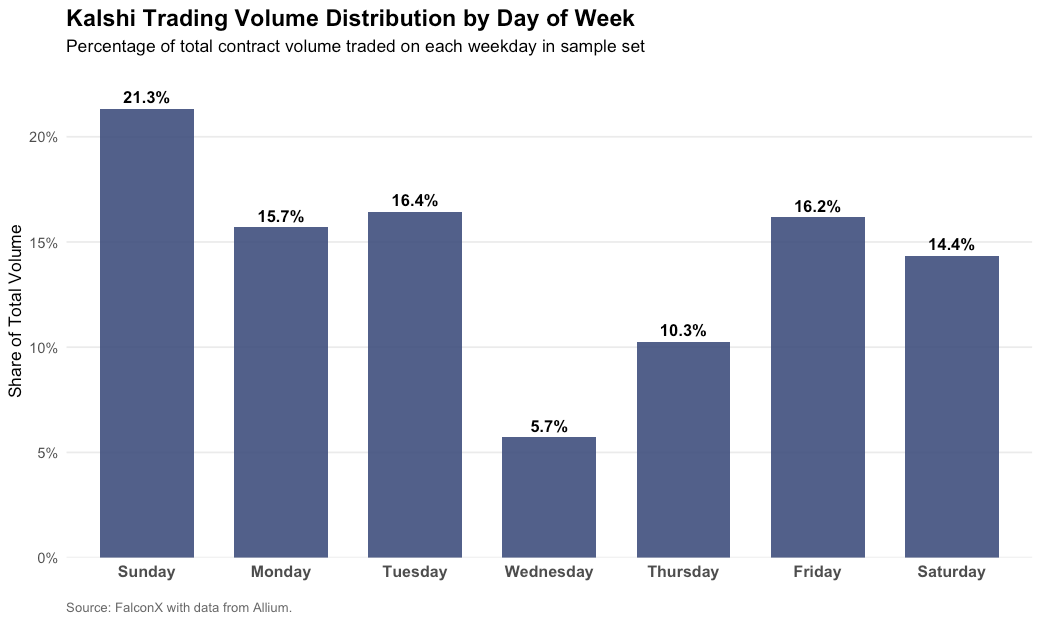

Moreover, the weekend drove strong volumes across the sample set, with Sunday driving 21% of volumes in the month. This suggests that users may have a preference to engage outside of work, or trading was driven around weekend events, such as NFL Sunday Football. Keep in mind it is possible for some events to conclude the day after sports events finish given timing adjustments and any potential game delays.

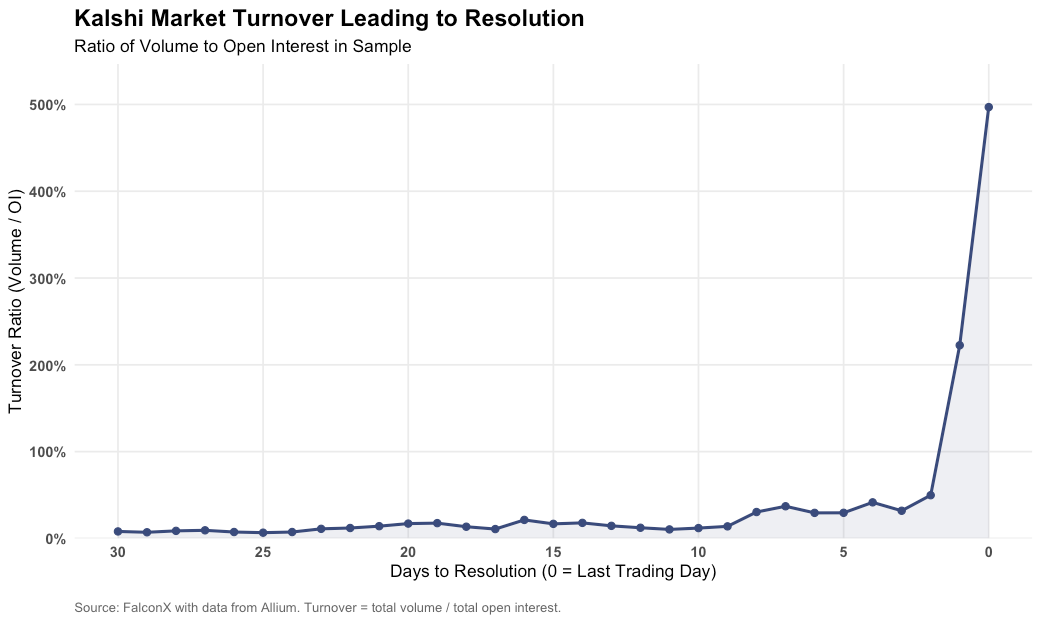

Volume turnover ramps up considerably in the 3 days leading up to resolution. In the sample set, turnover (volume/OI) jumped to 200-500% 1 and 0 days ahead of event resolution, respectively. Some of this may be explained by traders closing positions leading into or during the event, leading to lower OI at close.

