Fear in the Market, Aave’s Consumer App, ZK L2s Run

Market Sentiment Erodes

The market is at a crossroads with BTC and ETH recently erasing gains for the year, while SOL is now -25%. The Fear and Greed index (0-100) reads 14 as of November 17, firmly in the ‘Extreme Fear’ category. Readings have remained under 20 for a whopping 5 days in a row, highlighting the notable decline in sentiment.

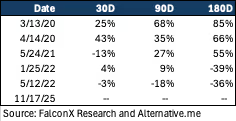

As far back as 2020, there have only been 5 other instances of a reading below 20 for 5+ days, most notably March 2020 (Covid crash), May 2021 (China BTC mining ban), and May 2022 (Terra/Luna collapse). So, it is telling of how severe this selloff is vs previous major events. Data on forward returns is mixed here and is largely a factor of whether we are in a mid-cycle lull or early innings of a sustained bear market.

Forward Returns on 5+ Day Streak of Fear & Greed Readings Below 20

The index aims to capture sentiment for BTC and other large cryptocurrencies; consequently, it may understate the current pain in alts. In a basket of the largest 150 alts by market cap, nearly half are below their prices on April 8, 2025 (the day BTC bottomed after Trump tariff selloff), with an average price decline of 27% from those levels.

YTD, the picture is bleaker with only 12% of the set posting positive performance YTD. New launches are particularly hard hit, with names in the cohort that are down YTD have declined an average of 65%.

By sector, it is worth flagging that DeFi staples with otherwise decent activity and revenues have seen some of the sharpest YTD drawdowns. JTO, DYDX, RAY, ENA, and JUP are all down ~70-85% this year, with several below their tariff selloff lows. It is a sign that investors are becoming increasingly discerning with allocating to revenue-producing names even as multiples compress. On the L1 side, newer projects have seen some of the most pressure with SUI, SEI, TON, and APT all -60%+ YTD, suggesting investors are also punishing L1s that have failed to produce meaningful fees or activity yet.

Aave’s Consumer App

Lending protocol AAVE announced a consumer-facing high yield savings product (‘Aave App’). It’s worth following for several reasons:

· It offers up to 9% APY on stablecoins (5% base rate + boosts), exceeding yield paid by banks and fintechs

· Advertises $1M insurance per account (greater than the $250K FDIC insurance)

· Enables direct deposits from bank accounts

The insurance component could be a breakthrough for the crypto space, where insurance for DeFi participation has been hard or expensive to acquire, especially at this scale. This could help encourage more participation from retail to institutions, especially following the recent Balancer hack.

Arguably more important is that Aave is looking more like a fintech and less of a DeFi protocol with this offering. Its app looks sleek and simple, while its messaging seems focused on the higher yield. This kind of approach resembles that of its fintech peers and could prove effective in onboarding new users. Crypto apps have historically faced challenges in acquiring new, non-crypto-native users due to complexity and friction in the process (sourcing funds, setting up a wallet, gas fees, etc.). Aave’s app promises to upend that.

Keep in mind, despite operating as a DeFi protocol and not a bank, Aave’s TVL ($54B) would rank it amongst the 50 largest banks by deposits. At this scale, and with a time-tested protocol, it will be interesting to see how and whether they can capture the retail market. Moreover, with the market expecting more Fed cuts in the next year, Aave’s historically above-market rates may be more enticing for this audience.