Polymarket Overview

Founded in 2020 by Shayne Coplan, Polymarket has since grown to one of the largest prediction markets. It made waves after announcing an investment from NYSE parent Intercontinental Exchange for $2B at a pre-money valuation of $8B in October 2025. Other backers include Founders Fund, Dragonfly Capital, and Vitalik Buterin. Coplan dropped out of NYU to build crypto projects, before eventually founding Polymarket. His background may help explain Polymarket’s crypto-first architecture. While its international platform is on-chain, Polymarket’s US platform is off-chain, in part to meet regulatory requirements.

In contrast to Kalshi’s regulation-first approach, the CFTC had fined Polymarket in 2022 and forced it out of the US for operating as an unregistered exchange. This may have led it to adopt a stablecoin model for its otherwise offshore markets. Despite the setback, Polymarket emerged as a leading barometer of the shifting political winds in the 2024 US Election, seeing billions in volume. In September 2025, the CFTC granted Polymarket approval to relaunch in the U.S. market, following its $112M acquisition of CFTC-licensed derivatives exchange and clearinghouse QCEX in July 2025. In November 2025, the CFTC approved Polymarket to onboard brokerages and customers directly and facilitate trading on U.S. venues, helping expand integrations. In January 2026, Polymarket announced a partnership to distribute its data across Dow Jones consumer platforms, which followed Bloomberg integrating Polymarket data in its Terminal in 2024. As of early February 2026, Polymarket is still gradually rolling out its US offering via waitlist. Polymarket’s international platform currently operates on Polygon PoS, an L2 built on Ethereum, with all core activities recorded on-chain, enabling transparency and verifiability. It leverages USDC for its platform, with all markets denominated in USDC, which it says supports global reach. All shares of a market (Yes/No) are collateralized by $1.00 of USDC. Polymarket uses a central limit order book (CLOB) for its markets. It has tick sizes of up to $0.0001, and therefore can deliver low spreads through such granularity.

For event resolution, Polymarket uses UMA and Chainlink as oracles. UMA is useful for determining outcomes to more ambiguous events, while Chainlink can provide deterministic prices/outcomes for financial events for example. Smart contracts then redeem winning shares for USDC.

While users cannot create their own markets, they can submit ideas for the markets team to review.

Polymarket’s international offering does not charge trading fees except on select markets such as its 15-minute crypto markets. It charges a 10 bp taker fee on its US platform. Polymarket’s relatively low fees, especially on its international platform, help drive competitive pricing and make it stand out relative to peers.

Notably, Polymarket has a 3-second delay on the placement of market orders on sports markets, joining peers like Crypto.com in doing so, per Bloomberg, which also reported Kalshi as considering similar moves. These delays can help market makers avoid being picked off by traders with real-time data (such as being physically at sporting events), helping them keep spreads tighter.

Polymarket Trends Analysis

Polymarket volumes cover many categories, but are primarily driven by sports, politics, and crypto events. Volumes have exploded along with DAUs in recent months. Polymarket saw a high of nearly 100K DAUs in January 2026, per data from Allium.

The top 10 active markets by open interest as of January 31, 2026 skewed towards politics. These markets alone made up approximately 25% of total open interest on the platform.

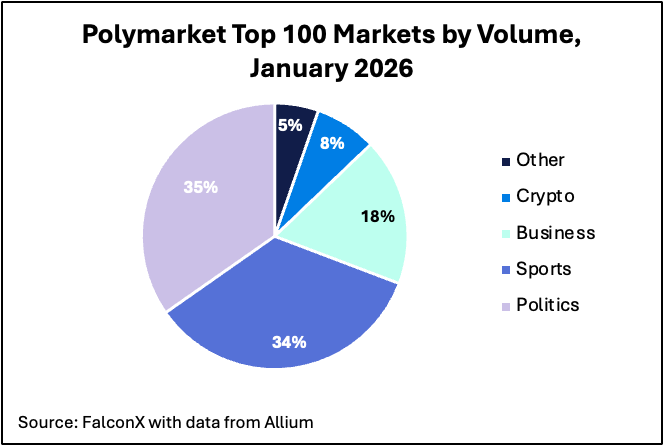

An analysis of the top 100 markets by volume in January showed diversity in categories traded, with politics and sports driving the majority of volume.

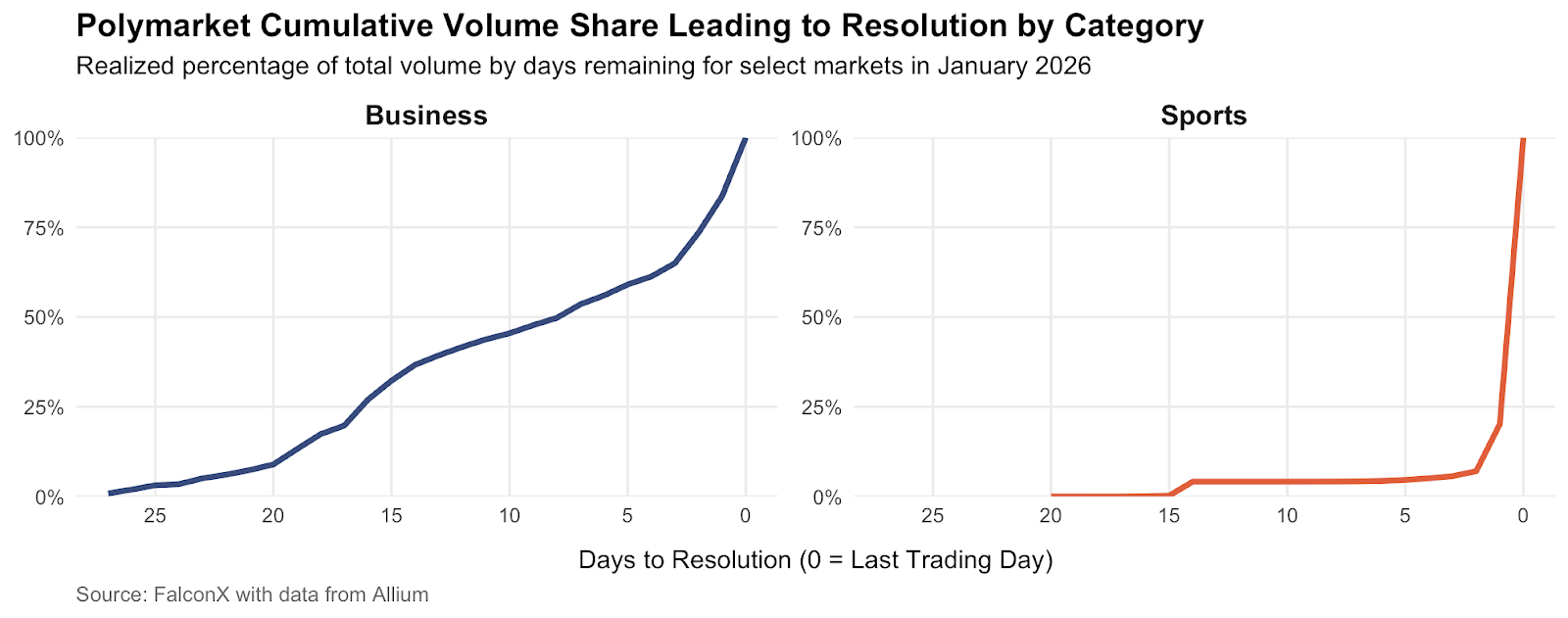

Moreover, we saw similar volume trends to that of Kalshi. Volumes in aggregate would spike in the days leading up to event resolution, especially prevalent in sports markets. Interestingly, the business category saw more distributed volumes, although also spiked in the final days of trading. This possibly reflects traders responding to new information coming out throughout the period. Business markets included ‘Fed decision in January?’, for example.

Spreads also generally improved towards event resolution across longer dated markets, although most of the markets in our sample had less than 2 weeks of trading history until event resolution, suggesting most markets are launched much closer to event resolution. We found that while Polymarket spreads can be relatively tight due to more granular tick sizing on some markets, spreads across the set as a whole were relatively higher vs some of the most traded individual markets.