L2 Tokens Heat Up

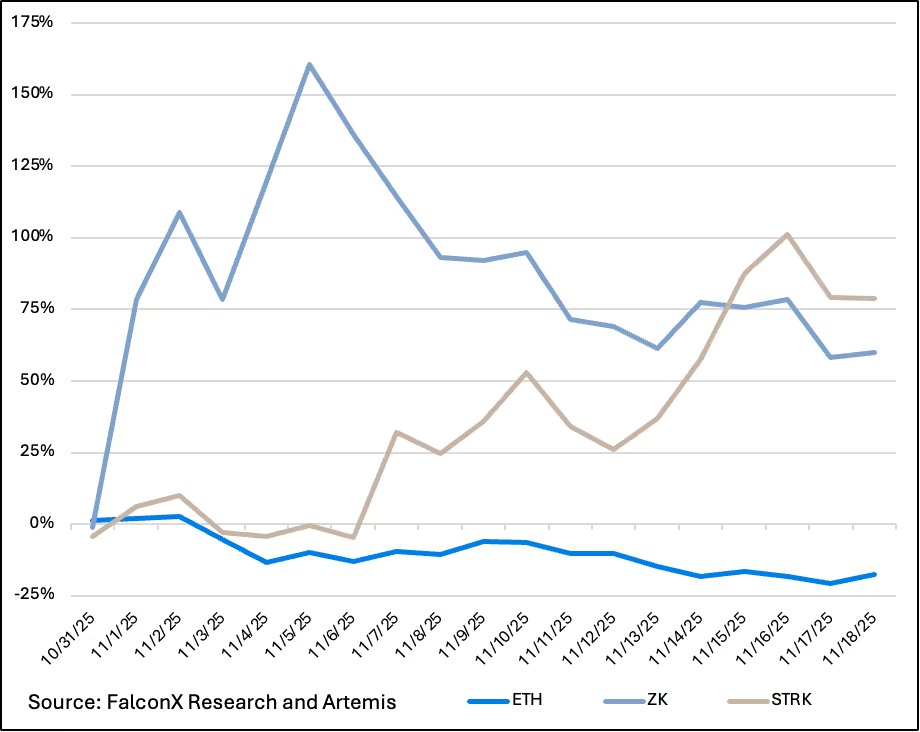

Two of the top performers MTD in November are L2 names: STRK and ZK, both of which are ZK-related names. Considering the broader weakness in the crypto market over this period, it’s worth noting that both projects announced tech upgrades that purport to meaningfully improve ZK functionality.

November MTD Returns of ZK and STRK vs ETH

ZKSync (ZK): The token jumped 80% at the start of the month after Vitalik Buterin posted twice on the same day about it, stating the project’s work was ‘underrated and valuable’ in regards to its recent Atlas upgrade, which promises to bring 15K+ TPS and near-real time ZK proofs (compares to 1hr batch proving times previously).

The Atlas upgrade improves L2 to L2 and L1 to L2 interop latency significantly to where it is fast enough to simply draw on liquidity directly from the Ethereum L1, removing the need to maintain a hub of capital on the L2.

On Nov 4, ZKsync’s founder Alex Gluchowski published a tokenomics proposal, calling for on-chain protocol fees and real-world fee arrangements to go to ZK buybacks to go towards a burn, staking rewards, and treasury funding for protocol/ecosystem development. It sees interop fees as a key driver of protocol fees in the future, while off-chain revenues would be driven by enterprise licensing.

Starknet (STRK): Announced its new prover, which it claims to be the fastest built, that is up to 100x faster and more cost effective than its prior one, boosting network efficiency and enabling local proof generation. It says this enables new use cases such as zk-ID.

It has also benefited from traction in its BTCFi initiative, which involves bridging BTC assets (ex: WBTC) to Starknet to be staked to secure the network and/or deposited into DeFi yield strategies. This has seen considerable interest with $100M+ in BTC staked as of Nov 17.

Separately, the project has benefited from its link to privacy around Zcash's (ZEC) impressive recent performance. STRK’s co-founder Eli Ben-Sasson is also a co-founder of Zcash. STRK announced plans to connect Zcash to its L2 via proofs, enabling smart contracts for it.

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd. nor Banzai Pipeline Limited service retail counterparties, and the information in this material is NOT intended for retail investors. This material is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this material is not and should not be regarded as investment advice, investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over the counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a Swap Dealer with the U.S. Commodities Futures Trading Commission and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is licensed by the MFSA as a Class 2 Crypto-Asset Service Provider (Regulation (EU) 2023/1114). It is also licensed as a Financial Institution (Cap. 376) exclusively for EMT payment services.

"FalconX" is a marketing name for the FalconX Group and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.