Sizing the Potential Opportunity for Prediction Markets

Spurred by interest in political odds around the 2024 U.S. Presidential Election, prediction market volumes grew nearly 4X sequentially to $64B in 2025, per data from Artemis. Volumes have accelerated since mid-2025, notching 5 consecutive months of ATH volumes through January 2026, driven in part by new entrants and growth in incumbents. Across all prediction markets measured by Artemis, volumes totaled $27B in January 2026, on track for volumes of over $325B at this pace, or 5X 2025 volumes.

We see parallels in the recent acceleration of prediction markets activity to the early growth seen in perpetual futures, as both were novel kinds of tradable markets, although worth noting they are regulated differently. Both allowed traders to express views on events and assets in ways that have not been possible previously.

Total reported perpetual futures volumes for BTC and ETH alone grew from $1T in 2019 to $42T by 2025, a CAGR of approximately 78%. Applying this rate to prediction markets, we could see volumes exceed $1.1T by 2030. Supporting the growth of these markets will be the liquidity flywheel. Today, prediction market orderbook depth is still relatively thin despite growing volumes, preventing larger traders from coming in size. As adoption and liquidity improve, these markets should be able to absorb larger trade sizes, therefore driving volumes.

Supporting this trajectory are increasing integrations of these platforms, with both Polymarket and Kalshi able to have other FCMs connect to their markets. Most recently, we have seen Coinbase offer prediction markets through Kalshi on the back end, while sports entertainment operator PrizePicks announced an integration with Polymarket.

Furthermore, the introduction of leverage could provide meaningful growth in the space. Today, contracts are fully collateralized, so offering leverage on such events could unlock significant capital efficiency for participants and help support greater notional volumes.

Also worth noting is other players entering the market on their own. Robinhood initially integrated with Kalshi, but later announced a JV with Susquehanna International Group to roll out its own prediction markets platform via acquisition of CFTC-licensed exchange and clearinghouse MIAXdx. In the announcement, it noted “Prediction Markets have quickly become Robinhood’s fastest-growing product line by revenue.” In its 4Q25 earnings release, it said its annualized prediction market revenue grew nearly 4X QoQ to $435M and listed prediction markets among its top priorities in 2026. Other players such as Interactive Brokers and Crypto.com have moved to offer their own prediction markets as well. The breadth and availability of these offerings should help drive adoption over time, similar to the expansion of perpetual futures.

Crypto-native platforms are also rolling out prediction markets. In February 2026, Hyperliquid announced plans for HIP-4 markets that would support outcome trading, such as prediction markets and options-like instruments. Backpack was also reported to be developing its own prediction market, said to be in private beta. Other major DEXes including dYdX and Drift launched prediction market offerings in 2024.

Looking Ahead: Regulation and Leverage to be Drivers

One of the key drivers behind prediction markets may be their legitimacy provided by CFTC regulation, enabling their broader rollout in the US, and this liquidity hub driving international activity.

On this front, Michael Selig was recently confirmed as the new CFTC Chairman, and he has signaled plans to write new rules for prediction markets, specifically to establish “clear standards for event contracts that provide certainty to market participants.” The CFTC has since withdrawn a proposed rule from 2024 that would have prohibited sports and political-related sports contracts. It has also withdrawn a 2025 advisory that warned about state-level litigation from offering sports-related contracts, indicating intent to defend its jurisdiction over event contracts vs state regulators. Such moves come as state gaming regulators pursue prediction markets for allegedly operating unlicensed sportsbooks, and could ultimately result in prolonged legal battles. Further constructive policies from the CFTC could help attract more participation and liquidity in these markets.

Another key factor that could propel growth for prediction markets is the introduction of leverage. Currently, both Polymarket and Kalshi offer fully collateralized contracts, likely in part due to regulatory considerations. It’s possible that they move to offer leverage in the future, which could help drive volumes. Key to this would be lining up market makers to handle larger notional sizes and designing risk and liquidation engines that could handle the relatively rapid gapping of event contracts. While a complex problem to solve, the success of the perps market offering up to 100x leverage on volatile tokens suggests it is possible to accomplish.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a swap dealer with the U.S. Commodities Futures Trading Commission (CFTC) and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is licensed by the MFSA as a Class 2 Crypto-Asset Service Provider (Regulation (EU) 2023/1114). It is also licensed as a Financial Institution (Cap. 376) exclusively for EMT payment services. FalconX’s complaint policy can be accessed by sending a request to complaints@falconx.io

"FalconX" is a marketing name for the FalconX Group and its affiliates. Availability of products and services can be subjected to jurisdictional restrictions and operational capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.